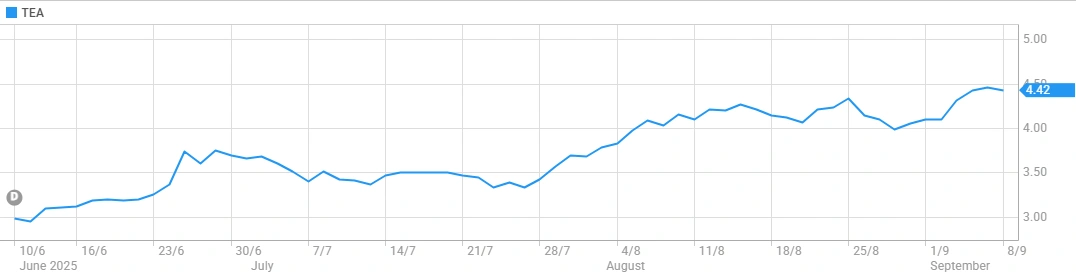

Tasmea Limited (ASX: TEA) has wrapped up a solid $43 million institutional placement at $4.30 per share on 8 September 2025. This move shows clear investor faith in the company’s path forward. The price sat at just a 2.3% discount from the last close, pointing to keen interest from big players in this diversified specialist trade services firm.

This institutional placement says a lot about Tasmea’s focus and careful handling of finances. Leaders have highlighted two main goals: boosting chances for index inclusion and speeding up growth via smart buys.

Tasmea Pushing for ASX 300 Status

With a bigger free float and more institutional holders, Tasmea stands a better shot at joining the ASX 300 Index come the March 2026 review. That could mean more trading activity and a wider pool of investors.

Tasmea aims for admission to the ASX 300 Index in March 2026 Rebance

Getting into these indices brings real perks for companies. For instance, New Zealand firms listing on the ASX often see early index spots as a drawcard. Being in something like the S&P/ASX All Technology index pulls in money from funds that track it, creating a cycle where more liquidity leads to even more.

Tasmea figures its spot in the S&P/ASX 300 could draw in more big investors, much like we’ve seen with other recent additions. Firms entering the ASX 300 usually gain better exposure and easier access to global funds.

Taasmea’s Acquisitions Backed by Smart Money Management

The fresh funds will help chase down several acquisition targets already in the works, giving Tasmea a stronger hand to ramp up its planned buyouts.

Tasmea keeps things disciplined when it comes to debt. It holds its net debt to EBITDA ratio under 1.0x, with net debt (minus property leases) over FY23 pro forma EBITDA at 0.45x. This steady approach echoes what works in Australia’s mining and industrial fields, where outfits like Northern Star have shown sharp discipline in big deals.

The company eyes buys in the $10-40 million bracket, where fewer rivals tend to compete. It’s paid off so far, with recent picks like West Coast Lining Systems, Future Engineering Group, and the $27 million Flanco Group deal.

Strong History of Acquisitions at Tasmea

Tasmea’s recent results back up its knack for blending acquisitions and drawing out value. For the year ending 30 June 2025, revenue jumped 37%, and after-tax profit climbed 74.9% from the year before.

Bought businesses keep running on their own but tap into central support for strategy, finance, and operations. This setup holds onto that startup spirit while grabbing efficiency gains.

Cross-selling stands out as a big win. Leaders expect to boost income by offering Tasmea’s specialist maintenance services to new customers from deals like Flanco.

Backing from the Market and Experts

Pulling off the placement with such a small discount underlines solid trust from institutions. Analysts stay upbeat, with the average one-year price target for Tasmea (ASX: TEA) now at $4.49 per share – a 29.41% lift from the earlier $3.47 mark.

Tasmea Limited Share Price

Morgans, with a buy rating, sets a $4.35 target, pushing the average from three key brokers to $4.40. That suggests about 25% upside from current prices.

Where Tasmea’s Institutional Placement Fits in the Industry

The industrial services space has some favourable long-term trends. Australia’s outsourced maintenance market tops $21 billion, with an addressable slice over $8 billion for players like Tasmea.

Unlike some who chase deals just for size, Tasmea stresses real improvements and synergies, much like top performers in mining.

Tasmea’s strong balance sheet underpins its plans. It aims to pay fully franked dividends, handing out 30% to 50% of retained earnings based on performance and position.

This policy reflects belief in steady cash flow, while keeping funds free for key opportunities.

Also Read: Ancient Rocks in Australia Reveal New Niobium Deposit for Clean Energy and Steel

What’s Next for Tasmea Limited

This institutional placement marks Tasmea’s shift from newcomer to a more established name in industrial services. The strong pricing and investor turnout confirm its direction.

With exec directors holding 60.8% of shares for long-term commitment, Tasmea looks set to blend organic growth with targeted buys.

The March 2026 ASX 300 review could spark more liquidity and big-holder interest. Paired with its careful acquisition style and solid operations, this capital raise sets Tasmea up for its next growth chapter.