The global shift towards electrification and renewable energy has positioned base metals as the backbone of modern industrial growth. Premium copper and nickel producers on the London Stock Exchange (LSE) and TSX Venture Exchange (TSXV) are emerging as critical players in meeting surging demand from electric vehicles, charging infrastructure, and clean energy projects.

With global copper demand projected to reach 28.5 million tonnes in 2025 and nickel consumption growing at 5.7% annually, these LSE and TSXV copper and nickel companies are positioned to capitalise on unprecedented market opportunities.

LSE Copper Giants: Glencore and Anglo American Lead Production

The London Stock Exchange hosts two of the world’s most significant LSE copper producers Anglo American, Glencore, whose combined production capacity and strategic assets make them cornerstone suppliers for global industrial growth.

Glencore: Diversified Global Copper Leader

Glencore (LSE: GLEN) maintains its position as a global copper powerhouse despite facing production challenges in Q1 2025. The company’s own-sourced copper production of 167,900 tonnes in Q1 represented a 30% decline year-over-year, primarily due to lower ore mining rates at key operations.

However, Glencore’s full-year 2025 guidance remains robust at 850,000-890,000 tonnes of copper production. The company’s strategic assets span multiple continents, including:

- Collahuasi (Chile): 44% ownership in one of the world’s largest copper mines

- Antamina (Peru): 33.75% stake in the major copper-zinc operation

- KCC (Democratic Republic of Congo): Key African copper cathode production

The completion of Collahuasi’s planned pit reorientation and additional truck deployment is expected to drive stronger H2 2025 performance, with copper production anticipated to weight approximately 42%/58% over H1 and H2 2025 respectively.

Quarterly copper production trends 2024-2025

Anglo American: Copper-Focused Transformation

Anglo American (LSE: AAL) has significantly restructured its business to focus primarily on copper and iron ore, divesting non-core assets to capture the energy transition opportunity. The company’s 2025 copper guidance of 690,000-750,000 tonnes reflects its strategic pivot towards premium copper assets.

Key operational highlights include:

- Quellaveco (Peru): Flagship operation producing 300,000-330,000 tonnes in 2024, fully renewable-powered since 2023

- Los Bronces (Chile): Enhanced water recycling systems supporting consistent production

- Portfolio optimisation: Divestment of nickel assets to MMG for strategic focus

Anglo American’s H1 2025 copper production reached 342,200 tonnes, positioning the company well for its full-year targets despite temporary headwinds from lower grades at certain operations.

TSXV Nickel Juniors: Canada’s Critical Minerals Champions

Canada’s TSX Venture Exchange has become home to some of the world’s most promising TSXV nickel juniors Canada 2025, leveraging the country’s vast mineral endowment and proximity to North American battery supply chains.

Power Nickel: TSXV 50 Top Performer

Power Nickel (TSXV: PNPN) dominated the TSX Venture 50 rankings with a remarkable 630% share price increase over the past year, reaching CAD 1.70 per share for a market capitalisation of C$330.8 million.

The company’s flagship Nisk Project in Quebec has delivered outstanding results:

- Multi-zone mineralisation: Lion, Tiger, and Nisk deposits containing high-grade nickel-copper-PGM

- Expanded land package: Recent acquisition of 167 square kilometres from Li-FT Power

- Active drilling program: Four rigs targeting resource expansion across all deposits

Power Nickel’s transformation reflects the broader industrial growth copper nickel theme, with the company recently changing its name to Power Metallic Mines to better reflect its diversified mineral portfolio.

Canada Nickel Company: Timmins District Consolidation

Canada Nickel Company (TSXV: CNC) has strategically consolidated the Timmins Nickel District, positioning it as potentially the world’s largest nickel sulphide district. The company’s Crawford Nickel Sulphide Project represents the second-largest nickel resource globally based on Wood Mackenzie metrics.

Key project fundamentals include:

- Resource scale: 9.2 million tonnes of Measured & Indicated nickel across six deposits

- Government backing: Ontario recognition as priority nation-building initiative

- Zero-carbon potential: NetZero Metals downstream processing capability

- Strategic financing: CAD 17.5 million raised across multiple private placements in 2025

Talon Metals: US-Focused Battery Strategy

Talon Metals delivers targeted exposure to the US domestic battery supply chain through its Tamarack Project in Minnesota. The company’s 205.88% year-to-date gain to July 2025 reflects strong investor confidence in its strategic positioning.

The Tamarack Project benefits from:

- Rio Tinto partnership: Joint venture with global mining major

- High-grade deposits: Premium nickel-copper mineralisation for battery applications

- US domestic focus: Aligned with critical minerals reshoring initiatives

Also Read: Victory Metals Secures $11.5M to Advance North Stanmore Rare Earths Project

EV Charging Copper Demand: Infrastructure Expansion Drives Growth

The rapid expansion of electric vehicle charging infrastructure represents a major EV charging copper demand driver, with profound implications for copper consumption patterns.

Global Charging Infrastructure Requirements

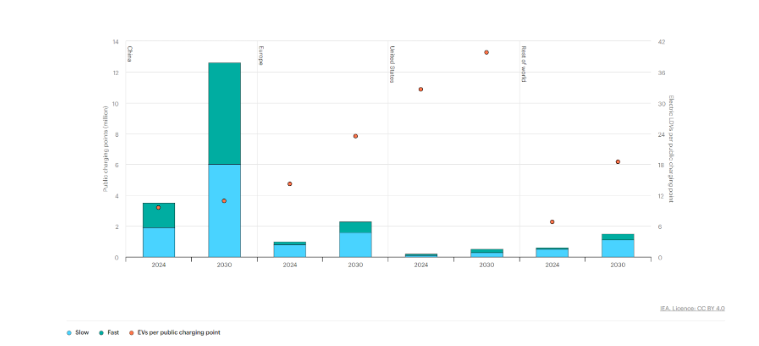

According to IEA projections, the global public charging stock must exceed 15 million points by 2030, representing a four-fold increase from 2023 levels. This expansion requires substantial copper inputs:

- Level 2 chargers: Approximately 1.5 kg copper per charging point

- DC fast chargers: Up to 8 kg copper per high-power installation

- Grid infrastructure: Additional copper for power distribution upgrades

The Alternative Fuels Infrastructure Regulation (AFIR) mandates DC fast charging installation every 60 km along EU’s TEN-T network by 2025, creating immediate copper demand.

Regional Infrastructure Investments

Key regional developments driving copper consumption include:

- United States: Target of 500,000 public charging stations by 2030

- European Union: Over 180,000 charging points in the Netherlands alone

- China: 85% of global fast chargers, targeting full urban and highway coverage by 2030

Global EV charging infrastructure

Renewable Energy Metals Outlook: Powering the Energy Transition

The renewable energy metals outlook shows accelerating demand for both copper and nickel across multiple clean energy applications, from wind turbines to battery storage systems.

Grid Expansion and Copper Intensity

Clean energy transitions necessitate significant electricity grid expansion. The IEA projects that grid expansion needs to more than double in the period to 2040 under sustainable development scenarios.

Key copper demand drivers include:

- Transmission lines: New interconnections for renewable energy integration

- Distribution networks: Grid modernisation for two-way power flows

- Offshore wind: High copper intensity for subsea cables and transformers

Battery Storage and Nickel Requirements

Energy storage systems represent a growing source of nickel demand, with battery applications accounting for 85% of total demand growth over the past two years.

Concentrated solar power expansion alone drives 75-fold growth in chromium demand and 89-fold growth in nickel demand between 2020 and 2040.

UK and Canadian Mining Stocks 2025: Investment Landscape

The investment landscape for UK and Canadian mining stocks 2025 reflects both opportunities and challenges as markets navigate supply-demand dynamics and geopolitical considerations.

LSE Performance Drivers

London-listed mining stocks benefit from:

- Currency advantages: GBP weakness enhances USD-denominated revenues

- ESG leadership: Established frameworks for sustainable mining practices

- Financial sophistication: Access to global capital markets and institutional investors

TSXV Growth Catalysts

Canadian junior miners on the TSXV offer:

- Resource jurisdiction: Stable regulatory environment and mining-friendly policies

- Critical minerals focus: Government support for strategic mineral development

- Proximity advantage: Access to North American industrial markets

The TSX Venture 50 companies achieved a combined market capitalisation of C$8.1 billion in 2024, representing a 174% increase year-over-year, with mining companies comprising two-thirds of the rankings.

Global Infrastructure Copper Projects: Mega-Project Pipeline

The pipeline of global infrastructure copper projects reflects the scale of investment required to meet growing demand, with significant capital commitments across multiple jurisdictions.

Major Development Projects

Key projects advancing towards production include:

- El Pachón (Argentina): Glencore/Yamana joint venture targeting 1 million tonnes annual copper by mid-2030s

- Agua Rica (Argentina): Part of integrated Glencore development strategy

- Quellaveco expansion (Peru): Anglo American evaluating capacity increases

- Resolution Copper (Arizona): Rio Tinto’s major US development project

Capital Investment Requirements

The total expansion capex for copper projects from 2025-2034 is estimated at approximately USD 250 billion, representing a significant increase from the previous decade’s USD 150 billion spend.

Technology Innovations Reshaping Base Metals Mining

The base metals mining sector is undergoing a technological revolution that’s enhancing productivity and reducing environmental impact across LSE and TSXV copper and nickel companies. These innovations are particularly crucial as miners face declining ore grades and increasing operational complexity.

Digital Mining and Automation

Advanced automation technologies are transforming traditional mining operations:

- Autonomous vehicles: Rio Tinto’s Kennecott operation uses AI-powered ore sorting systems, increasing average mill feed grade by 0.18 percentage points compared to the previous year

- Predictive maintenance: IoT sensors and machine learning algorithms reduce unplanned downtime by up to 30%

- Remote operations: Digital twin technology enables real-time monitoring and optimisation of complex mining processes

Processing Technology Advancements

Metallurgical innovations are improving recovery rates and reducing processing costs:

- Heap leaching optimisation: New bacterial leaching techniques increase copper recovery from low-grade ores

- Nickel processing innovations: Advanced pressure leaching technologies improve nickel extraction rates from lateritic ores

- Waste-to-resource conversion: Enhanced recycling technologies enable secondary metal recovery from tailings and industrial waste

Environmental and Sustainability Imperatives

The transition to sustainable mining practices has become a competitive advantage for leading base metal miners UK and Canada, with ESG considerations increasingly influencing investment decisions and project approvals.

Carbon Footprint Reduction

Mining companies are implementing comprehensive decarbonisation strategies:

- Renewable energy adoption: Anglo American’s Quellaveco operates entirely on renewable power, demonstrating feasibility of green mining operations

- Electrification of mobile equipment: Battery-electric haul trucks and drilling equipment reduce diesel consumption and emissions

- Carbon capture initiatives: Pilot projects exploring mineral carbonation for permanent CO2 sequestration

Water Management and Conservation

Water scarcity challenges are driving innovation in water management:

- Desalination projects: Collahuasi’s USD 1.3 billion desalination plant will provide 1,050 litres per second via 194-kilometre pipeline

- Closed-loop systems: Advanced water recycling technologies achieving 95%+ water recovery rates

- Dry processing methods: Air separation and dry grinding technologies reducing water requirements

Biodiversity and Land Stewardship

Progressive rehabilitation and biodiversity conservation programs include:

- Progressive rehabilitation: Concurrent restoration of mined areas using native species and ecosystem restoration techniques

- Biodiversity offsets: Strategic conservation programs protecting critical habitats equivalent to mining footprints

- Community partnerships: Indigenous and local community collaboration in environmental monitoring and land management

Regional Market Dynamics and Trade Flows

The global base metals trade is increasingly influenced by regional policy initiatives and supply chain localisation efforts, creating new opportunities for UK and Canadian mining stocks 2025.

North American Supply Chain Integration

The USMCA trade agreement and critical minerals policies are reshaping North American metal flows:

- Buy American provisions: Infrastructure spending prioritising domestic and allied nation sources

- Critical minerals partnerships: Canada-US cooperation on battery supply chain development

- Nearshoring trends: Manufacturing relocation driving regional metal demand growth

European Green Deal Impact

EU climate policies are creating substantial metal demand increases:

- REPowerEU program: EUR 300 billion investment driving renewable energy metal requirements

- European Battery Alliance: Domestic battery manufacturing creating nickel demand concentration

- Critical Raw Materials Act: Strategic autonomy objectives supporting non-Chinese supply sources

Asia-Pacific Growth Dynamics

Continued industrialisation and urbanisation across Asia-Pacific regions maintain strong base metals demand:

- India’s infrastructure boom: National Infrastructure Pipeline creating sustained copper demand

- ASEAN manufacturing growth: Electronics and automotive production driving metal consumption

- Japan’s energy transition: Offshore wind development requiring substantial copper inputs

Advanced Market Analysis and Price Projections

Copper Market Fundamentals

Current copper market dynamics reflect complex supply-demand interactions:

Supply Side Analysis:

- Mine depletion: Existing operations facing grade decline averaging 0.5% annually

- Capital intensity: New project development costs increasing 40% over past decade

- Geopolitical risks: Concentration in Chile, Peru, and DRC creating supply vulnerability

Demand Projections:

- Energy transition: IEA estimates copper demand growth of 50% by 2040 in net-zero scenarios

- Grid modernisation: Smart grid investments requiring 25% higher copper intensity per MW installed

- Industrial automation: Manufacturing digitalisation creating additional wiring and component demand

Price Outlook:

- Short-term: Surplus of 200,000 tonnes in 2025 creating downward pressure

- Medium-term: Balanced markets by 2027-2028 as new supply matches demand growth

- Long-term: Structural deficit emerging post-2030 supporting price appreciation

Nickel Market Transformation

The nickel market is undergoing fundamental restructuring driven by battery demand evolution:

Supply Evolution:

- Indonesian dominance: NPI production growth creating downward pressure on traditional nickel

- Class I supply constraints: Limited high-purity nickel availability for battery applications

- Recycling emergence: Secondary supply reaching 15% of total nickel consumption by 2030

Battery Chemistry Transitions:

- LFP growth: Lithium iron phosphate batteries reducing nickel intensity per vehicle

- NCM evolution: Higher nickel content cathodes increasing unit consumption

- Solid-state batteries: Next-generation technologies potentially altering nickel requirements

Investment Strategies and Portfolio Positioning

Risk-Return Optimisation

Successful base metals investment requires careful balance of risk factors:

Large-Cap LSE Positions:

- Diversification benefits: Multi-commodity exposure reducing single-metal volatility

- Dividend sustainability: Established cash flow generation supporting income strategies

- Currency hedging: Natural USD revenue hedge for GBP-based investors

TSXV Growth Opportunities:

- High-beta exposure: Junior miners offering leveraged upside to commodity price movements

- Discovery potential: Exploration success creating substantial value appreciation

- Takeover premiums: Acquisition activity by major miners supporting valuations

Sector Rotation Strategies

Optimal positioning across the base metals cycle:

Early Cycle (Current Phase):

- Overweight exploration: TSXV juniors with quality projects and strong management

- Selective development: Companies with shovel-ready projects and financing secured

- Technology leaders: Miners implementing operational efficiency improvements

Mid Cycle (Projected 2026-2028):

- Production growth: Companies ramping new operations with improving margins

- Infrastructure beneficiaries: Miners serving charging infrastructure and grid expansion

- ESG leaders: Premium valuations for sustainable operation practices

Late Cycle (Post-2030):

- Cash generation: Established producers with low-cost, long-life assets

- Consolidation plays: Strategic positions in acquisition targets

- Dividend sustainability: Companies with robust balance sheets and cash flow visibility

Emerging Trends and Future Catalysts

Battery Technology Evolution

Next-generation battery technologies will reshape nickel demand patterns:

- Lithium-metal anodes: 22% higher lithium demand but reduced graphite requirements

- All-solid-state batteries: Potential for higher nickel intensity in premium applications

- Alternative chemistries: Sodium-ion and other technologies creating demand uncertainty

Circular Economy Integration

Recycling and secondary supply development:

- Urban mining: Extraction of metals from electronic waste and end-of-life infrastructure

- Closed-loop systems: Manufacturer take-back programs reducing primary metal requirements

- Recycling technology: Advanced sorting and processing enabling higher recovery rates

Geopolitical Supply Chain Restructuring

Strategic competition driving supply chain reconfiguration:

- Friend-shoring initiatives: Allied nation cooperation on critical mineral security

- Strategic stockpiling: Government reserves supporting supply chain resilience

- Industrial policy coordination: Coordinated investment in processing and manufacturing capacity

Risk Management and Due Diligence

Operational Risk Assessment

Key factors for evaluating mining investments:

Technical Considerations:

- Resource confidence: JORC/NI 43-101 compliance and reserve classification

- Metallurgical complexity: Processing requirements and recovery rate projections

- Infrastructure access: Transportation, power, and water availability

Financial Analysis:

- Capital intensity: Upfront investment requirements and funding availability

- Operating cost structure: Cash cost positioning relative to industry quartiles

- Sensitivity analysis: Price assumptions and scenario planning

ESG Integration:

- Environmental permits: Regulatory approval status and compliance track record

- Community relations: Social licence to operate and stakeholder engagement

- Governance standards: Management experience and board independence

Portfolio Construction Guidelines

Effective base metals portfolio allocation:

Geographic Diversification:

- Jurisdiction risk: Balanced exposure across mining-friendly jurisdictions

- Currency exposure: Natural hedging through multi-currency revenue streams

- Political stability: Preference for established regulatory frameworks

Asset Stage Diversification:

- Production (40-50%): Established operations with predictable cash flows

- Development (30-40%): Advanced projects with defined timelines and funding

- Exploration (10-20%): Early-stage opportunities with discovery potential

Also Read: Pacgold Limited Reports Strong Gold Drilling Results at Alice River Project

Conclusion: Seizing the Base Metals Opportunity

The convergence of electrification, decarbonisation, and digitalisation creates an unprecedented growth opportunity for LSE and TSXV copper and nickel companies. Success will require strategic positioning across the value chain, from exploration through production, while maintaining focus on operational excellence and sustainable practices.

LSE copper producers Anglo American, Glencore provide institutional-quality exposure to the copper super-cycle through their diversified asset portfolios and strategic market positioning. Their operational scale, financial resources, and technical expertise position them to capitalise on growing EV charging copper demand and renewable energy metals outlook.

TSXV nickel juniors Canada 2025 offer compelling risk-adjusted returns through focused exposure to battery minerals in stable jurisdictions. Companies like Power Nickel, Canada Nickel, and Talon Metals demonstrate the potential for substantial value creation through resource development and strategic partnerships.

The industrial growth copper nickel theme represents a multi-decade investment opportunity driven by fundamental economic transformation. While commodity cycles will create periodic volatility, the underlying demand drivers remain robust and continue strengthening as the global economy transitions towards electrification and sustainability.

For investors seeking exposure to these transformational trends, the combination of established LSE producers and emerging TSXV developers provides balanced exposure to both stable cash flow generation and high-growth potential within the essential materials powering tomorrow’s economy.

Frequently Asked Questions

Q: Which are the top LSE copper producers in 2025?

A: Glencore and Anglo American lead LSE copper production with combined guidance of ~1.5 million tonnes, focusing on South American assets and strategic diversification.

Q: What are the best TSXV nickel juniors to watch in 2025?

A: Power Nickel, Canada Nickel Company, and Talon Metals lead the TSXV nickel sector with high-grade Canadian projects targeting battery supply chains.

Q: How will EV demand impact copper prices?

A: EV charging infrastructure could require an additional 100,000 tonnes of copper annually by 2027, with total EV-related copper demand potentially doubling to 2.2 million tonnes by 2030.

Q: What’s the renewable energy outlook for base metals?

A: Grid expansion for renewables requires doubling by 2040, while battery storage creates 89-fold growth in nickel demand for energy storage applications.

Q: Are UK and Canadian mining stocks good investments in 2025?

A: Both markets offer distinct advantages – UK stocks provide currency benefits and global access, while Canadian juniors offer critical minerals exposure with jurisdictional stability.