Copper is having a moment. From record prices on the London Metal Exchange to a stampede of institutional capital rotating into the red metal, the structural bull case for copper has never been more compelling. Against this backdrop, an ASX explorer is quietly assembling a portfolio of copper assets in one of Asia’s most prospective jurisdictions, and the market appears to have barely noticed.

Asian Battery Metals PLC (ASX: AZ9) currently trades at a market capitalisation of roughly $12.1 million, yet it holds a growing cluster of copper, copper-nickel, and copper-gold projects in southwest Mongolia. The Company also boasts metallurgical results that would make a mid-tier producer envious.

Figure 1: Image of mining equipment at the Oval Cu-Ni-PGE Project site. [Source: Asian Battery Metals]

The Copper Supercycle Is No Longer a Theory

The copper market has undergone a dramatic transformation over the past 18 months. What began as a debate about energy transition demand has morphed into a full-blown supply crisis, pushed further by mine disruptions, tariff-driven stockpiling, and a structural deficit that multiple major banks now treat as a baseline assumption, not a tail risk.

Where Copper Prices Stand Today

- Copper hit a record high of $11,771 per tonne on the LME in December 2025 — its highest level in history

- A separate record of $13,387 per tonne was set in January 2026 on the back of tariff-driven pre-emptive buying

- J.P. Morgan Global Research forecasts copper averaging ~$12,075/t for full-year 2026, peaking at $12,500/t in Q2 2026

- BMI (a Fitch Solutions company) maintains a 2026 average forecast of $11,000/t, citing tightening supply and net-zero transition demand

- Goldman Sachs Research projects the LME copper price will reach $15,000 per tonne by 2035

The Demand Drivers Are Structural and Compounding

- Grid and power infrastructure will drive more than 60% of copper demand growth to 2030, per Goldman Sachs — effectively adding another United States of copper consumption

- Wood Mackenzie forecasts copper demand will rise 24% to 43 million MT per year by 2035 — requiring 8 million MT of new primary supply plus 3.5 million MT from scrap

- Data centre demand alone could reach 475,000 tonnes in 2026 — up ~110,000 tonnes on 2025 — as AI hyperscale facilities each require up to 50,000 tonnes of copper

- Battery EVs require 53.2 kg of copper per vehicle — more than double the 22.3 kg in a conventional car

- BloombergNEF warns copper may enter structural deficit as early as 2026, with a cumulative gap of 19 million tonnes by 2050 without new supply

The International Copper Study Group forecasts refined copper use will grow 2.1% to 28.73 million MT in 2026, outpacing production and creating a 150,000 MT deficit by year-end. The world needs more copper — and it needs it urgently. The projects entering the development pipeline today will command enormous strategic value in the decade ahead.

Gan-Ochir Zunduisuren: The Friedland Playbook, Applied in Mongolia

Figure 2: Gan-Ochir Zunduisuren, Managing Director of Asian Battery Metals, at JMM Conference. [Source: Asian Battery Metals / JMM Conference]

Before assessing the assets, it is worth understanding the person building the Company. Managing Director Gan-Ochir Zunduisuren brings more than 20 years of hands-on mining experience in Mongolia — from grassroots exploration through to underground production — and his career trajectory reads like a blueprint for what a world-class copper developer looks like in this part of the world.

The Oyu Tolgoi Connection

Critically, Gan-Ochir served on the board of Oyu Tolgoi — the mega-copper mine in Mongolia’s South Gobi that became the country’s defining mining project. Oyu Tolgoi was the flagship discovery of the Ivanhoe Mines group, led by legendary copper billionaire Robert Friedland.

Friedland founded Ivanhoe Mines (originally Indochina Goldfields) in 1994. Exploration since 2000 uncovered a chain of copper, gold and silver deposits at Oyu Tolgoi, with first commercial production commencing in 2013. The Mongolian President awarded Friedland the Order of the Polar Star — the country’s highest civilian honour for a foreign citizen — for his leadership in what became one of the largest known copper and gold deposits in the world.

The Ivanhoe group’s approach to exploration became a masterclass in building land packages aggressively around a discovery and pursuing all geological neighbours systematically. Gan-Ochir absorbed that philosophy directly. It now shapes how he runs Asian Battery Metals.

“I’m a person who started the company — for me it’s essential to the company to be successful. I’m not here just for one project. I’m trying to build a company here. The success of the company is very important. I’m one of the largest shareholders, and combined board and the large shareholders we probably own 50% of the shares in the company, and we are there to deliver the value.” — Gan-Ochir Zunduisuren, Managing Director

This is not a project-flipping exercise. This is a long-term Company-building effort from a founder with skin in the game, deep local knowledge, and a network forged in one of the most consequential copper discoveries of the modern era.

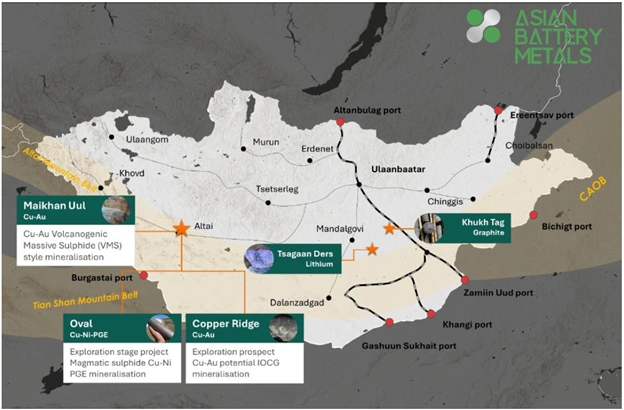

The Portfolio: Three Copper Opportunities in One Tight Geographic Belt

Figure 3: Project locations map of Asian Battery Metals [Source: Asian Battery Metals]

Asian Battery Metals holds its assets in the southwestern corner of Mongolia — an emerging mining district that sits on the same Central Asian Orogenic Belt that hosts world-class deposits across Kazakhstan, Russia, Mongolia and China. The Company operates three discrete but geographically clustered opportunities, all serviced by the same infrastructure, the same logistics chain, and the same gateway to the Chinese copper processing market.

“The southwestern part of Mongolia is really an emerging mining district. It’s the same belt — the Central Asian Orogenic Belt — that hosts a number of rich metal deposits in Kazakhstan, Russia, Mongolia and China. So that’s where we are working.” — Gan-Ochir Zunduisuren, Managing Director

1. Oval Cu-Ni-PGE Project: The Flagship Discovery

The Oval Copper-Nickel-Platinum Group Elements Project, anchored within the Company’s 100%-owned Yambat Project, is the asset that first put AZ9 on the map — and for very good reason.

The story of Oval’s discovery begins with BHP. In 2023, when the Company was still a private enterprise, it applied to BHP’s global exploration accelerator programme and was selected as one of only seven companies globally — and the sole entrant from the Asia-Pacific region. Using BHP’s funding, the team made a discovery at what is now the Oval Cu-Ni-PGE Project. The Company subsequently listed on the ASX in 2024.

Key Drilling Highlights

- OVD020: 19.5m @ 1.61% Cu, 2.15% Ni, 0.72 g/t PGE

- OVD033: 9.5m @ 3.11% Cu, 3.39% Ni, 1.27 g/t PGE

- OVD044: 8.1m @ 3.24% Cu, 1.64% Ni from 239.0m

- OVD051: 9.3m @ 1.06% Cu, 0.48% Ni — confirms North Oval extension

- OVD049: 16.8m @ 0.39% Cu, 0.41% Ni — confirms southeast extension

Phase 3 drilling extended Oval’s mineralisation to 880 metres of total strike length — a 60% increase on the previously known footprint. The system remains open along strike and at depth, with new geophysical targets including the newly identified MS4 magnetic anomaly suggesting additional undrilled intrusive bodies nearby.

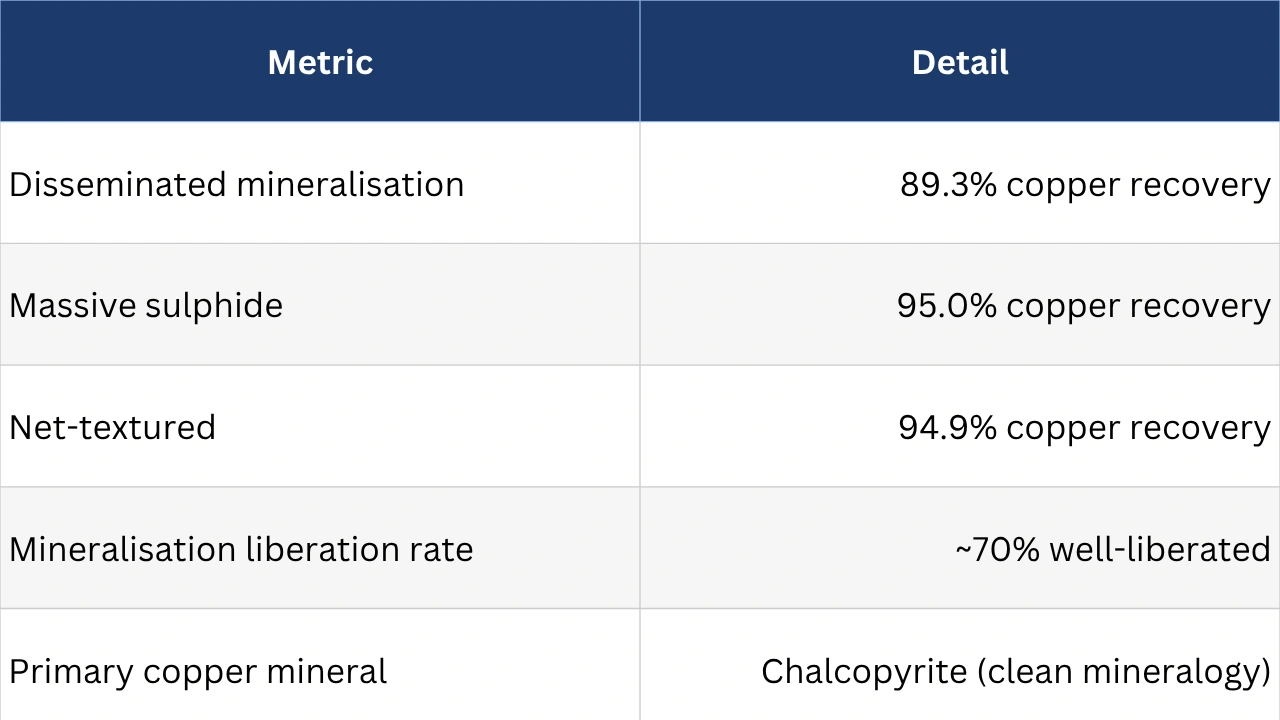

Metallurgical Results

Metallurgical test work completed at ALS Metallurgy in Perth returned copper recoveries of 89–95% across all three composite sample types — results that de-risk the processing pathway significantly:

Approximately 70% of the mineralisation is well-liberated, indicating straightforward and potentially low-cost processing characteristics. Chalcopyrite is confirmed as the sole copper-bearing mineral — a clean mineralogy that reduces metallurgical complexity for any future flowsheet design.

For our detailed coverage of the Oval project’s exploration breakthroughs, see: Asian Battery Metals Delivers Major Exploration Breakthroughs at Oval Cu-Ni-PGE Project

2. Maikhan Uul Cu-Au VMS Project: The Option Exercised

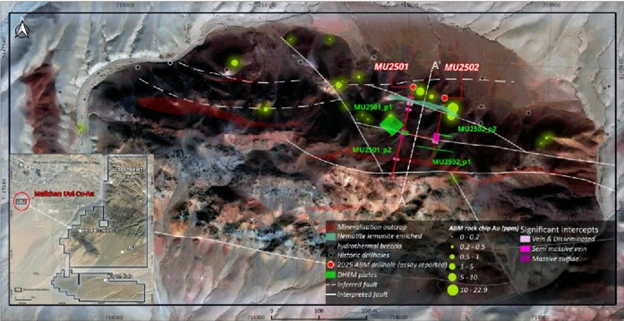

In March 2026, the Company formally exercised its option to acquire the Maikhan Uul Copper-Gold VMS (Volcanogenic Massive Sulphide) Project — a significant corporate milestone that reflects management’s conviction in the quality of what their due diligence drilling uncovered.

Figure 4: Drillhole location map for Maikhan Uul Cu-Au Project showing drill collar positions, rock chip sample locations, and strike direction. [Source: Asian Battery Metals]

Due Diligence Drilling Highlights — Drill Hole MU2501

Strongly mineralised massive sulphide zones:

- 14.5m @ 2.23% Cu and 0.73 g/t Au from 132.5m, including:

- 4.8m @ 2.80% Cu and 0.88 g/t Au from 132.5m

- 6.3m @ 2.58% Cu and 0.82 g/t Au from 139.7m

- 2.6m @ 2.28% Cu and 0.49 g/t Au from 154.1m

Shallow high-grade gold and silver mineralisation:

- 5.2m @ 6.54 g/t Au and 126.40 g/t Ag from 36.9m, including:

- 2.1m @ 13.33 g/t Au and 227.81 g/t Ag from 37.9m

- 4.8m @ 2.02 g/t Au and 35.39 g/t Ag from 28.2m

The historic resource at Maikhan Uul stands at 5 million tonnes — but the key drill hole was positioned below that resource, meaning significant upside exists both above the existing historical resource horizon and at depth. The massive sulphide lens continues at depth and along strike. Exercising the option locks in what the Company considers one of the most strategically located high-grade copper-gold assets in the southwestern Mongolian belt.

3. Shallow Gold Prospect: A High-Grade Bonus

Sitting directly adjacent to the Maikhan Uul Cu-Au Project is a shallow gold prospect confirmed in the back half of 2025. Intercepts include a combined 10 metres grading approximately 4–5 g/t gold, with a high-grade core of 3 metres at 13 g/t gold.

Surface sampling has already delineated a 100-by-600-metre anomalous zone, with individual samples returning up to 22 g/t gold. The zone remains open to the west.

Why Mongolia? A Jurisdiction That Has Matured Beyond Its Reputation

Mongolia’s reputation as a complex jurisdiction has historically deterred some institutional capital. But that narrative is increasingly at odds with the operating reality on the ground — and the macro fundamentals now actively support it.

“Some say Mongolia has an unstable government. Yeah, we are a democracy. So we change as much as we would like to, when we would like to. On average, a Mongolian government lasts 1.9 years — which is the same as Australia. So it’s not much difference there, guys.” — Gan-Ochir Zunduisuren, Managing Director

The Numbers Tell Their Own Story

- Mongolia ranks in the top five for mineral prospectivity in Asia

- The country sits in the top five on the Global Peace Index for the Asia-Pacific region

- S&P Global Ratings upgraded Mongolia’s sovereign credit rating to BB- in Q4 2025 — its first BB category rating — citing a falling debt-to-GDP ratio forecast at 31.2%

- Oyu Tolgoi’s underground expansion drove a 45% increase in copper export volumes in 2025, strengthening Mongolia’s fiscal position

- The Company can obtain exploration permits and begin field programmes within 30 days of a new tenement grant

The proximity to China is also a core competitive advantage that tends to be underappreciated by markets focused on Western jurisdictions. China is the world’s largest refiner and downstream processor of copper, and Mongolia sits on its doorstep. Every tonne of copper concentrate that AZ9 eventually produces will benefit from freight and logistics costs that would be the envy of producers in South America or sub-Saharan Africa.

For our detailed overview of the Company’s broader portfolio context and market positioning, see: Asian Battery Metals Advances Multi-Commodity Portfolio with Strong Drilling Results

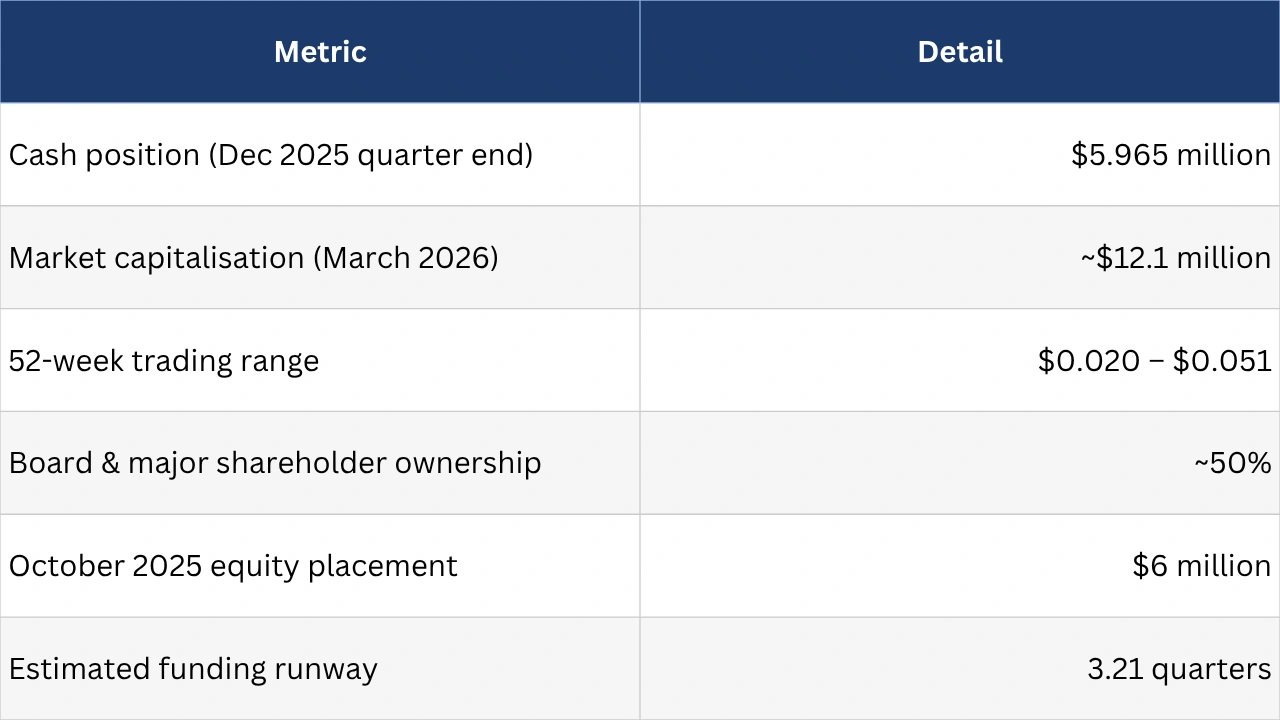

The Balance Sheet: Funded and Ready to Drill

The Company closed the December 2025 quarter with $5.965 million in cash, providing an estimated 3.21 quarters of planned expenditure coverage. This follows a successful $6 million equity placement completed in October 2025, supported by institutional investors including LA Resource Fund (Melbourne) and Dragon Tree Capital (Melbourne).

The aligned shareholder base — with the board collectively owning around half the Company — removes much of the dilution risk that plagues smaller explorers and ensures management incentives are directly tied to share price performance.

The Undervaluation Argument: What the Market Is Missing

At a market capitalisation of approximately $12.1 million, Asian Battery Metals trades at a fraction of the value implied by its asset base, its exploration results, and the copper price environment in which it operates. Consider the following:

- Oval Cu-Ni-PGE Project: An 880-metre mineralised system with copper recoveries of 89–95%, confirmed high-grade massive sulphide zones, and multiple untested geophysical targets. A comparable discovery in a Tier 1 jurisdiction would typically command a market cap measured in the hundreds of millions as it approaches resource definition.

- Maikhan Uul Cu-Au Project (now acquired): A high-grade VMS system with a historic 5-million-tonne resource, confirmed deep copper-gold mineralisation, and a shallow gold/silver zone that independently tests as economic-grade.

- Shallow gold prospect: A 100-by-600-metre anomalous zone grading up to 22 g/t at surface, open to the west, and untested at meaningful depth.

- Copper pricing tailwind: With J.P. Morgan targeting $12,500/t by Q2 2026 and Goldman Sachs projecting $15,000/t by 2035, the valuation multiple the market assigns to copper in the ground will expand materially as forecasts are validated.

- Operator pedigree: A founder-led team with decades of Mongolian mining experience, whose MD personally served on the board of Oyu Tolgoi — perhaps the most significant copper development achievement of the past two decades in Asia.

What to Watch: Key Catalysts for 2026

Figure 5: Drilling rig on-site at the Oval project area in Mongolia. [Source: Asian Battery Metals]

The Company has outlined a clear and near-term catalyst pipeline that gives investors specific milestones to watch:

- Phase 4 drilling at Oval Cu-Ni-PGE: Planning and permitting underway for Q1–Q2 2026, targeting the MS4 magnetic anomaly and other FLEM/DHEM geophysical targets

- Updated 3D geological model at Oval: Integrating all Phase 3 data for a tighter vector on resource definition

- Shallow gold fieldwork at Maikhan Uul: Systematic follow-up of the 100-by-600-metre surface anomaly grading up to 22 g/t gold

- Copper-gold drilling at Maikhan Uul: Expanding the confirmed deep massive sulphide zones both down-dip and along strike

- Overall copper resource definition: The stated 2026 goal is to establish a thorough understanding of the total copper potential across the entire portfolio

At ~$12 million in market capitalisation, the Company offers leveraged exposure to what could be one of the more significant copper development stories to emerge from the ASX in the current cycle. The copper macro is aligned. The jurisdiction has matured. The results are real. The Managing Director’s leadership and direct experience with Oyu Tolgoi provide the strategic expertise required to navigate this landscape.

Disclaimer

This article is provided for informational and educational purposes only and does not constitute financial product advice. The information presented has not taken into account your personal objectives, financial situation, or needs. Past performance is not a reliable indicator of future results. Readers should seek independent financial advice before making any investment decision.