Critical minerals companies in Australia are poised to make a difference in decarbonisation across the world. These listed companies are suppliers to the global economy of minerals that are material inputs to renewable energy and electrification. The mining industry is no longer limited to the traditional commodities as it now concentrates on lithium, rare earth elements, nickel and cobalt.

Global Market Dynamics Drive Critical Mineral Demand

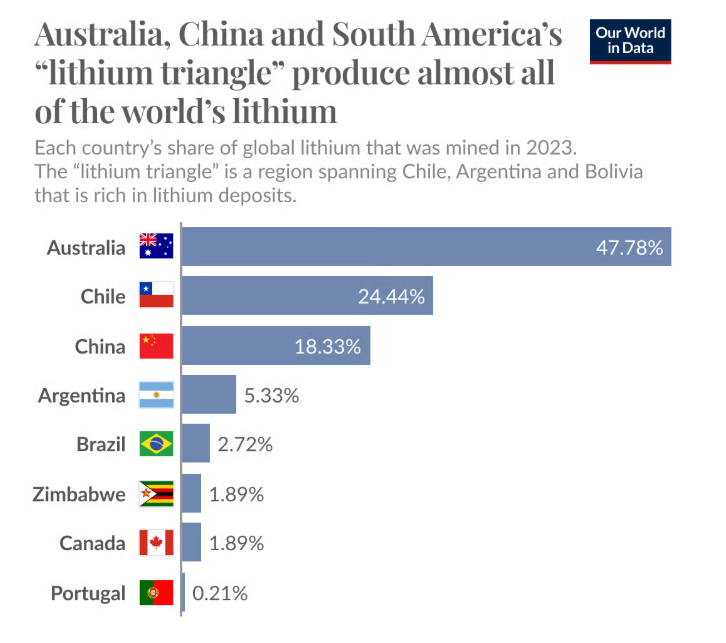

The surge in electric vehicles, grid-scale energy storage, and wind power has magnified the demand for critical minerals. Australia’s mines now deliver over 45% of global lithium, positioning the nation as the largest lithium supplier. The transition to renewable energy magnifies the urgency for a secure supply of these resources.

- Over 70% of Australia’s lithium output in 2025 will reach Asian EV manufacturers.

- Australia’s lithium sector expects an 18% increase in production this year to meet international demand.

- Critical minerals now feature in supply security agreements and trade alliances worldwide.

Global Lithium production in 2023

Industry Overview: Top ASX Critical Minerals Companies

The Australian Securities Exchange (ASX) is home to a broad spectrum of producers, including large mine operators as well as other specialist ones. Australian miners have solidified their reputation at international levels due to an orientation on operational excellence, sound ESG standards and continued innovation.

Major Players and Their Roles

- BHP Group (ASX: BHP) is a resource powerhouse that is diverse. It has iron ore, copper, nickel, and coal in its portfolio. The wide commodity by BHP and financial strength in the past are the drivers of sustained revenue growth. The firm estimates an 8-10 % growth in revenue and a 5.5 % dividend payment in 2025. Its ESG credentials and its orientation toward green mining activities help strengthen its competitor market position.

- Fortescue Metals Group (ASX: FMG) is a company working with iron ore and green hydrogen and is expected to increase its sales by 10 -13 per cent. Its clean energy-integrated plan is on track with the global energy transition. A 7 per cent dividend yield appeals to investors who want income.

- Pilbara Minerals (ASX: PLS) is a prime example of lithium-focused stocks that supply key battery-grade minerals to EVs and storage. Pilgangoora project in WA stakes its claim in the market through increased production and technological processing. Pilbara forecasts a 25-30 per cent growth in revenues by 2025, with more than 640,000 tonnes LCE that should be produced. Investment risk is increased via exposure to fluctuations in commodity prices.

- South32 (ASX: S32) offers diversified operations in alumina, manganese, nickel, and more. Expansion of battery-grade nickel and manganese justify high ESG ratings and balanced growth prospects. The firm projects a 12–15% revenue increase as demand for battery materials accelerates.

- Lynas Rare Earths (ASX: LYC) remains the only significant rare earths producer outside China. Its products underpin defence, wind turbines, and high-tech manufacturing. Projected revenue growth for 2025 stands at 17–20%. Lynas’ uniqueness in the rare earth supply chain gives it strategic importance.

- IGO Limited (ASX: IGO) holds substantial stakes in lithium and nickel, including the world’s highest-grade lithium mine at Greenbushes. ESG initiatives and downstream processing investments align with global battery manufacturers’ needs. IGO forecasts 15–18% revenue growth with a 2.5% dividend for the coming year.

Leading ASX Lithium Companies: Meeting Battery Demand

Australia’s lithium narrative in 2025 focuses on scale, innovation, and strategic market positioning. Five companies dominate the ASX lithium field:

| Company | ASX Ticker | Est. 2025 Lithium Production (LCE tonnes) | Market Share (%) | Major Project | Trend/Development | Main Challenges |

| Pilbara Minerals | PLS | 640,000 | 19.5 | Pilgangoora (WA) | Ramp-up, tech innovation, battery-grade conversion | Logistics, costs, resource depletion |

| Mineral Resources | MIN | 520,000 | 15.8 | Wodgina, Mt Marion (WA) | Downstream processing, JV expansion | Environmental approvals, cost inflation |

| Allkem Limited | AKE | 310,000 | 9.2 | Mt Cattlin (WA), Olaroz, Sal de Vida | M&A integration, global supply, brine/rock tech | Regulation, FX, tech implementation |

| Liontown Resources | LTR | 330,000 | 10.2 | Kathleen Valley (WA) | Shift to production, offtake to EV makers | Project execution, competition |

| IGO Limited (JV) | IGO | 420,000 | 12.8 | Greenbushes (WA) | Downstream, ESG, supply to battery players | Regulatory scrutiny, competition |

Over 70% of this output is committed to Asian markets, reinforcing Australia’s supply chain dominance.

Innovation and Technology in Lithium Production

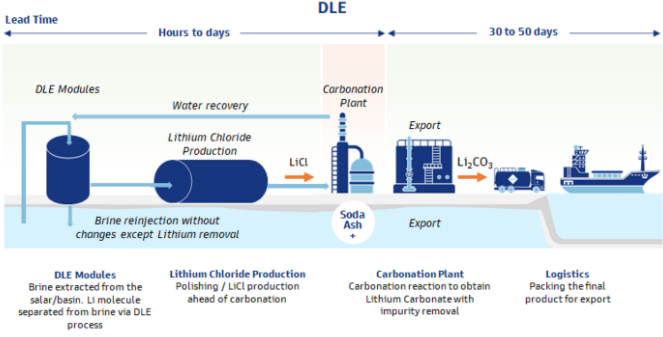

Lithium production is changing rapidly via innovation and technology to make the process more economical to extract and produce batteries. Improvements are being made into new processes such as Direct Lithium Extraction (DLE) that directly extracts lithium by use of selective absorbents and membranes that reduce water consumption, and lead to lower negative environmental impact than used in traditional methods.

Meanwhile, battery technologies are being improved with solid-state batteries featuring solid electrolytes, silicon anodes, and dry manufacturing processes that increase battery safety, energy density, charging capacity, and life span. This is because the innovations allow lithium to be recovered in less time, where emissions are reduced, and the emerging trend of electric vehicles and renewable energy storage growth is impacting the environment to be healthier and more robust in its supply chain of technologies utilising lithium.

Direct Lithium Extraction Technology

Rare Earth Mining: Securing the Future of High-Tech

Rare earth metals underpin the manufacture of wind turbines, electric motors, electronics, and defence systems. Their supply remains a strategic concern:

- Lynas Rare Earths operates the largest rare earths mine outside China, with advanced processing and export channels.

- Advanced exploration companies such as Trek Metals (ASX: TKM) and DY6 Metals (ASX: DY6) focus on lithium and rare earth projects in Australia and abroad.

- New entrants bolster Australia’s credentials as a stable, alternative supplier for future minerals.

The Mt Weld mine, in Western Australia

ESG Standards Attract New Investment

Australian mining firms embed Environmental, Social, and Governance (ESG) principles at every level. They take steps to reduce emissions, manage water sustainably, and foster community engagement. High ESG ratings drive more investment in Australian mineral companies. ASX miners with advanced ESG practices have outperformed less compliant competitors by 15% over the last 12 months. Federal and state governments give policy support for faster approvals and private sector innovation.

The Northern Goldfields Solar and Battery Storage Facility

Sector Challenges and Solutions

The challenges affecting this sector are peculiar to it. Companies need to overcome volatility in the price of commodities and deal with increased costs of labour and energy. Environmental laws demand active project design and local interaction. Major companies invest in Indigenous relations, water conservation and environmental rehabilitation as a way of ensuring long term licensed access to operate.

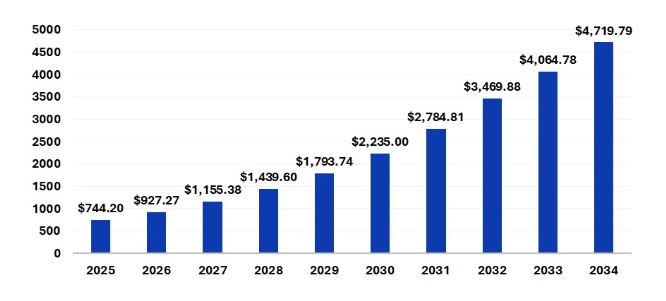

A Decade-Long EV Demand Outlook

The global EV market is expected to grow strongly over the next 10 years, between 2025 and 2035, with a compound annual growth rate of about 8.3%. It is estimated that the value of the market will increase more than two-fold, increasing to approximately USD 99 billion in 2025 and USD 222 billion in 2035. The number of EV sales has reached 20 million by 2025 and will pass over 50 percent of car sales worldwide by 2035. Electric cars have the potential to account for about 70 percent of world passenger car sales by the year 2040.

Currently, China rules the world market with EV sales, posting an estimated 65% of the total number of EV sales, followed by Europe with 17%, and the United States with about 7%. Cumulatively, these three markets make up approximately 95 percent of EV sales in the world today. In the meantime, areas previously underserved like Southeast Asia, Latin America and some parts of Africa are also experiencing the rapid increase in EV popularity, as local policies and the introduction of more cars push the market in these directions.

Though the US market has experienced lower-than-anticipated growth as a result of policy changes such as weakened federal vehicle mileage requirements and EV tax credit phaseouts, it is still projected to modestly grow the EV sales by 1.6 million units in 2025 to 4.25 million by 2030. This entails the fact that the electric vehicle adoption in spite of the existing national regulatory headwinds, remains a significant long-term trend not just in the US but also all around the world.

Electric mobility market size from 2025 to 2034

Australia’s Strategic Role in Global Supply Chains

The rich supply of critical minerals in Australia positions the country at the centre of world supply chains in the diversification and strengthening of such supply chains to EV battery metals. The increasing US and European interest in creating secure national and allies’ supply chains increases the pressure to source open, conflict-free and ESG-friendly mineral supply. The political stability of Australia and existing mining infrastructure make it an ideal mining-supply option to the markets.

As part of such associations and trade deals, Australia is also becoming an important participant in these supply chains through exports of battery metals like lithium, nickel, cobalt and rare earth elements. The ASX-listed companies enjoy access to international battery manufacturers, vehicle producers, and energy storage companies, which underpin long-term offtake agreements that are critical in continuing to invest and develop on critical mineral projects.

Government and Policy Support for Critical Minerals

The Australian Government released the Critical Minerals Strategy 2030. It identifies 26 critical minerals essential for clean energy and defence.

In 2023–24, the government committed $500 million through the Northern Australia Infrastructure Facility for critical minerals projects. Export Finance Australia also supports projects with loans and guarantees.

The US and Australia signed a compact on critical minerals cooperation in 2022. European and Japanese institutions have engaged in similar resource partnerships.

These frameworks secure market access for ASX critical minerals stocks and reduce sovereign concentration risks in supply chains.

Also Read: Rare Earth Elements: The Strategic Metals Driving Clean Energy and Defence

ASX Critical Minerals Stocks in Global Portfolios

ASX critical minerals companies are increasingly being approached as a target by institutional investors. Global investment funds want to be exposed to the lithium and rare earths supply. The market capitalisation of Pilbara Minerals was above $15 billion in 2023. Lynas Rare Earths’ market capitalisation was more than $6 billion.

The ETFs listed below include the stocks within sustainability-oriented portfolios. Investor aligns portfolios in the transition to clean energy and gains access to the growth of resource exports

The other indirect investment made by global car manufacturers is in Australian miners. Upcoming productions sign long-term offtake agreements with ASX-listed producers with Tesla, Toyota as well as Korean battery groups. These contracts ensure the terms of security of supply at decade like horizons.

Sustained Growth and Industry Momentum

The ten-year EV market growth will ensure long-term demand for battery metals and critical minerals. ASX-listed groups like Pilbara Minerals, Mineral Resources, and Lynas Rare Earths are already expanding production and investing in downstream processing technologies. Such initiatives make Australia competitive in the wake of changing battery supply chains, mainly where international clients focus on seeking secure and sustainable supply.

Dedication to long-term plans in international energy rather than market variation requires investment in innovation, integrated environmental, social, and governance strategies and strategic supply relationships. These moves are in tandem with the international determination to curtail climate change by reducing the use of internal combustion engine vehicles and transitioning to zero-emission vehicles within the next 15 years.

Investor Strategies for Energy Transition Exposure

Market watchers suggest diversified exposure across lithium, nickel, and rare earths. Pilbara and Allkem provide lithium volume exposure. Lynas delivers rare earth supply diversification. IGO offers nickel and lithium integration.

Investors monitor cost positions, project pipelines, and strategic partnerships. Sustainability credentials also shape capital allocation.

Funds view ASX critical minerals companies as structural growth opportunities linked to electrification and renewable energy transitions.

Conclusion

The prospects of ASX critical minerals firms extend far beyond quarterly briefings, encompassing a multi-decade journey that is ushering in the rise of electrification on the planet. The long-term outlook of electric vehicle purchases, with the strong markets held by the US/EU supply chain, can ensure the long-term demand for Australian critical mineral exports. Such a decade long trend provides a steady footing to investment, innovation, and further input in the global energy transition, reinstating the position of Australia as a giant in clean energy mineral supply.