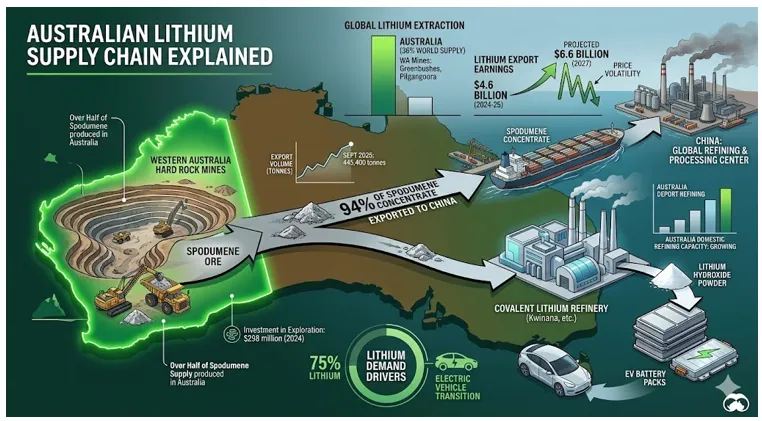

Mining operations in Australia currently lead the world in the production of lithium. Data from 2025 indicates that Australia accounts for 36 per cent of the extraction of this metal. Most of this production comes from hard rock mines in Western Australia. These facilities extract spodumene concentrate for export.

The export volume from Australia reached 445,400 tonnes in September 2025. This figure represents a peak for the year. The nation sends 94 per cent of this material to China for processing. The dependence on China for refining remains a factor in the market.

Australia aims to increase the value of its exports. The government supports the construction of refineries within the country. The Covalent Lithium refinery in Kwinana represents one such project. This plant produces lithium hydroxide for batteries.

The industry in Australia faces price volatility. Earnings from lithium exports totalled $4.6 billion in the 2024-25 period. Projections suggest this figure will rise to $6.6 billion by 2027. This growth depends on the increase in volume from mines.

- Australia produces over half of the supply of spodumene.

- Western Australia hosts the Greenbushes and Pilgangoora mines.

- Investment in exploration reached $298 million in 2024.

The transition to electricity for transport drives the demand for lithium. Batteries for vehicles consume 75 per cent of the lithium produced. Australia provides the raw material for these batteries. However, the refining process mostly occurs elsewhere.

Australia’s lithium supply chain

The Infrastructure and Refining Capacity of China

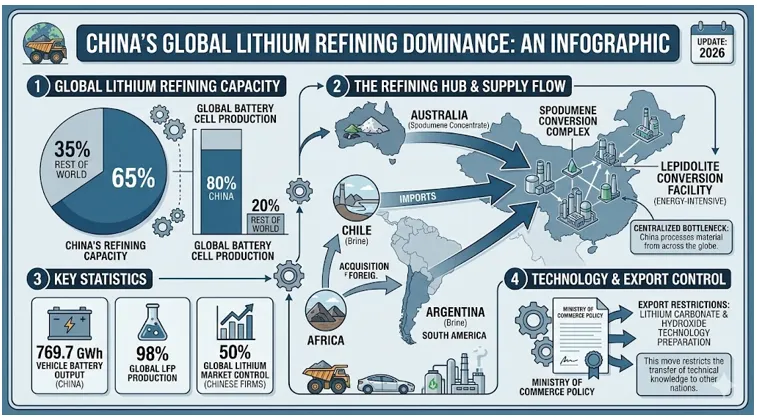

China controls the midstream and downstream sectors of the lithium supply chain. The nation manages 65 per cent of the refining of lithium chemicals. It also produces 80 per cent of the cells for batteries. China hosts the majority of the capacity for the conversion of spodumene.

The output of lithium from mines in China is also increasing. Forecasts suggest China will overtake Australia in mining by 2026. China utilises lepidolite for a portion of its production. This process requires more energy than the extraction from spodumene.

The strategy of China involves the acquisition of assets in other countries. Chinese firms hold stakes in mines in Africa and South America. This vertical integration secures the supply of feedstock for refineries. The dominance of China extends to the manufacturing of cathodes and anodes.

The Ministry of Commerce in China recently updated the catalogue of technologies for export. The list now includes the preparation of lithium carbonate and hydroxide. This move restricts the transfer of technical knowledge to other nations. China seeks to maintain its lead in the sector.

- China produces 769.7 GWh of batteries for vehicles.

- The nation accounts for 98 per cent of the production of lithium iron phosphate.

- Chinese companies control 50 per cent of the market for lithium.

The scale of production in China allows for lower costs. This advantage makes competition difficult for new entrants. The refineries in China process material from Australia, Chile and Argentina. This centralisation creates a bottleneck in the supply chain across the world.

China’s global lithium supply chain

The Strategy and Production Goals of the United States

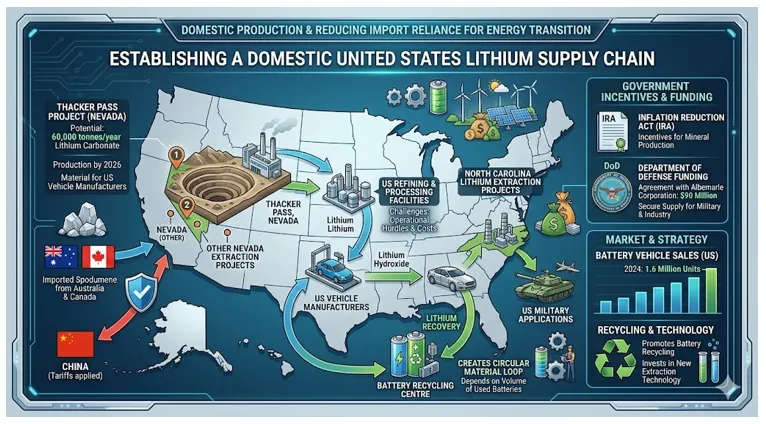

The United States works to establish a supply chain for batteries within its borders. The Inflation Reduction Act provides incentives for the production of minerals. The government aims to reduce the reliance on imports for the transition to energy.

The Thacker Pass project in Nevada represents a major development. This mine has the potential to produce 60,000 tonnes of lithium carbonate per year. The project expects to start production by 2026. This facility will provide material for manufacturers of vehicles in the United States.

The Department of Defence also provides funding for the mining of minerals. An agreement with Albemarle Corporation involves $90 million for domestic production. The United States seeks to secure the supply of lithium for the military and for industry.

The market in the United States currently depends on imports. Spodumene comes from Australia and Canada. The refining of lithium hydroxide in the United States faces challenges. Operational hurdles and costs impact the speed of the ramp-up.

- The sale of vehicles with batteries in the United States reached 1.6 million units in 2024.

- The government implements tariffs on materials from China.

- Projects in North Carolina and Nevada target the extraction of lithium.

The United States promotes the recycling of batteries to recover lithium. This approach aims to create a loop for the material. The success of this strategy depends on the volume of batteries available. The industry continues to invest in technology for extraction.

US lithium supply chain

Global Market Dynamics and the Outlook for 2026

The price of lithium experienced a decline in 2024 and 2025. This trend resulted from an oversupply of material in the market. However, prices began to recover in early 2026. The demand for storage of energy and for vehicles remains strong.

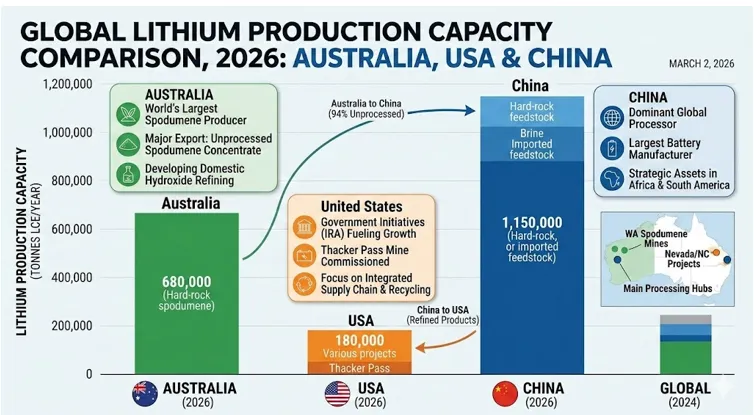

The competition between Australia, China and the United States shapes the market. Australia provides the raw material. China dominates the processing. The United States seeks to build an integrated chain.

The ban on exports of lithium from Zimbabwe impacts the supply. This decision removes a portion of the material from the market. The deficit in supply could lead to higher prices. The industry monitors these developments across the globe.

Global lithium production capacity comparison, 2026

The demand for lithium will reach 1.3 million tonnes of carbonate equivalent by 2030. This projection requires the opening of new mines. The industry must also address the impact of mining on the environment.

- The growth in the demand for lithium reaches 15 per cent per year.

- The market for batteries for storage expands rapidly.

- Investment in the sector focuses on the security of the supply.

The supply chain for lithium involves complex logistics. The movement of material from mines to refineries requires infrastructure. Australia, China and the United States invest in ports and rail. These improvements facilitate the flow of lithium to factories.

The future of the industry depends on the collaboration between nations. The standards for sustainability are becoming more important for investors. The “battery passport” requires transparency in the origin of the material. Australia and the United States emphasise these standards to differentiate their products.

China remains the leader in the conversion of lithium. The refineries in China have the capacity to meet the demand. The expansion of capacity in other regions takes time. The industry expects the dominance of China to continue in the short term.

The comparison of these three nations reveals different roles in the chain. Australia acts as the primary source of the metal. China serves as the hub for processing. The United States strives for independence in the sector.

The market for lithium enters a new phase in 2026. The focus shifts from the discovery of deposits to the execution of projects. The ability of companies to produce material at a low cost determines their success. The energy transition continues to drive the demand for this metal.