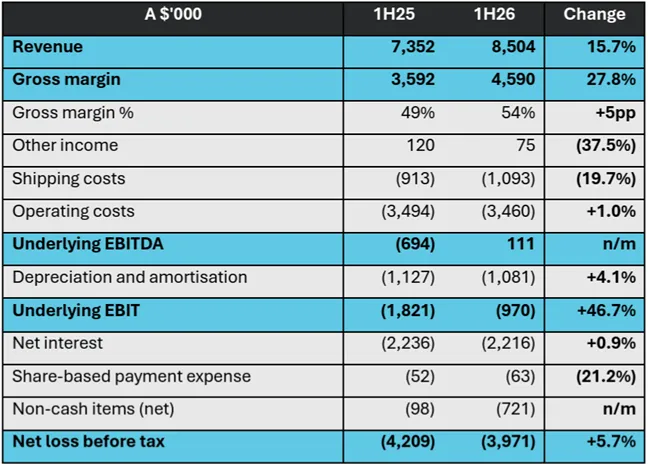

Carbonxt Group Limited (ASX: CG1), the Australian-listed activated carbon developer and manufacturer, has delivered a compelling half-year performance for the period ended 31 December 2025. Under the leadership of Managing Director Warren Murphy, the Company posted revenue of $8.50 million, a 15.7% increase on HY25’s $7.35 million, while making critical strides toward the commissioning of its flagship Kentucky production facility.

With gross margins expanding, operating cash flow turning positive, and regulatory tailwinds accelerating, Carbonxt is positioning itself firmly at the intersection of cleantech and environmental compliance.

![]()

Figure 1: Carbonxt Group Limited logo [Source: Carbonxt Group]

Warren Murphy: Driving the Strategy Forward

Warren Murphy has been the driving force behind Carbonxt’s disciplined growth strategy. As Managing Director, Murphy has consistently prioritised a combination of pricing discipline, improved product mix, and deliberate capital deployment — qualities that show clearly in the HY26 numbers.

Figure 2: Warren Murphy, Managing Director of Carbonxt [Source: Carbonxt Group]

Commenting on the half-year result, Murphy described the performance as reflecting “a materially improved margin profile and stronger contracted sales position.” He was direct about the temporary ACP delivery disruption caused by a maintenance outage at the Black Birch facility in Georgia, confirming that those deferred volumes are being recovered under existing contracts in 2HFY26.

The Company has methodically increased its ownership in New Carbon Processing, LLC — the joint venture operating the Inez Power Activated Carbon Plant in Inez, Kentucky — from a minority stake to 47.4%, with a stated target of 50%. Each capital raise, convertible note issuance, and shareholder placement over the past 12 months has been prioritised, in part, toward locking in greater control of this strategically vital asset.

“HY26 reflects a materially improved margin profile and stronger contracted sales position compared to the prior corresponding period. Regulatory momentum from tightening US EPA PFAS standards continues to support demand across our core markets.” – Warren Murphy, Managing Director

HY26 Financial Performance: Margin Expansion Tells the Real Story

The half-year revenue figure of $8.50 million comprised $4.50 million in Q1 FY26 and $3.83 million in Q2 FY26. The softer Q2 result reflects a temporary maintenance outage at the Black Birch facility, which deferred approximately $0.9 million in Activated Carbon Pellet (ACP) deliveries. Those contracted volumes are being recovered in the current quarter.

Figure 3: Carbonxt Group Financial highlights HY26 [Source: Carbonxt Group]

Beyond the top line, the margin story is where the most meaningful progress appears:

- Gross Margin: Gross margin reached 54%, up five percentage points from 49% in the prior corresponding period — the highest margin the Company has reported in recent periods

- Positive Operating Cash Flow: Net cash from operating activities turned positive at $0.66 million for the half, compared to a net outflow in the prior period

- PAC Revenue: Powdered Activated Carbon (PAC) contributed approximately 57% of revenue, anchored by the long-term ReWorld contract

- ACP Revenue: Activated Carbon Pellets (ACP) accounted for the remaining 43%, with Q1 showing strong volume growth before the Black Birch disruption

The Kentucky Facility: The Asset That Changes Everything

The Kentucky facility is the centrepiece of the Company’s growth narrative, and HY26 brought it meaningfully closer to commercial production. During the period, the Company completed several critical commissioning milestones:

- Kiln construction was completed, and the refractory lining was heat-treated

- Back-end infrastructure — including bagging lines, conveyors, and additional storage silos — was installed and integrated

- An on-site power station was brought online to support commissioning activities

- Remediation works to support system redundancy were advanced

The Kentucky plant carries an initial capacity of 10,000 tonnes per annum, with a scalable pathway to 20,000 tonnes per annum for a modest incremental investment. Management forecasts that a fully running Kentucky facility would increase group sales by approximately 200% and provide the Company’s first meaningful entry into the liquid-phase activated carbon market — a segment three times the size of the air-phase market Carbonxt currently serves.

Figure 4: Carbonxt’s Kentucky activated carbon facility [Source: Carbonxt Group Limited]

Early product samples have already demonstrated 99% PFOA removal efficiency and 92% geosmin removal — results that position the Company competitively against established GAC suppliers in North American water treatment markets.

Following a A$500,000 convertible note issuance to major shareholder Phelbe Pty Ltd, the Company lifted its ownership in New Carbon Processing, LLC to 47.4%, with a stated target of reaching 50%. The consistency with which Phelbe has backed the Company — through multiple placements, expanded note facilities, and convertible notes — represents a meaningful signal of alignment from the major shareholder.

Why PFAS Regulation Is Reshaping the Market

PFAS — per- and polyfluoroalkyl substances, commonly called “forever chemicals” — have emerged as one of the most pressing environmental issues of the decade. These synthetic compounds do not break down naturally in the environment or in the human body, and their presence in drinking water sources has been linked to serious health risks, including certain cancers and immune system disorders.

Figure 5: PFAS or per- and polyfluoroalkyl substances [Source: Carbonxt Group]

In 2024, the U.S. Environmental Protection Agency finalised its National Primary Drinking Water Regulations for PFAS — the first time legally enforceable limits have been set on six PFAS compounds in public water supplies. The rule is expected to require thousands of water utilities across the United States to install treatment infrastructure, generating a wave of long-term activated carbon supply contracts.

The scale of this market opportunity is significant:

- Market Size: The global activated carbon market is estimated at USD 4.16 billion in 2026, forecast to reach USD 5.47 billion by 2031 at a CAGR of 5.62%

- PFAS Filtration: The global PFAS filtration market is projected to grow from USD 2.28 billion in 2025 to USD 3.22 billion by 2030 at a CAGR of 7.18%

- Market Position: Activated carbon remains the leading technology for PFAS remediation, owing to its adsorption capacity, scalability, and proven operational track record

- Regulatory Deadline: TSCA PFAS Reporting Rule obligations are expected to run from April through October 2026, intensifying compliance activity across the industry

Carbonxt’s Kentucky facility produces Granular Activated Carbon (GAC), the product of choice for liquid-phase water treatment, including PFAS removal. Murphy has acknowledged this regulatory momentum directly, noting that tightening EPA PFAS standards continue to support demand across the Company’s core markets.

Three Facilities, One Strategic Direction

Carbonxt operates three U.S.-based production facilities, each serving a distinct but complementary market:

- Black Birch, Georgia — Powdered Activated Carbon (PAC) production, serving air-phase industrial applications and the long-term ReWorld Waste supply agreement (a four-year, AUD 24 million contract)

- Arden Hills, Minnesota — Activated Carbon Pellet (ACP) manufacturing, serving the Wisconsin Public Service contract and other industrial clients (a seven-year agreement)

- Inez, Kentucky — Granular Activated Carbon (GAC), targeting liquid-phase water treatment and PFAS removal — the Company’s growth engine

Figure 6: Map of the United States highlighting the three Carbonxt production facility locations [Source: Carbonxt Group]

The Kentucky facility is the growth engine. The Georgia and Minnesota operations provide a stable, contracted revenue foundation as commissioning in Kentucky progresses. Together, the three facilities give the Company diverse exposure across both air-phase and liquid-phase activated carbon markets.

Capital Management and the Balance Sheet

The Company closed the half with cash and cash equivalents of $1.27 million as at 31 December 2025. The debt facility with Pure Asset Management sits at $15.0 million drawn at a 9.5% interest rate, with a maturity date of 31 May 2027.

To shore up its capital position, the Company executed a series of corporate actions during the half:

- Raised $587,769 via an underwritten non-renounceable entitlement offer issuing 58.8 million Loyalty Options

- Issued 11.0 million Loyalty Options to directors in lieu of $110,000 in fees

- Raised $600,000 via a placement to major shareholder Phelbe Pty Ltd at $0.075 per share

- Issued 400,000 convertible notes at $1.00 each, convertible into shares at $0.08 per share

- Secured a further A$500,000 via a convertible note issuance, directing part of the proceeds toward increasing its Kentucky joint venture stake to 47.4%

Investors’ Outlook

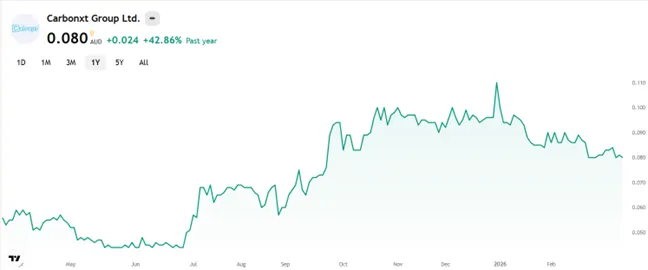

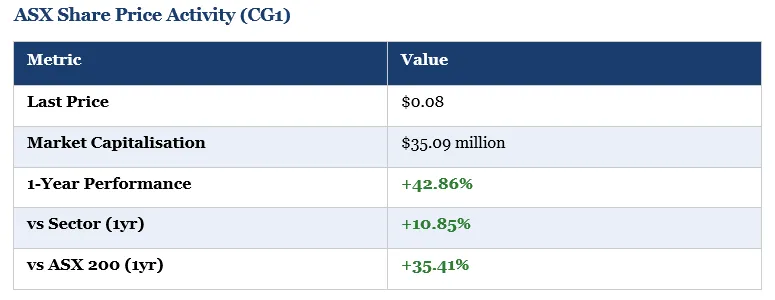

Carbonxt Group Limited (ASX: CG1) has delivered a 42.86% share price gain over the past 12 months, outperforming its sector by 10.85% and the ASX 200 by 35.41% — a result that reflects improving operational momentum and growing market interest in cleantech companies exposed to regulatory-driven demand.

Figure 7: Carbonxt share price performance in the last 12 months [Source: Colitco]

The investment case for Carbonxt rests on two key pillars. First, the commissioning of the Kentucky facility promises a potential 200% uplift in group sales capacity, marking the Company’s strategic entry into the high-growth liquid-phase activated carbon segment. Second, the anticipated recovery of deferred ACP volumes in Q3 FY26 provides near-term revenue momentum, strengthening the outlook for H2 results.

With a lender waiver secured until September 2026, the Company has a clear runway to translate operational milestones into financial performance. Warren Murphy’s methodical, margin-focused leadership continues to anchor a business positioned for a transformative step-change in scale.

As PFAS regulations tighten across North America, the demand for GAC—the primary output of the Kentucky plant—is intensifying. For investors, Carbonxt represents a compelling opportunity at the forefront of this environmental transition, with its growth story gaining significant traction.

Disclaimer: This editorial is for informational purposes only and does not constitute financial product advice. Readers should seek independent financial advice before making any investment decisions.

Tags: Activated Carbon, ASX: CG1, Carbonxt Group Last modified: March 26, 2026

{kind=link}