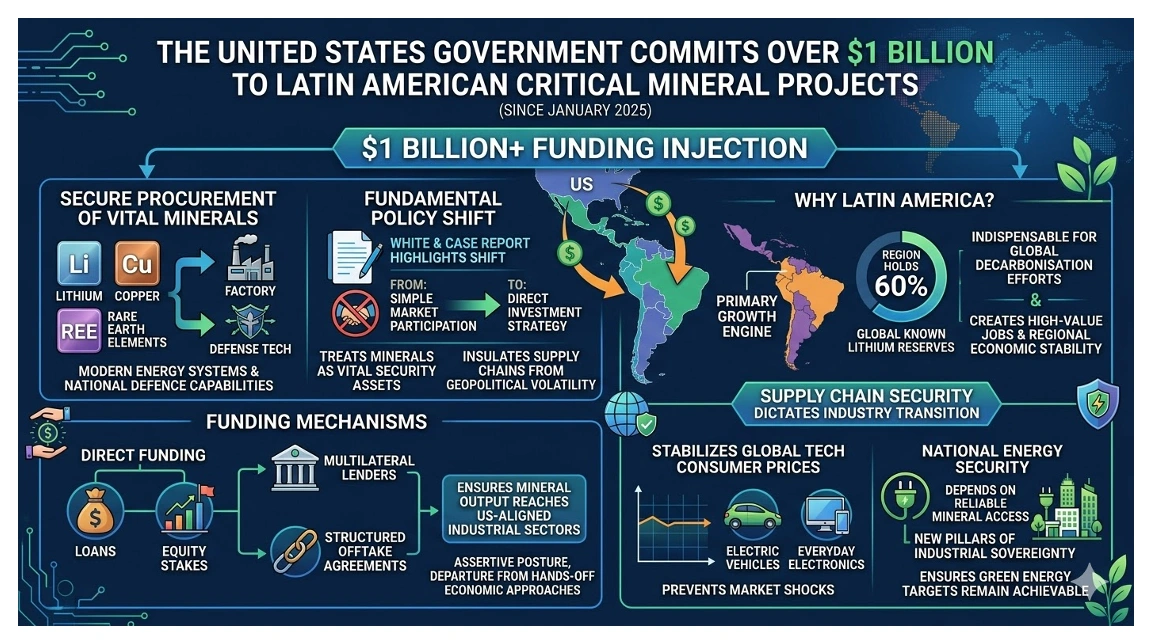

The United States Government has committed over $1 billion to critical mineral projects across Latin America since January 2025. This capital injection targets the secure procurement of lithium, copper, and rare earth elements. These materials remain essential for modern energy systems and national defence capabilities.

Washington now treats these minerals as vital security assets. A report by law firm White & Case highlights this fundamental policy shift. Government agencies now prefer direct investment over simple market participation. This strategy aims to insulate supply chains from geopolitical volatility.

Direct funding supports projects through loans and equity stakes. Multilateral lenders also provide structured offtake agreements for regional miners. These financial instruments ensure that mineral output reaches US-aligned industrial sectors. This assertive posture marks a departure from previous hands-off economic approaches.

Supply Chain Security Dictates Industry Transition

Securing these minerals stabilises prices for global technology consumers. Critical minerals power electric vehicles and advanced aerospace hardware. Supply chain disruptions often lead to higher costs for everyday electronics. This investment surge aims to prevent such market shocks.

National energy security now depends on reliable mineral access. Governments view these resources as the new pillars of industrial sovereignty. The transition to renewable energy requires vast amounts of raw materials. Reliable supply chains ensure that green energy targets remain achievable.

Investors see Latin America as a primary growth engine. The region holds 60% of the world’s known lithium reserves. This concentration makes the territory indispensable for global decarbonisation efforts. Successful mining operations create high-value jobs and regional economic stability.

$1b Roadmap For Securing The Critical Minerals

$1b Roadmap For Securing The Critical Minerals

Business Leaders and Lenders Coordinate Projects in the Region

The second Trump administration leads this strategic financial deployment. Key officials coordinate with the US Development Finance Corporation on project funding. Law firm White & Case monitors the regulatory shifts affecting these deals. Their legal experts track the intersection of mining and national policy.

Major corporate players like Rio Tinto actively participate in the region. Rio Tinto secured approval for a $2.5 billion lithium project in Argentina. The Inter-American Development Bank also provides substantial low-interest loans. These institutions facilitate the massive capital requirements of modern mining.

The private sector drives innovation within these emerging mineral corridors. Brazilian Rare Earths explores high-grade deposits in Minas Gerais. Their leadership emphasises the strategic importance of domestic processing capacity. Such companies bridge the gap between raw extraction and industrial utility.

St George Mining occupies a strategic position within this ecosystem. This Australian explorer focuses on high-potential targets in Brazil’s Lithium Valley. Their presence aligns with the broader push for Western-aligned supply chains. Investors monitor such firms for their ability to deliver critical tonnage.

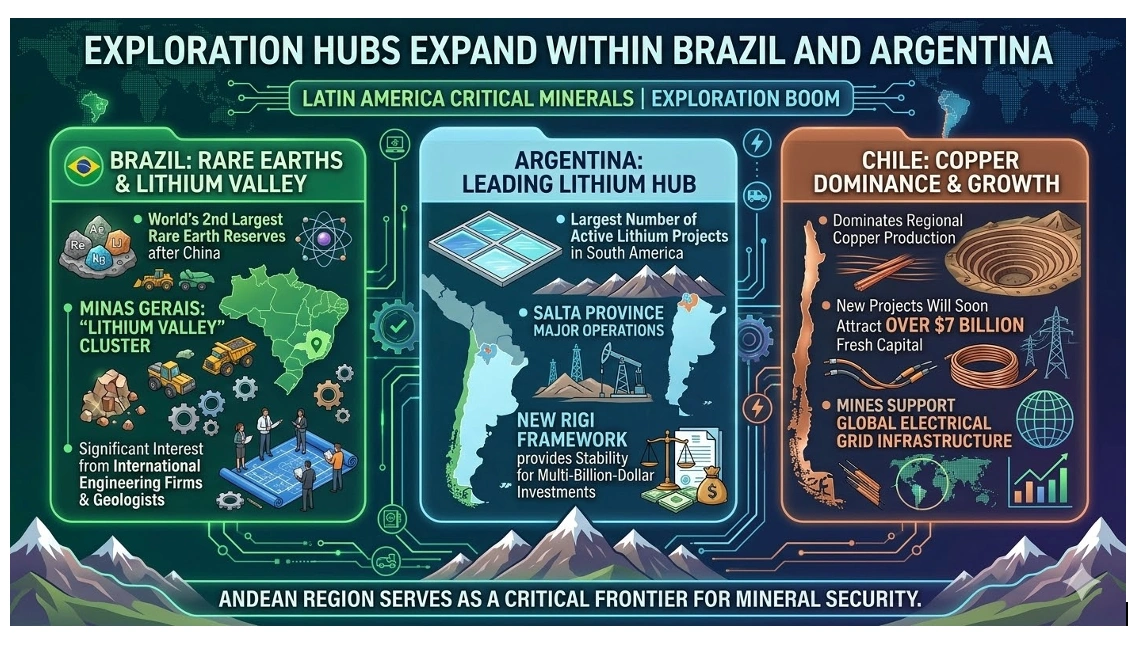

Exploration Hubs Expand Within Brazil and Argentina

Brazil and Argentina serve as the primary destinations for this capital. Brazil hosts the world’s second-largest rare earth reserves after China. The Minas Gerais region now carries the moniker Lithium Valley. This cluster attracts significant interest from international engineering firms and geologists.

Argentina remains the leading hub for lithium exploration and development. The country manages the largest number of active lithium projects in South America. Salta province hosts major operations under the new RIGI framework. This legal structure provides the stability necessary for multi-billion-dollar investments.

Chile continues to dominate the regional copper production landscape. New projects in Chile will soon attract over $7 billion in fresh capital. These mines support the global demand for electrical grid infrastructure. The entire Andean region serves as a critical frontier for mineral security.

Latin America’s Critical Minerals Boom

Latin America’s Critical Minerals Boom

Production Targets Rise as Market Values Stabilise

The current investment surge began in earnest during January 2025. This timeline followed the implementation of the US strategic mineral roadmap. Argentina launched its Incentive Regime for Large Investments in July 2024. These policies set the stage for the massive spending seen today.

Market conditions improved significantly by early January 2026. Battery-grade lithium carbonate prices rebounded to $18,200 per tonne. This price recovery encouraged lenders to finalise pending project applications. The government expects lithium output to peak significantly by 2035.

Brazil showcased its mining potential during a summit in June 2025. Delegates at Belo Horizonte discussed the shift toward energy security. Several copper projects in Chile are preparing for operations starting next year. These milestones indicate a period of rapid industrial expansion and scaling.

Also Read: St George Mining Delivers High-Grade Rare Earths and Niobium Hits at Araxá

Geopolitics and Policy Determine Mining Success

Latin American governments will balance interests between Washington and Beijing. Chinese firms currently process over 90% of global rare earth elements. Regional leaders seek to build domestic processing facilities to capture value. This pragmatism allows them to accept capital from diverse global sources.

Regulatory frameworks will continue to evolve to attract foreign miners. Argentina’s RIGI framework offers tax and customs stability for thirty years. Brazil may implement incremental reforms to improve environmental compliance standards. These policies determine the speed of project approvals and site development.

Geopolitics will influence every major mining transaction and merger review. European and US regulators now scrutinise deals for strategic alignment. Companies must navigate complex compliance hurdles to secure long-term financing. Strategic alignment with US priorities provides a competitive advantage for explorers.

The demand for copper will drive the next decade of investment. Global requirements for the metal will likely double by 2035. Power grids and electrification efforts consume vast quantities of copper wire. Miners must scale operations quickly to meet these projected industrial needs.

- US investment has exceeded $1 billion since early 2025.

- Argentina targets 658,000 tonnes of lithium by 2035.

- Brazil holds 23.3% of global rare earth reserves.

- Copper demand projections show a 100% increase by 2035.

- Lithium prices stabilised near $18,200 per tonne in 2026.