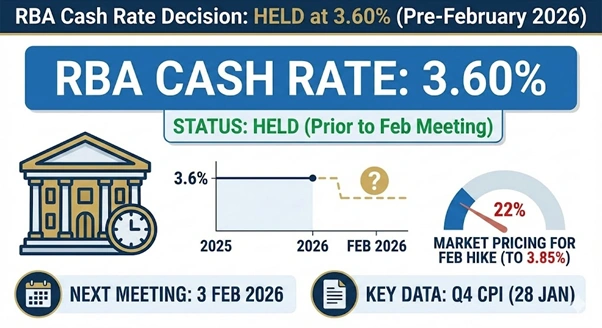

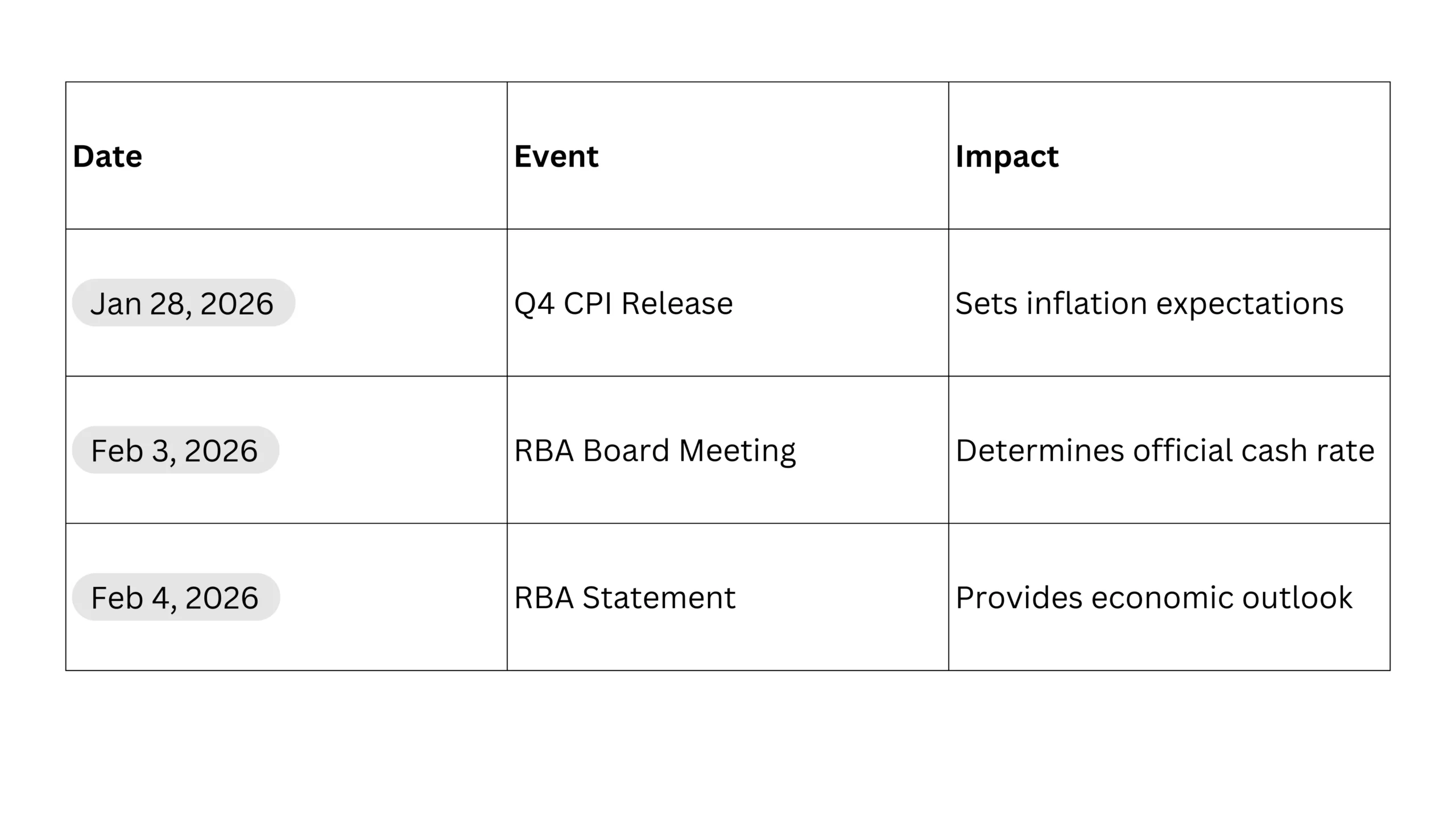

The Reserve Bank of Australia maintains the official cash rate at 3.6%. Board members meet again on 3 February 2026 to discuss further adjustments. Financial markets currently price a 22% chance of a rate increase to 3.85%. This follows the final policy decision of 2025, where officials kept costs at the lowest level since April 2023.

Inflation risks remain a primary concern for the central bank. Minutes from the December meeting show the board considers the possibility of higher rates. Consumer price readings from October and the third quarter showed surprisingly high results. The board now waits for the fourth-quarter inflation data due on 28 January.

RBA cash rate decision

Banking Majors Lift Fixed Rates Ahead of RBA Decision

Commonwealth Bank and Macquarie Bank recently increased fixed home loan rates. These lenders lifted some products by as much as 70 basis points. Commonwealth Bank now advertises its lowest fixed rate at 5.79% for a two-year term. This change occurred despite the RBA keeping the cash rate steady in December.

Lenders often adjust fixed pricing to reflect their own economic outlooks. Macquarie Bank increased its rates for the third time in three months. Its lowest fixed offer now sits at 5.59%. These movements suggest that banks expect higher borrowing costs in the near future.

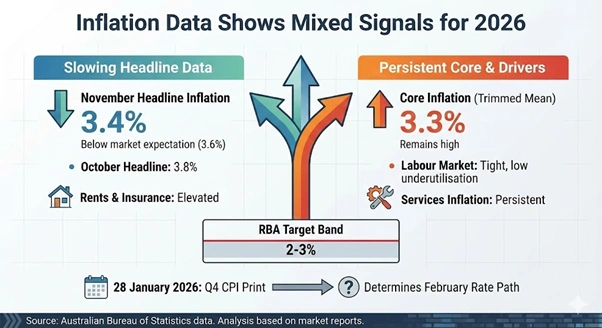

Inflation Data Shows Mixed Signals for 2026

The Australian Bureau of Statistics reports that inflation slowed to 3.4% in November. This figure fell below the market expectation of 3.6%. However, the result still sits above the RBA target band of 2 to 3%. Core inflation remains high at 3.3% according to recent data.

- Headline inflation reached 3.8% in October.

- Services inflation for rents and insurance stays elevated.

- The labour market remains tight with low underutilisation.

- The upcoming 28 January CPI print will determine the February rate path.

Average Market Rates for Variable and Fixed Loans

The average variable mortgage interest rate in Australia currently stands at 6.41%. Data from Finder shows that the average fixed rate is lower at 5.83%. Borrowers find the lowest variable rates around 4.99% from specific lenders. Fixed rates for two-year terms start at 4.94% in the current market.

The gap between fixed and variable rates influences many household decisions. Fixed loans currently offer a lower average entry point than variable products. However, fixed loans limit the use of certain features like offset accounts. Borrowers must weigh the lower rate against the loss of flexibility.

Impacts of Potential Rate Hikes

A small change in the cash rate creates significant impacts for average borrowers. Canstar data indicates a 0.25 percentage point hike adds $90 to monthly repayments on $600,000 loans. For a $1 million mortgage, the monthly cost increases by approximately $150. These figures assume banks pass on the full central bank increase to customers.

- $600,000 Loan: Monthly repayments rise by $90.

- $750,000 Loan: Monthly repayments rise by $112.

- $1,000,000 Loan: Monthly repayments rise by $150.

Financial experts urge borrowers to review their current financial buffers immediately. Household consumption showed unexpected strength in the final quarter of 2025. This trend complicates the path for further interest rate relief in 2026. Governor Michele Bullock previously stated that rate rises remain a risk if inflation stays high.

Major Bank Forecasts Diverge on Future Hikes

Economists from the Commonwealth Bank and NAB predict a rate hike in early 2026. They cite persistent price pressures and strong consumer spending as the main drivers. These analysts believe the RBA will increase the cash rate by 0.25 percentage points in February. This move would take the official rate to 3.85%.

Westpac and ANZ economists expect the RBA to remain on hold in the near term. They note that modest economic growth and cost-of-living pressures constrain household spending. These experts believe the central bank will assess more data before changing policy. Risk remains balanced between future increases and potential cuts later in the year.

Strategy for Homeowners Considering Fixed Rates

Fixing a home loan provides certainty for monthly repayments. This tool helps households manage budgets during periods of economic uncertainty. Many borrowers choose two-year terms as a common middle ground. This duration allows for planning without locking in a rate for too long.

- Fixed rates provide protection against future RBA increases.

- Fixed loans often restrict extra repayments and redraw facilities.

- Break fees apply if a borrower exits the loan early.

- Repayments stay the same regardless of market movements.

Also Read: Iconic Fresh Prince Mansion Lists for $30 Million After Nearly 50 Years

The Benefits of Splitting the Home Loan

Australian borrowers can choose to split their mortgage between fixed and variable portions. This strategy allows for a combination of certainty and flexibility. A borrower might fix 50% of the loan and keep the rest variable. This setup protects half the debt from rate rises.

The variable portion still allows for the use of an offset account. It also permits the borrower to make unlimited extra repayments on that section. If interest rates fall, the variable portion of the loan benefits immediately. This approach spreads the risk across different market scenarios.

Key Dates for Australian Borrowers in 2026

The next few weeks will provide clarity for homeowners. The Australian Bureau of Statistics will release the December quarter CPI on 28 January. This data point serves as the final indicator before the RBA meeting. A high reading will likely trigger a rate increase in February.

Borrowers should review their current interest rates against the market average. Contacting a lender for a rate review can lead to immediate savings. Proactive management of the mortgage remains essential in the current climate.