The Australian economy’s September quarter performance tells a tale of two narratives. While year-on-year growth hit its highest level since mid-2023, the quarterly figure fell short of market expectations.

According to the Australian Bureau of Statistics, the Australian gross domestic product expanded 0.4% in the third quarter of 2025. This missed economist forecasts of 0.7% growth but still pushed the annual rate to 2.1%, exceeding the revised 2% recorded in the previous quarter.

The data release, published on 3rd December 2025, presents a complex picture for policymakers and investors navigating inflation concerns and monetary policy decisions.

What Drove Q3 Growth?

Household consumption emerged as a bright spot, rising 0.6% during the September quarter. This marks a solid rebound in consumer spending, supported by earlier interest rate cuts from the Reserve Bank of Australia.

Government spending and business investment also contributed meaningfully to quarterly expansion. Public sector infrastructure projects continued providing economic support, while private businesses maintained elevated capital expenditure.

However, inventories delivered a significant blow to overall growth. Stock drawdowns subtracted 0.5 percentage points from GDP, partially offsetting the gains from consumption and investment. This large drag suggests businesses reduced stockpiles amid uncertain demand conditions.

Net trade provided minimal support, contributing just 0.1 percentage points as export growth barely outpaced import declines.

Australian economy grew 0.4% in the September quarter 2025

Household Finances Show Resilience

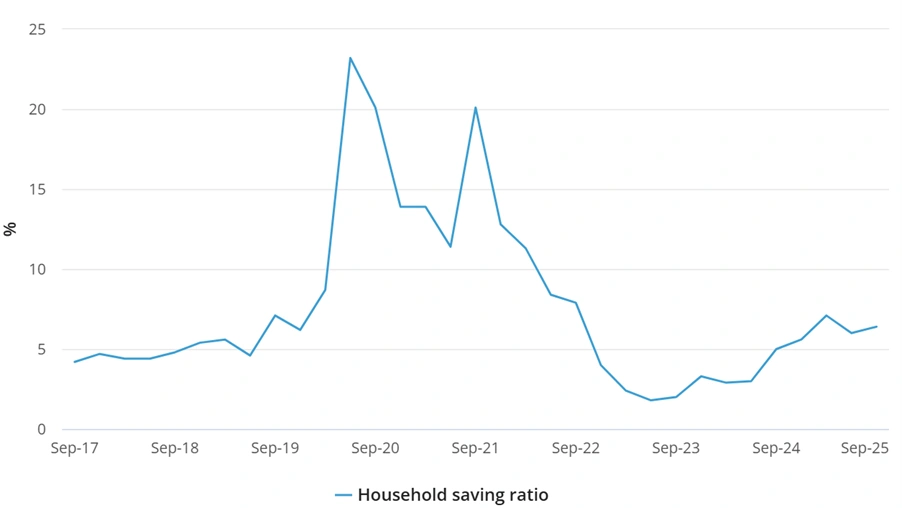

Perhaps the most encouraging sign came from household balance sheets. The savings ratio climbed to 6.4% from an upwardly revised 6%, indicating consumers still possess substantial spending power despite cost-of-living pressures.

This elevated savings rate suggests Australian households have built a financial buffer, potentially supporting consumption in coming months. The rise occurred even as discretionary spending picked up, pointing to improved household confidence.

Real household disposable income has benefited from declining inflation and earlier interest rate cuts by the Reserve Bank. The RBA reduced the cash rate to 3.6% earlier in 2025, providing relief to mortgage holders and stimulating consumer activity.

Reserve Bank Implications

The below-forecast growth figure complicates the RBA’s monetary policy calculus. Governor Michele Bullock and the Monetary Policy Board must balance supporting economic growth against persistent inflation pressures.

Recent inflation data showed headline CPI rising to 3.2% in the September quarter, above the RBA’s 2-3% target range. Trimmed mean inflation, the central bank’s preferred measure, increased to 3.0% from 2.7% in June.

Measures of Consumer Price Inflation

This inflation surprise led the RBA to hold the cash rate steady at its November 2025 meeting. Market expectations for further rate cuts in 2026 have been scaled back significantly.

The September quarter GDP outcome may provide some ammunition for doves on the RBA board arguing for continued monetary easing. However, the stubborn inflation print likely prevents any imminent action.

ANZ recently scrapped its forecast for additional rate cuts in 2026, citing persistent price pressures and the economy’s resilience. Other major banks have similarly pushed back expectations for the next easing move.

Per Capita GDP Remains Weak

Beneath the headline numbers lies a less encouraging story. GDP per capita, a key measure of living standards, continues struggling despite the aggregate economic expansion.

While official September quarter per capita data wasn’t immediately available, the trend through mid-2025 showed Australia experiencing one of the longest stretches of negative per capita growth on record. This reflects high population growth from migration outpacing economic expansion.

The phenomenon has sparked political debate about Australia’s migration settings and their impact on household prosperity. Cost-of-living pressures remain acute for many families despite improving aggregate economic conditions.

Market Reaction Muted

Australian stock markets responded with modest moves to the GDP release. The ASX 200 traded slightly higher on the day, with energy and materials sectors leading gains while technology stocks faced pressure.

The weaker-than-expected quarterly figure supported arguments for continued monetary accommodation, lifting rate-sensitive sectors. However, elevated inflation readings prevent excessive optimism about rapid rate cuts.

The Australian dollar remained relatively stable against major currencies. Foreign exchange traders appeared to focus more on inflation dynamics and RBA policy implications than the GDP miss itself.

Bond markets saw yields tick marginally lower as investors priced in a slightly slower economic trajectory than previously anticipated.

Economic Headwinds Persist

Several structural challenges continue weighing on Australia’s economic performance. Business investment, while elevated, has shown signs of plateauing after strong gains in previous quarters.

Public investment actually fell in recent quarters before recovering slightly, reflecting lumpy government infrastructure spending patterns. The outlook for public capital expenditure remains uncertain given fiscal constraints.

Global economic conditions present ongoing risks. China, Australia’s largest trading partner, faces persistent property sector weakness and soft domestic demand. Recent stimulus measures from Beijing have provided some support, but structural economic challenges remain.

US trade policy under the Trump administration adds another layer of uncertainty. Tariff threats and protectionist rhetoric could disrupt global trade patterns, potentially impacting Australian commodity exports.

What Economists Say

Capital Economics’ Abhijit Surya noted the economy appears to be transitioning toward more sustainable growth rates. “The recovery in private demand continues, though at a slower pace than markets expected,” he said.

Oxford Economics pointed to emerging green shoots despite the quarterly disappointment. Leading indicators suggest economic momentum may build in coming quarters as rate cuts work through the system.

However, productivity growth remains a critical concern. Labour productivity has stagnated, limiting potential economic gains and wage growth. Boosting productivity requires increased business investment and structural reforms.

Treasury officials have emphasised the need for policies supporting productive capacity expansion. Without improved productivity, sustaining higher living standards becomes increasingly difficult.

Outlook for 2026

The economic trajectory into 2026 depends heavily on several key factors. Consumer spending must maintain momentum as government stimulus effects fade and rate cut impacts gradually build.

Business confidence and investment intentions will prove crucial. Capital expenditure drives productive capacity and employment, underpinning sustainable growth.

Labour market conditions remain relatively tight despite recent unemployment increases. The jobless rate rose to 4.5% in September from earlier lows, but remains well below historical averages. Strong employment supports household incomes and consumption.

Housing market strength continues, with prices rising across most capital cities. Wealth effects from property appreciation typically boost consumer spending, though affordability concerns persist.

Global economic conditions, particularly China’s trajectory, will significantly influence Australia’s outlook. Any meaningful Chinese stimulus could lift commodity demand and prices, benefiting Australian exporters.

Internal Structural Challenges

Beyond cyclical factors, Australia faces several structural economic challenges requiring attention. Population growth has outpaced infrastructure investment, creating capacity constraints in major cities.

Housing supply remains critically short of demand, driving price increases that lock younger Australians out of homeownership. Construction bottlenecks and planning restrictions constrain new dwelling completions.

The economy’s productivity performance has deteriorated since the global financial crisis. Annual productivity growth has averaged below 1% in recent years, down from above 2% historically.

Addressing these structural issues requires policy reforms beyond monetary policy’s scope. Infrastructure investment, planning system reforms, and productivity-enhancing measures all deserve priority attention.

Fiscal Policy Considerations

Government spending played an outsized role in supporting recent GDP growth. Public consumption and investment together contributed significantly to quarterly expansion.

However, fiscal constraints may limit future public sector contributions. Budget deficits require eventual correction, particularly as Commonwealth debt levels rise. Treasury recently downgraded budget forecasts by over $100 billion due to weaker mining sector returns.

The challenge for fiscal policymakers involves supporting growth and essential services while maintaining sustainable debt trajectories. Difficult spending prioritisation decisions loom as revenue growth slows.

Natural disaster costs have added further fiscal pressure. Floods and cyclones cost the economy $2.2 billion in the first half of 2025, requiring government disaster response spending.

Regional Economic Divergence

Economic conditions vary significantly across Australian states and territories. Resource-rich states like Western Australia and Queensland continue benefiting from mining sector strength.

Eastern seaboard states face more challenging conditions. New South Wales and Victoria, home to Sydney and Melbourne respectively, experienced weaker economic performance. Service sector weakness and construction industry challenges weighed on these economies.

Regional areas dependent on agriculture faced mixed fortunes. Favourable weather supported crop production in some regions, while others dealt with climate challenges impacting yields.

Tourism recovery continued unevenly. International visitor numbers rebounded but remained below pre-pandemic levels. The weaker Australian dollar against major currencies should eventually support inbound tourism.

Looking Ahead

Australia’s economic performance in the September quarter delivered a reminder that recovery paths rarely follow straight lines. The miss against quarterly expectations tempers recent optimism without derailing the broader recovery narrative.

Key developments to watch include:

- December quarter GDP data, expected in March 2026

- RBA monetary policy decisions through early 2026

- Labour market trends, particularly unemployment and wage growth

- Inflation trajectories and their policy implications

- Global economic conditions, especially China’s performance

- Federal budget updates and fiscal policy directions

The Australian economy grew 2.1% year-on-year in September, marking the fastest annual expansion since mid-2023. While quarterly growth of 0.4% disappointed forecasts, household consumption showed resilience and savings ratios climbed.

Policymakers face difficult trade-offs between supporting growth and containing inflation. The path ahead requires navigating these competing pressures while addressing structural productivity challenges.

For Australian households and businesses, the mixed economic signals suggest continued volatility and uncertainty through 2026. Prudent financial management and flexibility will remain essential as economic conditions evolve.

The September quarter GDP report underscores that Australia’s economic recovery, while ongoing, faces headwinds requiring careful policy responses and structural reforms to secure sustainable prosperity.

Also Read: Government Finally Releases Damning Report on Appointments Process After Two-Year Delay

Frequently Asked Questions

Q: What was Australia’s GDP growth in the September 2025 quarter?

A: Australia’s gross domestic product grew 0.4% in the September quarter 2025, below market forecasts of 0.7%. However, annual growth reached 2.1%, the fastest pace since mid-2023.

Q: Why did Australia’s GDP miss forecasts?

A: The main drag came from inventory changes, which subtracted 0.5 percentage points from growth. Businesses reduced stockpiles amid uncertain demand conditions, offsetting gains from household consumption and business investment.

Q: What does this mean for RBA interest rates?

A: The below-forecast GDP growth provides some support for future rate cuts. However, persistent inflation above the RBA’s target range likely prevents imminent action. Market expectations for 2026 rate cuts have been scaled back.

Q: Is Australia in a per capita recession?

A: While aggregate GDP grew, per capita GDP has struggled due to high population growth from migration outpacing economic expansion. This has created pressure on living standards despite positive headline growth numbers.

Q: When will the next Australian GDP data be released?

A: The December quarter 2025 GDP data is scheduled for release in early March 2026. This will provide crucial insights into economic momentum heading into the new year.