The first half of FY26 in Botanix Pharmaceuticals Limited presented a high level of performance as its products have increased demand and sales activity. On 3 March 2026, the company released its Half-Year Investor Update 2026.

Sofdra® uptake and execution were executed throughout performance in its fulfilment model. The gross and net revenue were 93.5m and 21.2m, respectively, in the initial 11 months of launch. 62,500 prescriptions had been shipped.

According to management, the sales force and fulfilment operations exceeded the expectations of management. There was also improved platform scalability and operational discipline that was observed by investors.

These Botanix 2026 financial outcomes highlight a business that has just begun its transition to the commercial scale of business.

Botanix laboratory and fulfilment operations supporting Sofdra® distribution. [LinkedIn]

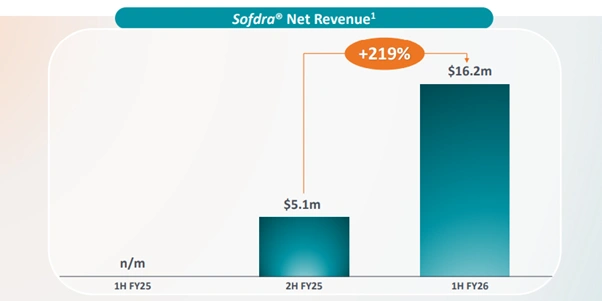

What Powered Botanix’s Half-Year Results And Sales Expansion?

The most important performance driver in the half was prescription growth. The shipments of Sofdra 1 H FY26, which is TRx, have gone up 171%. Shipments increased by 16.8k to 45.8k volumes.

The net revenue was also increasing according to demand. Sofdra’s net revenue increased by 219% to get to $16.2m. This was a positive indication of more growth in the future by healthcare professionals.

According to the survey information, 90 per cent of participants anticipate that in the next six months, they will become more prescribers. Most of them quoted convenient insurance clearance and home delivery preference by the patient.

SendRx access was rated highly on satisfaction. Such measures reflect the existence of a long-term trend and not demand peaks.

Sofdras’ revenue upsurge. [ASX]

Sofdra Platform Execution Strengthens Commercial Foundation

Botanix insisted that the fulfilment platform will continue to be the key point of its strategy. The system enhances patient adherence and gross-to-net yields. The fill rates have been cited at 2.5 times higher than those of the industry.

There is a high percentage of reimbursed prescriptions. Shipment to the consumer also avoids the middlemen and saves money. The network has a high refill behaviour. The management thinks that the addition of more products to the platform would not require significant development costs.

Such a scaled structure may increase profitability in the long term. The strategy makes Botanix unlike other conventional dermatology vendors. This kind of execution assists in the short-term revenue as well as the long-term margins.

Dermatology consultations and home delivery support higher prescription adherence. [Cedars Dermatology]

How Did Botanix Revenue And Profit Trends Perform?

Top-line improvement was seen to be significant in the half reflected in financial results. The total revenue was up to $16.5m as opposed to $346k in the past. Materials and other related costs amounted to $6.0m.

Direct Opex was $36.6m. Adjusted EBITDA came in at ($26.1)m. There was cash and cash equivalents of $31.6m. Costs were incurred on sales and marketing of products and employee benefits of 24,745k and 7,037k, respectively.

Consulting and administration at corporations were still in check. The loss before income tax expense was (-33,195) as compared to (-30,888). Although the loss occurred, the management emphasised that revenue growth should be a priority.

The trends in Botanix revenues and profits are thus expected to invest in the current to scale in the future.

Capital Raising And Supply Strategy Support Stability

The company had strong commitments of A$45 million capital raising before expenses. The money will help in buying API and producing parts. The API supply is approximately $12 million.

An alternate API supplier arrangement is provided with approximately 4 million. The advertising and marketing programs come to about $13.5 million. OpeX and working capital amount to approximately 13 million. Transaction costs are approximately 2.5 million.

Another supplier is also being negotiated by Botanix to cut the COGS by 25-40. This would address the single-source risk. According to management, these measures make it resilient and increase gross profit in the future.

Funding and supply chain agreements are designed to secure long-term production. [ET Edge Insights]

What Catalysts Could Shape Botanix Financial Results 2026 Next?

There are a number of operational catalysts that will occur in the coming reporting period. The management will provide further Sofdra growth. Other products can be inserted on the fulfilment platform. Expansion into other regions is still under consideration.

The term of patent protection is 2040 in support of higher-value. There are now 50 representatives who push the sales force in the form of demand.

The level of physician satisfaction is high, so there is continued uptake. Margins would also be improved through API diversification.

All these measures are intended to increase the stability of revenue. Botanix’s financial results for 2026 are therefore based on action and not conjecture. The company seems to be geared towards hardcore and quantifiable growth.

Also Read: Neuren Pharmaceuticals ASX: Investor Presentation 2026 Highlights

FAQs

Q1. What are Botanix’s financial results for 2026 highlights?

A1: Revenue reached $16.5m, and prescriptions increased 171% in 1H FY26.

Q2. How many Sofdra® prescriptions were shipped?

A2: 62,500 prescriptions were shipped in the first 11 months of launch.

Q3. What capital raising was completed?

A3: Botanix secured firm commitments for A$45 million before costs.

Q4. How could costs improve going forward?

A4: An alternate API supplier may reduce COGS by 25% – 40%.