National Australia Bank (NAB) has issued its FY2025 Pillar 3 Report, presenting key data on capital adequacy, risk exposure, and balance sheet stability. The bank continues to reinforce its commitment to transparency and robust risk management as it navigates an evolving financial landscape.

NAB released its FY2025 Pillar 3 Report

NAB released its FY2025 Pillar 3 Report

Strength in Capital Adequacy

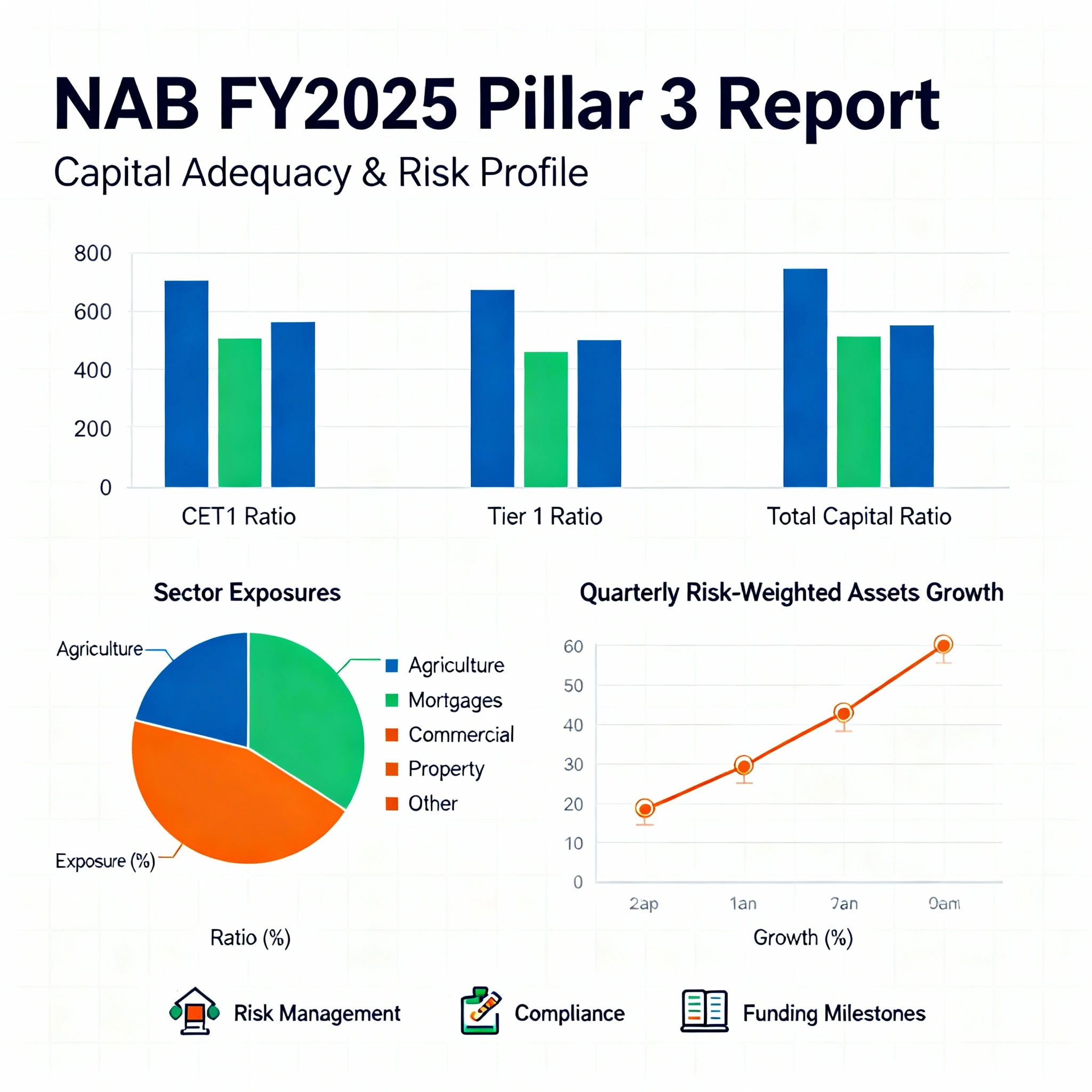

NAB’s Common Equity Tier 1 (CET1) capital ratio strengthened to 12.14% by the end of June 2025, up from 12.01% at March’s close. The total capital ratio reached 20.54%, with a Tier 1 capital ratio standing at 14.33%. Directors attribute this increase to $1.7 billion in retained earnings and positive impacts from currency translation. Capital generation remains a priority with board guidance unchanged.

CEO Andrew Irvine commented in the official release, “We remain optimistic about the outlook and are well placed to manage NAB for the long term and deliver sustainable growth and returns for shareholders”.

Risk-Weighted Assets and Loan Growth

The report points to a $10.4 billion, or 2.4%, quarterly jump in risk-weighted assets (RWAs), reaching $442.3 billion at June’s end. Credit Risk-Weighted Assets (CRWA) rose by 4.9% in the quarter, led by climbing corporate and business lending alongside changes in off-balance-sheet exposures. Loan and acceptances growth, driven by business and home lending, pushed total gross loans to $773.2 billion, up from $756.3 billion at March’s close.

NAB FY2025 Pillar 3 Report key financial and risk highlights

Leverage Ratio and Liquidity Coverage

NAB’s leverage ratio advanced to 5.11% by June, a nine-basis-point rise since March. The ratio reflects increased Tier 1 capital against total exposures, which hit $1.23 trillion after 1.3% quarterly growth. NAB’s liquidity coverage ratio dipped to 135%, slightly down from 139%, tracing to a rise in weighted net cash outflows and greater wholesale maturities. The net stable funding ratio steadied at 116%, with required funding up by $18.7 billion and available stable funding up by $8.1 billion.

Asset Quality and Risk Provisioning

Exposure at Default (EaD) closed at $1.11 trillion for the third quarter. Non-performing exposures increased by $623 million, or 5.5%, now standing at $11.88 billion. The spike centres on a $349 million rise in default-but-not-impaired exposures and a $274 million climb in impaired assets.

NAB’s provision for credit impairment on non-performing exposures stood at $2.29 billion at June, up by $90 million since March. The total provision, inclusive of performing assets, touched $6.15 billion. NAB attributed much of the uptick to sectors including manufacturing, agriculture, and commercial property.

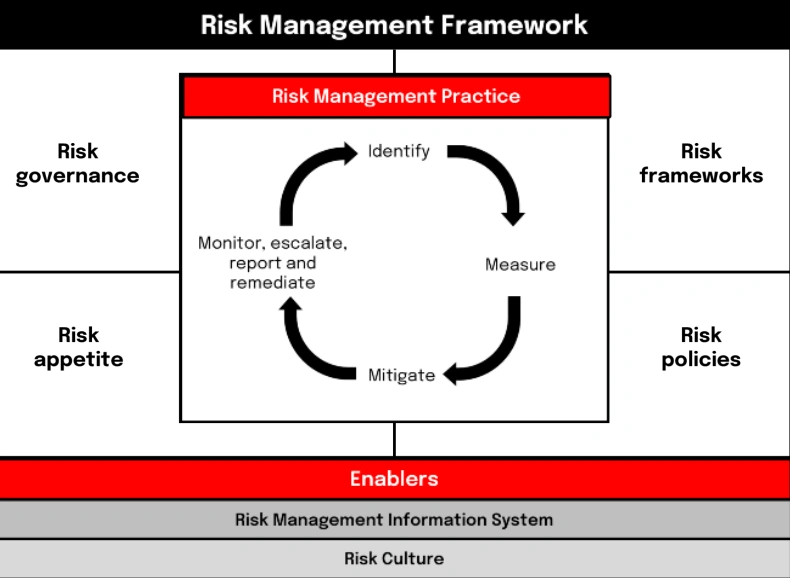

NAB’s risk management framework

Credit Impairment and Portfolio Performance

Credit impairment charges surged to $254 million for the third quarter, a sharp increase from $81 million in the previous period. Senior management cited business lending in Australia and New Zealand as major contributors to the higher charge alongside growth in unsecured retail lending portfolios. NAB saw the ratio of non-performing exposures to gross loans inch up to 1.54%, a sign of ongoing watchfulness in portfolio performance.

Sector Breakdown and Portfolio Mix

Agriculture, forestry, fishing, and mining exposures reached $70.8 billion. Residential mortgages accounted for $493.4 billion in exposure, with commercial property at $91.9 billion. Business services, construction, and retail also represented significant volumes across the lending book.

Liquidity, Funding Initiatives, and Compliance

NAB raised $30.5 billion in term wholesale funding by June after accessing global markets to maintain liquidity and support ongoing lending. Payroll remediation costs reached $130 million for the year as the bank continued its focus on workforce management and compliance.

NAB’s board reaffirmed its commitment to productivity savings beyond $400 million for FY25, with operating expenses expected to grow by 4.5% this year. Removal of the Enforceable Undertaking by AUSTRAC signalled progress in NAB’s compliance and risk management programs.

Also Read: How Australians Can Access Three Hours of Free Solar Power Daily from 2026

Outlook and Strategic Direction

NAB remains focused on capital conservation, with CET1 capital above minimum requirements at 7.64%. The board maintains buffers to meet D-SIB and countercyclical guidance. The group invests further in technology and risk controls to support a prudent, resilient banking franchise.

NAB’s FY2025 Pillar 3 Report confirms steady discipline in risk management, strong capital ratios, and resilience in banking operations. The results reinforce stakeholder confidence in one of Australia’s core financial institutions as it enters the final quarter of the financial year.