Australia and New Zealand Banking Group Limited (ASX:ANZ) has released its Registered Bank Disclosure Statement for the New Zealand branch for the year ended 30 September 2025. The financial results reflect the bank’s ongoing operational performance and risk management in the current economic environment.

ANZ Bank’s headquarters at 833 Collins Street in Melbourne

Financial Performance Overview

ANZ New Zealand recorded a profit after tax of NZ$2.581 billion for the year, up from NZ$2.132 billion in 2024. This increase was driven by a rise in profit before income tax, which grew to NZ$3.596 billion from NZ$2.978 billion the previous year. The bank’s operating income rose to NZ$5.385 billion, growing from NZ$4.783 billion in 2024, supported by higher net interest income and other operating income streams.

Net interest income increased to NZ$4.473 billion, up from NZ$4.316 billion, despite a decrease in interest income from NZ$11.933 billion to NZ$10.548 billion. Interest expense decreased significantly to NZ$6.075 billion from NZ$7.617 billion. Other operating income nearly doubled to NZ$912 million from NZ$467 million, supported by increased foreign exchange earnings and trading securities income.

Operating expenses rose modestly to NZ$1.814 billion from NZ$1.761 billion, with personnel costs reaching NZ$1.104 billion. The bank reported a credit impairment release of NZ$25 million, improving from a charge of NZ$44 million in 2024, indicating asset quality enhancements.

A significant rise was seen in ANZ Group’s share prices after its statement release

Balance Sheet and Capital Position

ANZ’s total assets increased to NZ$210.267 billion from NZ$199.466 billion, driven mainly by growth in net loans and advances, which rose to NZ$158.964 billion from NZ$151.963 billion. Investment securities also increased to NZ$16.458 billion from NZ$13.295 billion.

Deposits and other borrowings increased to NZ$156.172 billion, while debt issuances slightly rose to NZ$17.766 billion. Shareholders’ equity strengthened to NZ$17.518 billion from NZ$16.527 billion, reflecting retained earnings and reserves growth.

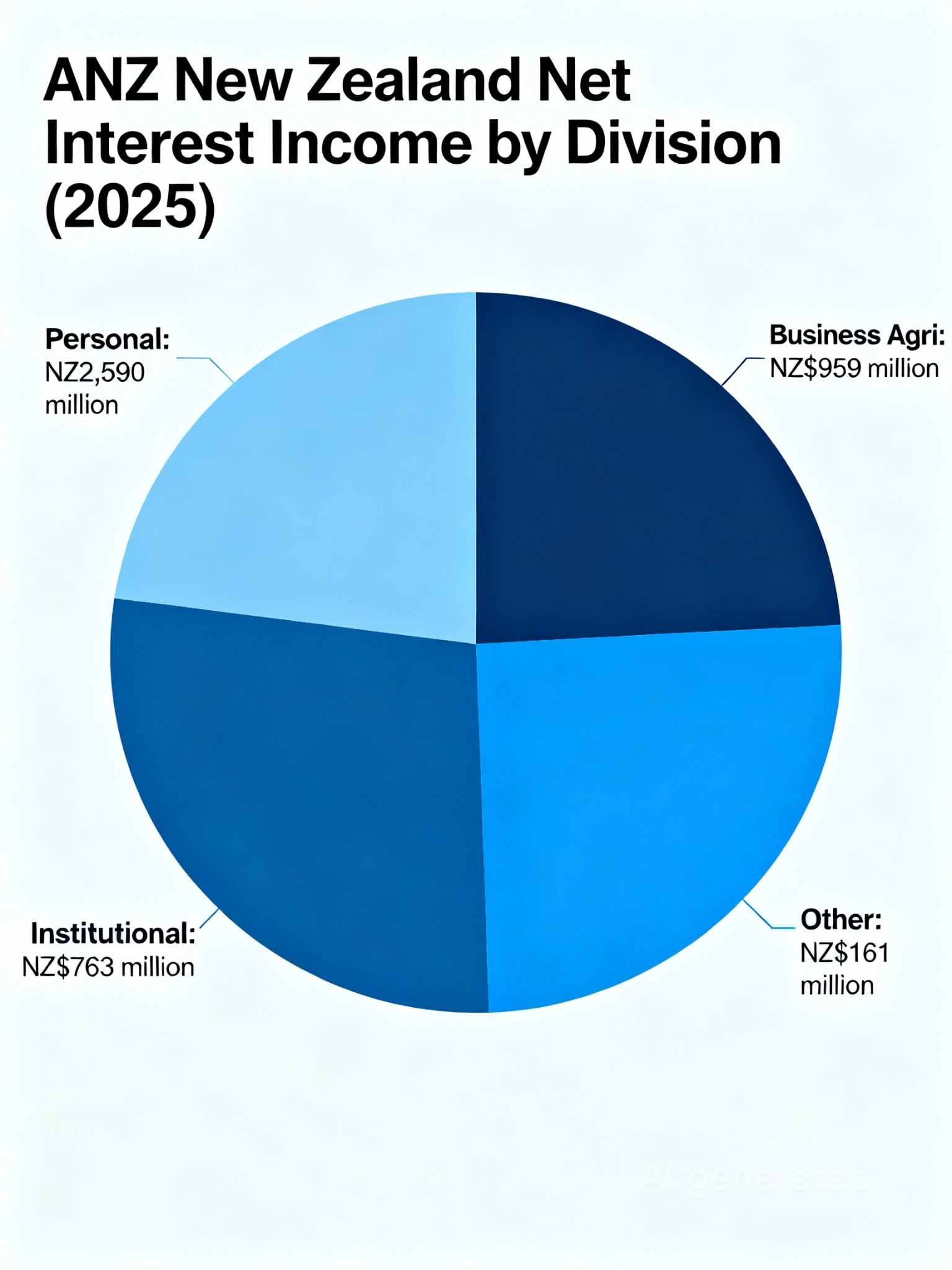

Segment Performance

The bank operates through three main segments: Personal, Business & Agri, and Institutional. The Personal segment, which includes consumer and private banking, generated NZ$2.590 billion in net interest income. Business Agri delivered NZ$959 million, and Institutional operations contributed NZ$763 million. These segments collectively supported strong profitability before tax.

Fee and commission income remained steady at NZ$1.006 billion, with lending fees at NZ$21 million and non-lending fees at NZ$713 million. Funds management income held firm at NZ$244 million.

ANZ New Zealand net interest income distribution across business segments in 2025

Credit Risk and Asset Quality

ANZ New Zealand manages credit risk through a comprehensive framework overseen by the Board Risk Committee. The bank applies internal credit rating systems and maintains stringent exposure limits. Total maximum exposure to credit risk reached NZ$236.125 billion, up from NZ$223.692 billion, supported by collateral covering the majority of net loans and other financial assets.

Provisioning for expected credit losses remained conservative, and the bank continues to monitor economic uncertainties, including impacts from geopolitical tensions and climate change.

Market and Liquidity Risk Management

The bank employs robust risk management practices across market and liquidity risks. It uses various derivative instruments to hedge foreign exchange, interest rate, commodity, and credit risks. These include forwards, futures, swaps, and options.

Derivative assets held for trading increased to NZ$11.432 billion, while liabilities reduced to NZ$10.178 billion. The bank’s hedge accounting framework limits profit and loss volatility by effectively matching hedge instruments with underlying exposures.

ANZ New Zealand maintains high-quality liquid assets to meet liquidity needs for at least one month under stress scenarios. The bank operates above regulatory minimums, supported by a diverse funding base with total deposits of NZ$143.542 billion.

Also Read: DroneShield Withdraws $7.6 Million Order Announcement After Administrative Mix-Up

Operating Expenses and Efficiency

Operating expenses grew moderately to NZ$1.814 billion, driven mainly by increases in technology expenditure and professional fees. Personnel expenses accounted for the largest share at NZ$1.104 billion, reflecting stable staffing levels.

The bank continues to invest in technology with a focus on digital banking and operational efficiency to meet evolving customer needs.

Dividend and Capital Management

ANZ New Zealand paid NZ$1.515 billion in dividends during the year, reflecting a conservative approach to capital returns. The effective tax rate remained steady at 28.2%, with an income tax expense of NZ$1.015 billion, up from NZ$846 million.

Shareholders’ equity increased to NZ$17.518 billion due to the retained earnings and reserves movement during the period, supporting ongoing capitalisation requirements.

Conclusion

ANZ New Zealand has demonstrated steady growth in profitability, asset quality, and capital during the 2025 financial year. The bank’s diversified business model, strong balance sheet, and prudent risk management underpin its operational resilience amid economic uncertainties. Continued investments in technology and risk management position ANZ New Zealand well for sustainable future performance.