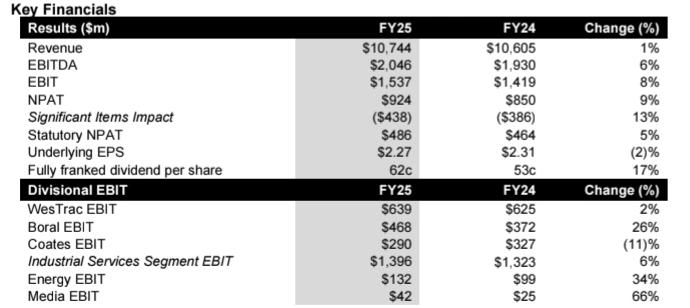

SGH Ltd (ASX:SGH) reported an EBIT of $1,537 million for FY25, which is an 8% increase from FY24. Revenue enjoyed a 1% growth to $10.7 billion, while NPAT improved by 9% to $924 million. EBIT margin witnessed an improvement of 93 basis points, closing at 14.3%.

Operating cash flow grew by 49% to $1,951 million, resulting in 2.0× of adjusted Net Debt/EBITDA ratio. SGH declared a fully franked final dividend of 32 cps, taking the FY25 dividend to 62 cps, up by 17%. A 46% total return to shareholders was delivered, well above the ASX100’s 15%.

SGH financial details

How Did SGH Divisions Perform?

WesTrac reported an EBIT of $639 million, relatively 2% ahead of revenues rising slightly by 4% to $6.1 billion. Equipment demand from WA for resources had to offset an approximately $60 million negative pricing impact associated with currency variations. Capital sales were up by 12% to $2.2 billion.

Boral reported a splendid EBIT of $468 million, showcasing increases of 26% and an improvement in margins by 255 basis points to 13%. Revenue grew by 1% to hit the $3.6 billion mark, supported by higher volumes of concrete and resilient commercial demand.

Coates went down with EBIT of $290 million, reflecting a 9% decline both in customer activity and revenue. The EBIT margin stayed strong at 27.8%, cushioned by cost controls and operational efficiencies.

The Energy segment saw production at Beach Energy rise by 9% to 19.7 MMboe, while revenue was up 13% to $2 billion. Developments are ongoing for Crux and Longtom gas projects.

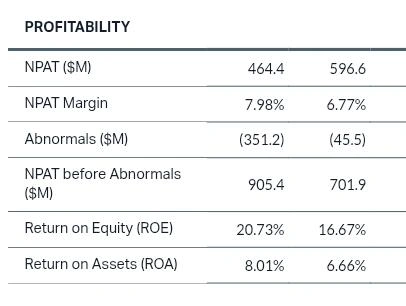

SGH profitability analysis

What Is the Market Size Driving SGH Growth?

SGH functions in sectors linked to Australia’s infrastructure and construction markets. The national pipeline is estimated at around 1.8 trillion dollars over the coming seven years. Housing demand is also huge, with 240,000 new homes being sought yearly to meet supply targets.

This strong market base ensures continued demand for the equipment, materials, and services offered by WesTrac, Boral, and Coates. Renewable energy, utilities, and defence are other growth areas alongside SGH’s positioning.

SGH Maintains Strong Capital Discipline

The group decreased net debt by 3% to reach $4.2 billion while maintaining liquidity at $1.9 billion. No major corporate facility maturities are due until FY29. Fixed-rate debt held 69% of borrowings with an average cost of 5.4%.

EBITDA Margins were at 19.1%, up 88 basis points, showing clear pricing discipline and operational efficiencies. SGH met its deleveraging target and is now set for future investment while sustaining shareholder returns.

How Are Investors Viewing SGH’s Outlook?

Market analysts continue to stay favourable on SGH and talk about the company outperforming its guidance and gaining operational momentum. Margin improvement and cash flow generation are thought to be among the company’s main strengths.

With leverage below 2x EBITDA and exposure to sectors with considerable demand, SGH will be well positioned to endure any market variability. Infrastructures market size coupled with energy investments should ensure medium to long-term growth.

FY26 guidance projects SGH toward low to mid-single digit EBIT growth, which is backed by continuous efficiency programs, strategic acquisitions such as Boral, and focus on high growth sectors.

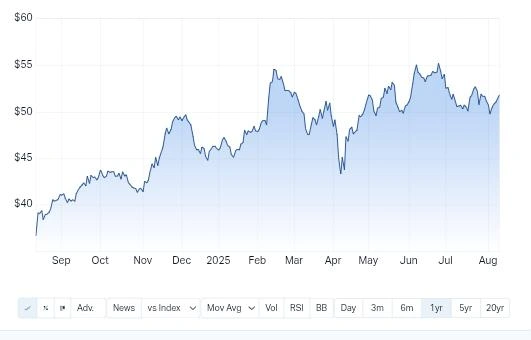

SGH Market Trend

Boral Acquisition Adds Strategic Value

Acquisition of Boral, coming full circle in 2024, further strengthened the SGH building materials capabilities. Operational synergies are becoming evident now-a-days with margins improving across the board and higher volumes coming from key markets.

There has been significant earnings growth through Boral’s optimisation programs and pricing discipline. Its performance is also synchronous with SGH’s operating model, the “SGH Way,” which puts a particular focus on efficiency, customer service, and disciplined capital allocation.

Also Read: Fortescue Breaks New Ground with RMB 14.2 Billion Syndicated Term Loan from Global Lenders

Final Thoughts: SGH Positioned for Sustainable Growth

SGH’s diversified industrial-service portfolio generates stable cash flows and is exposed to infrastructure demand in the long run. The Australian infrastructure pipeline is valued at around $1.8 trillion, and housing targets back the sustained demand for SGH’s services.

Energy projects such as Crux and Longtom also extend the long-term earnings profile. The company, with its conservative balance sheet and strong liquidity, protects its dividend-growth track record and; in turn, will give investors increased confidence regarding future returns.