Australia mines half the world’s lithium. Yet it refines barely 1%.

That glaring gap has fuelled China’s stranglehold on battery supply chains for years. Beijing controls 70% of global lithium refining despite producing just 17% of raw ore. The result? Australia exports truckloads of spodumene to Chinese facilities, capturing only a fraction of the value.

Now the country wants to change that narrative. New refineries are coming online, government cheques are flowing, and miners are betting billions on downstream processing.

But the path ahead looks brutal. Chinese plants cost a tenth of what Australia spends to build. Labor shortages plague the sector. Technical expertise remains thin.

Can Australia truly rival the refining giant? Or is this another expensive lesson in supply chain realities?

China’s Grip Tightens as Australia Stumbles

The numbers tell a sobering story. China will overtake Australia as the world’s top lithium miner by 2026, according to Fastmarkets forecasts. That’s despite Australian operations being more profitable on paper.

Chinese producers refuse to cut output when prices crash. They operate at a loss for months, backed by government subsidies and municipal pressure to keep jobs. When lithium prices collapsed 80% from 2022 peaks—plunging from $123,000 to $10,000 per tonne—Australian miners slashed production and shelved expansions.

Chinese operations barely blinked.

CATL, the battery giant, briefly paused mining in September 2024 when prices hit rock bottom. By February 2025, they were back at full throttle. Australian nickel mines? All shut by Chinese price manipulation, including BHP’s Nickel West operations until at least 2027.

Contemporary Amperex Technology Co., Limited

This aggressive market strategy works because China plays the long game. They’re not chasing quarterly profits—they’re cementing supply chain dominance for the next 50 years.

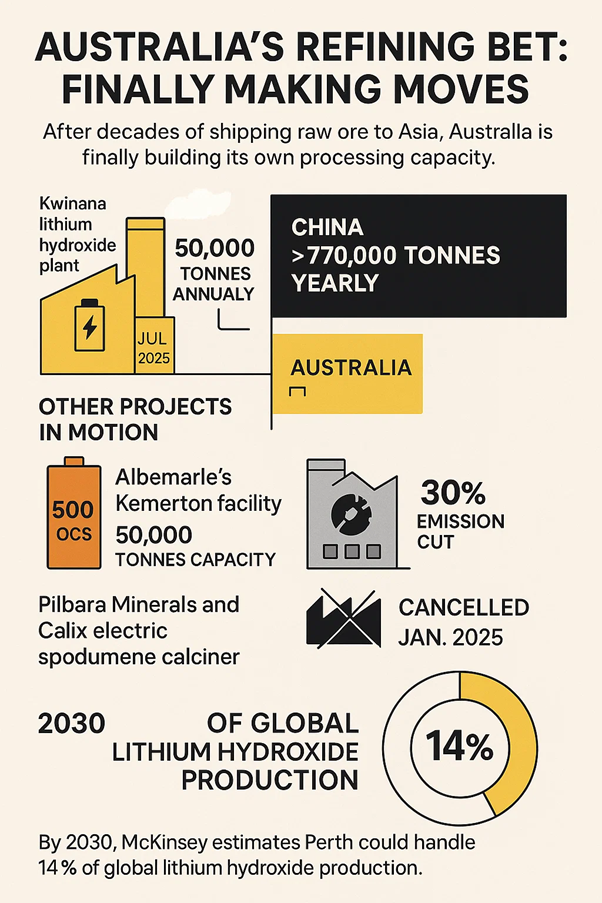

Australia’s Refining Bet: Finally Making Moves

After decades of shipping raw ore to Asia, Australia is finally building its own processing capacity.

The Kwinana lithium hydroxide plant in Western Australia started producing battery-grade material in July 2025. The facility, a joint venture between Chilean giant SQM and Wesfarmers, targets 50,000 tonnes annually.

That’s a start. But context matters: China processes over 770,000 tonnes yearly.

Other projects are in motion:

- Albemarle’s Kemerton facility reached 50,000 tonnes capacity

- Pilbara Minerals and Calix are building an electric spodumene calciner—a world-first technology slashing emissions by 30%

- Tianqi and IGO’s expansion at Kwinana was cancelled in January 2025, victim to low lithium prices

The pilot projects show promise. The Pilbara-Calix demonstration plant resumed construction in February 2025 after snagging $23 million in government support. If successful, it could revolutionise how Australia processes hard-rock lithium while dramatically cutting carbon emissions.

By 2030, McKinsey estimates Perth could handle 14% of global lithium hydroxide production. That would create a critical mass of expertise—potentially turning Western Australia into a knowledge hub for battery materials.

Why Building in Australia Costs a Fortune

Here’s the brutal economics: Australian refineries cost $50,000 per tonne of annual capacity. Chinese facilities? Around $20,000.

That 2.5x premium stems from several pain points:

- Construction timelines drag. China builds lithium refineries in under two years. Australian projects routinely blow past four years, with delays piling up costs. Regulatory approvals, Indigenous heritage surveys, and strict environmental standards all add months.

- Labor shortages bite hard. Western Australia’s mining sector already faces severe worker shortages. Adding 4,000 refinery jobs by 2030 seems optimistic when current operations can’t fill positions. The state needs mechanical engineers, process chemists, and commissioning specialists—roles requiring years of specialised training.

- Energy costs remain steep. Despite abundant renewable resources, Australian power still costs more than China’s coal-fired grid. Natural gas reduces emissions by 50% compared to coal roasting, but it’s not free.

McKinsey research suggests fully integrated operations (combining mining and refining) could produce lithium hydroxide at $10,000 per tonne—still competitive globally. But achieving that integration requires massive upfront capital most companies can’t muster during price downturns.

Government Steps Up With Strategic Funding

Canberra recognises the stakes. The National Reconstruction Fund injected $83 million into Liontown Resources’ Kathleen Valley operation in August 2025. That investment came during a savage lithium downturn, demonstrating strategic conviction.

Total government commitments include:

- $4 billion Critical Minerals Facility

- $3 billion earmarked for renewables and low-emission tech under the NRF

- 10% production tax incentive for processing and refining of 31 critical minerals

- Fast-tracked approvals through the Major Projects Facilitation Agency

Resources Minister Madeleine King framed Australia’s lithium mining as essential to the global energy transition. “To meet our net zero targets we will need more mining,” she stated at the Kathleen Valley opening.

That’s accurate. But mining is only half the equation. Processing determines who captures the real value.

State governments are also backing innovation. Western Australia provided $23 million to restart the Pilbara-Calix calciner project. The technology could slash processing emissions while making operations more cost-effective.

The Technical Expertise Gap Nobody Wants to Discuss

China didn’t build refining dominance overnight. They spent 30 years developing process engineering know-how, training thousands of chemical engineers, and perfecting hydroxide production from multiple feedstocks.

Australia is starting from scratch.

“We feel that we have adequate experience and capability together with our team in SQM to commission and run [the facility] successfully,” said Wesfarmers Managing Director Rob Scott. That confidence relies heavily on Chilean expertise—essentially importing knowledge rather than building it domestically.

The Greenbushes mine, despite being the world’s largest hard-rock lithium deposit, is 51% owned by Chinese Tianqi Lithium. IGO’s joint venture gives Australia control, but the technical partnerships reveal dependency.

The open pit of the Greenbushes mine, Western Australia

Training programs can’t close the gap quickly. Process chemistry for hydroxide extraction requires specialised understanding of roasting temperatures, leaching chemistry, and crystal formation. Chinese facilities have decades of institutional knowledge embedded in their operations.

Australian universities are ramping up materials science and mining engineering courses. But training cycles stretch years, not months. By the time graduates enter the workforce, will the market have already moved on?

What Victory Actually Looks Like

Rivalling China’s refining scale seems unrealistic. But Australia doesn’t need to match Beijing’s 770,000-tonne capacity to win strategically.

Success means capturing 20-25% of global lithium hydroxide production by 2035. That percentage would establish Australia as the Western world’s primary alternative supplier—critical for electric vehicle manufacturers and battery producers seeking supply chain diversification.

Geopolitical tensions make Australian lithium worth a premium. Automakers in the US, Europe, and Japan increasingly prioritise “friend-shored” supply chains from stable democracies. Tesla’s 110,000-tonne spodumene deal with Core Lithium’s Finniss project demonstrates this willingness to pay extra for security.

If Australian operations can produce hydroxide at $16,000-18,000 per tonne (competitive with Chinese imports after tariffs and transport), they’ll find ready customers. Lower-emission processing using renewable energy adds further value in markets with carbon border adjustments.

The ASX-listed critical minerals sector has already seen investment surge. IGO, Pilbara Minerals, Mineral Resources, and Liontown command multi-billion dollar valuations based on production growth potential.

The Verdict: David vs Goliath, With Government Backing

Australia won’t dethrone China as the lithium refining king. That ship sailed decades ago.

But the country can build a profitable niche as the secure, lower-emission alternative for Western manufacturers. Integrated operations combining Australia’s vast lithium reserves with renewable-powered refining offer genuine competitive advantages—if companies can survive the brutal capital costs and labor shortages.

The next five years will determine whether this downstream push succeeds or becomes another expensive lesson in industrial policy. Early movers like Wesfarmers, Pilbara Minerals, and Liontown are betting billions that geography, geology, and geopolitics can overcome China’s cost advantages.

Time will tell if they’re visionaries or just late to a party that’s already over.

Also Read: Why BHP Just Made Its Boldest Copper Move in Years

FAQs: Australia’s Lithium Processing Push

1.How much lithium does Australia currently refine?

Less than 1% of the country’s lithium production undergoes domestic refining. The Kwinana plant represents Australia’s first significant battery-grade hydroxide facility, with capacity reaching 50,000 tonnes in 2025.

2.Why are Australian refineries so expensive to build?

Construction costs run 2.5x higher than China due to longer timelines (4-6 years vs 2 years), labor shortages, strict environmental regulations, and higher energy expenses. Capital costs can exceed $50,000 per tonne of annual capacity.

3.Will Australia overtake China in lithium refining?

Unlikely in absolute terms. China will maintain majority market share through 2035. However, Australia aims to capture 20-25% of global hydroxide production, becoming the primary Western alternative supplier.

4.What’s driving government investment in lithium processing?

Supply chain security and value-adding domestic industry. Processing lithium hydroxide generates 5-10x more economic value than exporting raw spodumene. It also creates high-skilled jobs and reduces dependence on foreign refineries.

5.Are Australian lithium prices recovering?

Industry forecasts project lithium prices reaching $32,000 per tonne by late 2026, then stabilising around $24,000 per tonne midcycle. This recovery relies on EV adoption acceleration and normalisation of excess inventory stockpiles.