The newly published fire maps have shown increased danger zones near houses as well as near energy corridors. More real estate has now been classified in higher exposure groups. Such a change in the situation alters the up and the loss probability assessment by the particular insurers.

Simultaneously, it changes how the government councils will control the planning. In case the maps indicate an increase in fire risk, the utilities will enhance monitoring of the area. The communities will be given stricter safety measures during times of bad weather. The updates are an indication of longer fire seasons as well as drier fuel conditions.

Urban sprawl near the bush makes it riskier as well. As the risk profiles expand, the insurers rethink their pricing assumptions. The riskier the situation is, the higher the premiums often are. There may also be an increase in excess levels. Some insurance policies may contain stricter maintenance clauses. The purpose of these actions is to minimise the severity of future claims.

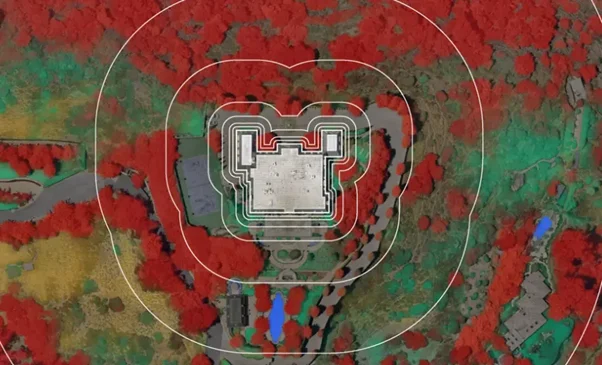

Updated hazard data reshapes insurance and planning decisions. [Nearmap]

Why Does Liability In Wildfire-Prone Areas Matter?

Liability has a significant value since it specifies who is responsible for the damage. Legal claims might arise when fires burn down houses. Insurers pay attention to liability in wildfire-prone areas when hazard ratings are on the rise.

The claims history is one of the inputs into risk pricing models. The increase in exposure leads to higher projected loss costs. This pressure is then translated into the premium structures. Utilities are under the same scrutiny as well. Sometimes fires lead to investigations concerning equipment malfunctions.

The areas of high risk need the implementation of very strong preventive measures, which consist of the clearing of the vegetation and installation of the fault detection systems. The councils are also responsible when it comes to their zoning approvals. When the planning turns a blind eye to the hazard data, then the legal risk is bound to rise. Therefore, the updated maps will affect several sectors simultaneously.

What Do These Changes Mean For Insurance Markets?

The insurance markets are quick to react to the signals regarding wildfire risk updates. The total exposure increases due to the expansion of broader hazard zones. Insurers, therefore, are adjusting their underwriting thresholds.

The new business might be subject to higher base rates. Existing customers might get the renewal adjustments. The coverage limits may also vary in the extreme areas. Besides, the reinsurers too are reacting to the changes in the hazard layers. The treaty pricing is determined by the potential of regional catastrophes.

The higher costs of reinsurance are passed on to the retail prices. In some areas, the capacity may become limited. That could lead to a reduction in competition. The investors keep a close watch on these signals. The accurate hazard modelling is the key to profitability. The quicker the updates, the faster the pricing cycles.

Pricing models shift as hazard data updates accelerate. [FasterCapital]

How Should Property Owners Respond To Risk Updates?

Mitigation steps can be taken by the property owners to lower their exposure. The spread of the flames is reduced by the clearing of dry vegetation. The ember-resistant vents minimise the risk of internal ignition.

The fire-resistant roofing is giving the property better chances to survive. These are the steps that contribute to the goals of wildfire property protection. The insurers are, by and large, taking such features into consideration during assessments. Some policies may now demand the declarations of maintenance.

The councils might also mandate the upgrading of buildings in the high-risk areas. It is very important to be aware of the local changes in the hazards. The risk ratings may change without any noticeable shifts in the environment. Taking early action helps to prevent future problems with insurance. Besides, community programs also enhance the potential for reducing losses on a collective basis.

What Are The Broader Economic Impacts?

Higher hazard classifications hurt the budgets of infrastructure. The power companies will have to upgrade their safety measures on the grids, and such an upgrading process will cost more. More monitoring systems will be installed, and the shut-off protocols will become standard.

These heavy capital investments will directly affect the operational costs in the long run. Accordingly, customers may have to pay higher service fees in the long run. The same thing takes place in the case of developers, who also have to incur new compliance costs. Besides, the projects that are already in the mapped-out danger zones will probably require more assessments.

Moreover, the building standards might become more stringent. All these costs work together to determine the quantity and price of housing units. The municipalities try to find a good compromise between the safety requirements and the need for development. The issue of the affordability of insurance is becoming a burning policy topic in the outback areas.

Infrastructure and housing costs respond to hazard reclassification. [The Australian]

What Comes Next For Wildfire Risk Management?

The future wildfire risk updates will be determined by the ongoing modelling. The use of satellite data has given a boost to the detection of the amount of fuel loaded. The projection of the climate has given a clearer picture of the fire behaviour forecast.

Therefore, the risk zones may get an extension. The Stakeholders would have to plan for the revisions to be done frequently. Insurers will have to adopt very flexible underwriting systems. The upkeep of the grid will have to be done according to the standards, and the utility companies will have to do it very quickly.

The data system for the council will have to be changed in line with the new zoning laws. The property owners who live in the wildfire area are still required to follow the mitigation guidance. To manage liability in areas that are prone to wildfires, it is necessary to share the responsibility. Coordinated action is the key to long-term resilience.

Also read: Canada wildfire season 2025: second-worst on record

FAQs

Q1: What is liability in wildfire-prone areas?

A1: It refers to legal and financial responsibility when fire damage occurs within mapped high-risk zones.

Q2: How do wildfire risk updates affect insurance?

A2: Updated hazard data can increase premiums, adjust excess levels, and tighten policy conditions.

Q3: Can home upgrades reduce wildfire risk?

A3: Yes, wildfire property protection measures can lower damage probability and support better insurance terms.

Q4: Do councils change rules after map updates?

A4: Yes, councils may revise zoning and building standards based on updated hazard classifications.