The world finds itself at a pivotal moment right now. Countries are rushing to lock in supplies of lithium, copper, and rare earth elements, all while trying to keep up with their promises on climate change. These critical minerals aren’t just ordinary stones buried in the earth – they form the foundation for a more sustainable world ahead.

Explosive Demand Growth Reshapes Global Markets

The figures tell a compelling story. In 2024, the global market for critical minerals hit $516 billion, and experts predict it will climb to $963 billion by 2032. According to the International Energy Agency, we’ll need three times as many minerals by 2030 and four times by 2040 if we’re serious about reaching net-zero emissions.

Lithium is at the forefront of this boom. Its demand shot up by almost 30% in 2024, and forecasts suggest a massive 1,500% rise by 2050. Copper, often called “the new oil,” is under similar strain, as electric vehicles and renewable energy setups devour huge amounts of it.

Lithium leads global critical mineral demand

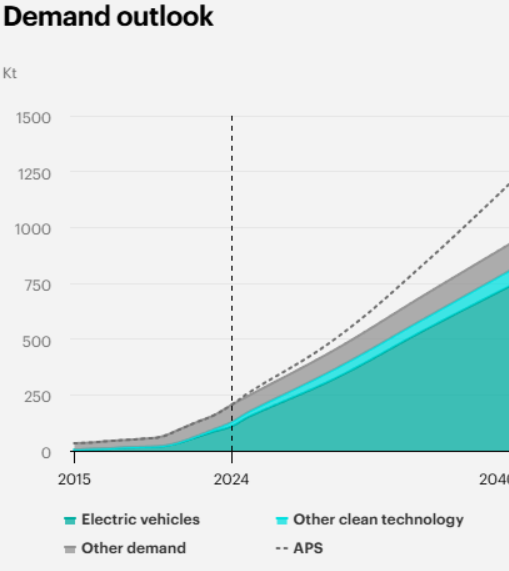

Electric vehicles are a big driver here. A standard EV uses six times more minerals than a traditional car, and wind farms require nine times more than gas-fired power plants. Since 2020, battery storage has accounted for 85% of the growth in demand for these key minerals.

The surge in renewable energy only adds to the pressure. Solar panel installations jumped 85% in 2023, wind turbine additions increased by 60%, and the world’s battery storage capacity doubled. Each of these technologies calls for particular mixes of minerals that our current supply networks are finding hard to deliver.

Sustainable Mining Practices for Critical Minerals Under Intense Scrutiny

Mining firms are feeling the heat to juggle the need for more extraction with care for the environment. Old-school open-pit methods guzzle enormous amounts of water, release greenhouse gases, and upset local wildlife. It’s a real irony: we’re digging up more to protect the planet from climate change.

Water consumption stands out as the toughest issue. In Chile’s Atacama Desert, extracting lithium uses up 500,000 litres of water for every tonne produced. This often leaves nearby communities short on groundwater as companies pump out brine for processing.

But forward-thinking businesses are turning to fresh ideas:

- Biomining swaps out harsh chemicals for microbes, cutting down on environmental hazards and pulling out a wider range of minerals.

- Progressive reclamation means fixing up damaged land while mining is still underway, not leaving it until the end.

- Bringing in renewable energy to run processing plants can slash emissions by as much as 80%.

Take Rio Tinto as an example of this change. The company aims to lift its copper production by 18% by 2025, all while rolling out tougher standards on environmental, social, and governance matters across its sites.

In Australia, the mining industry is pioneering these sustainable approaches. Companies listed on the ASX, such as Pilbara Minerals and Lynas Rare Earths, are pouring money into cleaner ways to extract minerals and building strong ties with Indigenous communities.

Recycling provides another promising route. The IEA reckons that solid recycling efforts could cut the need for new mining by 25-40% by the middle of the century. Yet, right now, recycling rates are disappointingly low – under 1% for lithium and rare earths.

Economic Implications of Critical Mineral Scarcity Send Shockwaves Through Industries

When supplies get disrupted, the economic fallout can be huge. The US Geological Survey’s 2025 report points to potential hits to GDP ranging from millions to billions of dollars, depending on the mineral. A prolonged shortage in battery metals might push global battery prices up by 40-50%.

Supply disruptions can have massive economic costs

The fact that production is concentrated in a few places makes things riskier. China handles the lion’s share of processing for several minerals:

- 80% of battery-grade graphite

- 70% of cobalt refining

- 60% of lithium processing

- 90% of rare earth elements

The Democratic Republic of Congo provides 70% of the world’s cobalt, and Indonesia leads in nickel. If something goes wrong in one of these countries, it could bring whole supply chains to a halt.

We’ve seen this in recent price swings. Lithium costs skyrocketed eight times over in 2021-22, then plummeted 80% in 2023. These ups and downs make it tough for manufacturers and investors to plan ahead.

Looking forward, mismatches between supply and demand are a real concern. Copper could face a 30% shortfall by 2035, even with steady demand growth. New mines take 10-15 years to get going, so the choices we make today will shape what’s available tomorrow.

The ripple effects go beyond single materials. Carmakers are already dealing with chip shortages that mess up their schedules. If critical minerals follow suit, it could slow down the shift to electric vehicles and green energy projects – just when we need to speed up for the climate.

Global Powers Rush to Secure Strategic Supply Chains

Around the world, governments see critical minerals as vital to national security. The US has expanded its list of critical minerals to 54 items, highlighting how relying on imports leaves economies exposed.

Policies are ramping up quickly. In the US, executive orders have sped up mining approvals on federal land and looked into offshore options. The Department of Energy has pledged close to $1.8 billion to strengthen homegrown supply chains.

Major economies are stepping up their strategies:

- The European Union, through its Critical Raw Materials Act, wants 10% of production to happen domestically by 2030.

- Australia’s Critical Minerals Strategy 2025 sets the country up as a reliable supplier.

- Canada’s approach stresses partnerships with Indigenous groups and high ESG standards.

- Japan is teaming up with Australia and African countries to lessen its reliance on China.

Trade barriers are popping up as nations guard their own stocks. China has put controls on exporting gallium, germanium, and tungsten. Others are thinking about doing the same for their key minerals.

On the brighter side, international groups are forming. The Minerals Security Partnership unites like-minded countries to build alternative supply routes. Deals between producers and buyers help create lasting stability.

Australia’s outlook for critical minerals in 2025 shows how resource-rich places can make the most of their strengths. With government support, clear rules, and a focus on ESG, it draws in overseas investment and eases global supply worries.

Investment Capital Flows Transform Mining Finance

The way mining gets funded is changing to match the demand for critical minerals. Tools like green bonds, loans tied to sustainability goals, and government-backed credits are becoming commonplace. They lower costs when companies hit their ESG targets.

Even in tough price times, exploration spending rose 15% in 2023. Canada and Australia saw the biggest jumps, with lithium projects getting an 80% boost in funding despite soft prices.

Some standout deals show the new trends:

- Summit Nanotech raised $81 million in Series A for eco-friendly lithium extraction.

- Kobold Metals secured $318 million to hunt for cobalt using AI.

- Energy Exploration Technologies got $81 million from GM Ventures for direct lithium methods.

On the ASX, critical minerals firms are drawing big interest from institutions. Pilbara Minerals reached a $24 billion market cap, and Lynas Rare Earths topped $10 billion.

Partnerships with end users are reshaping the sector. Tesla locks in long-term deals with miners, guaranteeing lithium while helping fund projects. Toyota and Korean battery makers are doing similar things to ensure steady income.

As ESG becomes central, companies that excel in it command higher values. Investment funds now prioritise low-emission operations, involvement with Indigenous peoples, and open management practices.

Technology Innovation Drives Efficiency Gains

Cutting-edge tech is revolutionising how we extract and process minerals. AI streamlines finding new deposits, cutting costs and time. Satellites and machine learning spot likely sites quicker than old techniques.

In processing, innovations like direct lithium extraction save water and boost yields. They pull lithium from brines without the huge evaporation ponds that take ages to work.

Automation makes underground work safer and more efficient. Machines controlled from afar handle risky jobs and trim labour expenses. Systems that predict breakdowns keep things running smoothly.

Digital tracking follows minerals from the mine to the final product, satisfying ESG rules and keeping supply chains clear. Blockchain offers tamper-proof records of where minerals come from and how they’re handled.

The idea of a circular economy is catching on with better recycling tech. “Urban mining” salvages metals from old electronics, easing the load on fresh digging. Facilities for recycling EV batteries recover lithium, cobalt, and nickel from worn-out packs.

Regional Dynamics Shape Market Development

Each part of the world tackles this based on what resources they have and their industrial setup. Australia uses its mineral riches and steady government to become a go-to supplier for Western buyers.

Africa has its hurdles. It boasts big reserves of cobalt and lithium, but often misses out on processing plants. Overseas money helps, but it sparks worries about exploitation and whether locals truly benefit.

In Latin America, the “Lithium Triangle” across Chile, Argentina, and Bolivia holds most of the world’s reserves. But shaky politics and water shortages make progress tricky. Chile turned down a lithium project lately over green concerns.

The Lithium Triangle – a region within the Arid Diagonal of South America

North America focuses on bringing production closer to home or to friendly nations. Mexico’s move to nationalise lithium and Canada’s rules on Indigenous partnerships show varied ways to claim control over resources.

The Asia-Pacific area leads in consumption while ramping up processing. South Korea, Japan, and Australia are linking up to cut back on Chinese dominance in battery chains.

Future Outlook: Navigating Uncertainty

Over the next ten years, the critical minerals scene will change a lot. Demand seems set to keep growing as clean energy spreads worldwide. But supply might lag because of long waits for new mines and tricky approvals.

Prices will probably stay unpredictable. Markets are tight, with little extra stock to cushion blows. Bad weather, political rows, or policy shifts can send prices soaring or crashing.

Tech advances might alter what we need. Solid-state batteries could use less lithium but more of other stuff. If fusion energy takes off, it might end our reliance on fossil fuels but demand new minerals.

Competition between countries is heating up. They view these minerals like oil or gas – key assets. Expect more trade limits and export rules as nations shield their industries.

The energy transition’s success hinges on sorting out these mineral issues. Without enough at fair prices, rolling out clean tech could grind to a halt just as the climate needs a peak.

Those companies and countries that create tough, green supply chains will reap the biggest rewards from the shift. Others who drag their feet might miss out on this new wave of industry driven by critical minerals.

Also Read: Victory Metals Identifies Ultra-High Heavy Rare Earth Zones at North Stanmore

Key Takeaways for Stakeholders

Tackling the critical minerals puzzle calls for teamwork among governments, businesses, and communities. No one can fix supply weak spots on their own.

For investors, look at firms that show:

- Solid ESG track records and community involvement

- Varied mineral holdings to spread risk

- Secure long-term deals with reliable buyers

- Tech that boosts how efficiently they extract

Policymakers have to juggle:

- Boosting local output without harming trade ties

- Drawing in funds while upholding eco rules

- Stockpiling strategically without messing up markets

- Sparking new ideas while keeping things fair

At its core, the critical minerals tale is about making things possible. They power the clean energy switch that drives climate efforts and supports human progress. Nailing this mineral side is crucial for all that comes next.

The competition is underway. Nations, firms, and groups that act swiftly and wisely in building sustainable critical mineral networks will shape the future of global economics. The risks are enormous – the planet’s tomorrow relies on pulling these resources out responsibly and smartly.