The Reserve Bank of Australia faces a critical decision today, with mortgage holders and businesses watching closely. Will the central bank deliver another rate cut or hold steady at 3.60%?

Most economists expect the RBA to pause. But the real question isn’t about Tuesday – it’s about when the next cut arrives and how much further rates will fall.

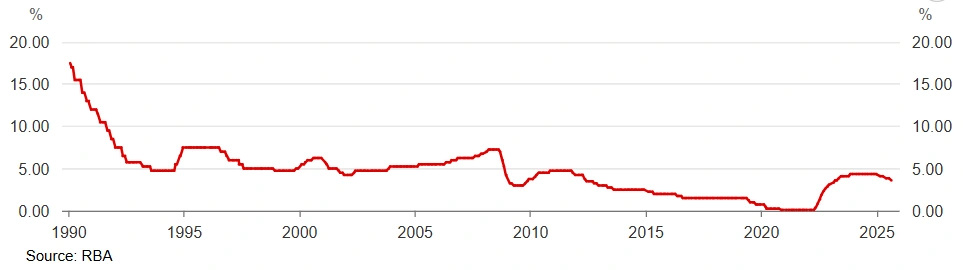

Three cuts have already landed in 2025. The RBA slashed rates in February, May, and August, bringing the cash rate down from 4.35% to 3.60%. Each cut delivered a 25 basis point reduction, offering relief to borrowers after years of aggressive tightening.

Yet inflation remains stubborn. Recent data shows prices climbing faster than expected, complicating the RBA’s decision-making process.

Big Four Banks Split on Timing

Australia’s major banks have made their predictions clear:

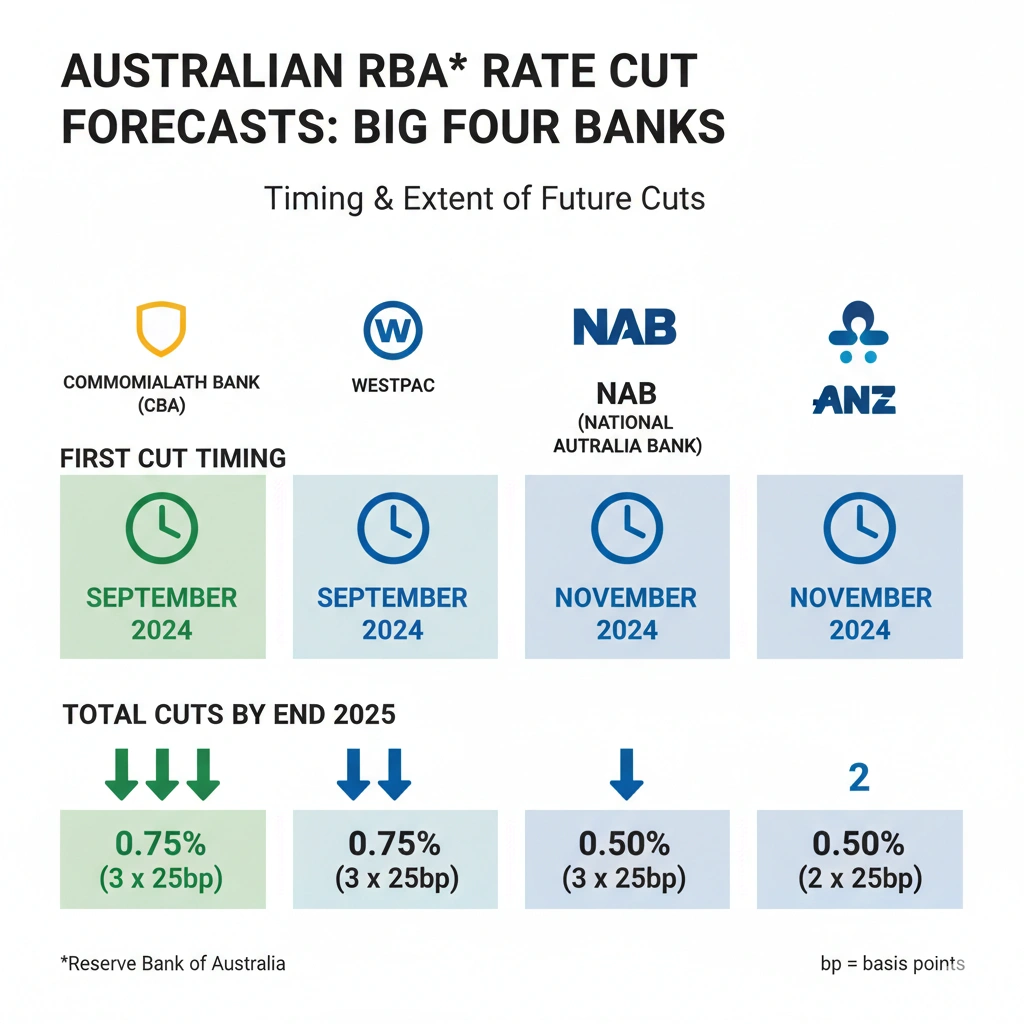

Commonwealth Bank expects the RBA to hold in September but cut again in November, taking the cash rate to 3.35% by year’s end. CBA economist Harry Ottley described the latest employment figures as “a mixed bag” but noted unemployment remains broadly in line with RBA forecasts.

ANZ also backs a November cut. The bank’s economists say September’s meeting “should pass with no change in rates,” with attention firmly on November’s decision.

Westpac maintains the same view—hold in September, cut in November. The bank’s chief economist Luci Ellis acknowledges risks have “tilted from favouring the downside towards something more two-sided.”

NAB stands alone among the majors. The bank reversed its earlier forecast and now expects no further cuts until May 2026. NAB economists point to “significantly hotter” services inflation as reason for their caution.

“We now see the RBA on hold at 3.60% until May 2026 as it will take some time for the RBA to rebuild confidence in the inflation trajectory,” NAB stated.

The cash rate fell from 4.35% to 3.60% in 2025 after peaking in November 2023.

Inflation Data Throws Curveball

The latest Consumer Price Index figures delivered an unwelcome surprise. Headline inflation hit 3.0% in August, up from July’s 2.8% and marking the highest level since July 2024.

The trimmed mean measure – the RBA’s preferred gauge – sits at 2.7%. That’s within the central bank’s target band of 2-3%, but the upward momentum has spooked some observers.

CBA economists warned that November’s cut is “by no means guaranteed” and will be “highly dependent on the data flow from here.”

Market services inflation remains particularly sticky. Restaurant meals jumped 1.3% and takeaway prices rose 1.5%. Vehicle maintenance costs climbed 1.1% for the quarter.

Housing costs tell a mixed story. Rents are cooling, with annual growth slowing to 3.7% – the slowest pace since November 2022. But electricity prices, while falling 6.3% in August, remain 24.6% higher over the year despite government rebates.

Employment Numbers Stay Resilient

The labour market continues defying predictions of a sharp slowdown. Unemployment held at 4.2% in August, with participation rates steady.

Full-time employment has shown surprising resilience. Job vacancies are declining, suggesting the labour market is gradually softening rather than collapsing.

This strength gives the RBA room to pause. Governor Michele Bullock has repeatedly emphasised the board’s focus on maintaining full employment while keeping inflation in check.

The Australian economy’s performance remains a delicate balancing act. Growth is slowing but not stalling. Consumers are cautious but not panicking.

What RBA’s Statement Will Reveal Today

The RBA’s post-meeting statement at 2:30pm AEST will provide crucial clues about the board’s thinking. Economists will parse every word for hints about November.

Watch for language around:

- Inflation expectations – Has the August uptick changed the board’s confidence that prices will continue moderating?

- Labour market assessment – Does the RBA see unemployment rising enough to justify further easing?

- Global risks – How concerned is the board about international trade tensions and geopolitical uncertainty?

- Forward guidance – Will the statement signal openness to a November cut or suggest a longer pause?

The board will also consider developments in the US, where the Federal Reserve has begun its own easing cycle. But as RBA officials have stressed repeatedly, Australian policy decisions are made based on domestic conditions.

How Rate Decisions Impact Borrowers

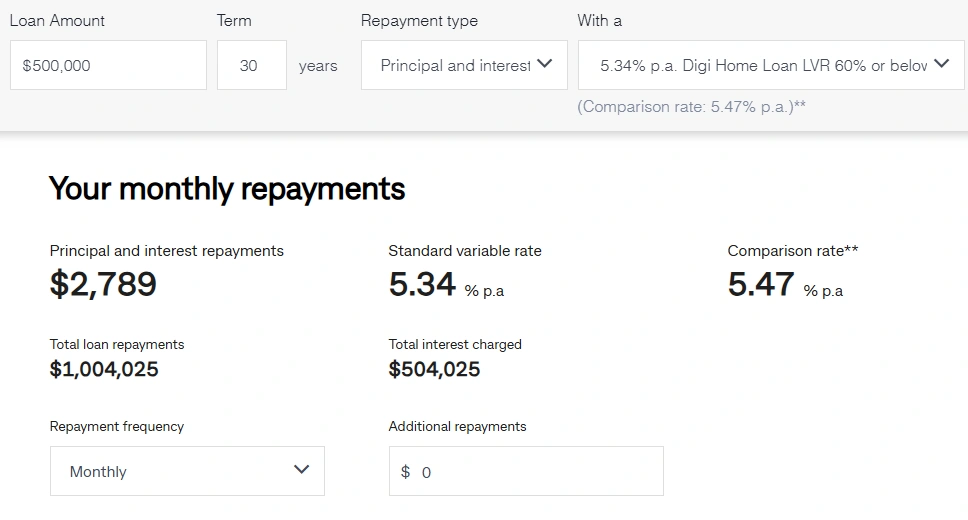

Variable rate mortgage holders have already benefited from the three cuts delivered this year. A borrower with a $500,000 loan has seen monthly repayments fall by roughly $105 since February.

If the RBA does cut in November, that same borrower would save another $35 per month. Over a year, the cumulative savings from four cuts would total around $1,680 annually.

But banks don’t always pass on the full rate reduction. Some lenders have been slower to adjust, while others have increased their margins. Borrowers should compare rates actively rather than assuming their bank will automatically deliver the best deal.

Three rate cuts in 2025 have reduced monthly repayments for variable rate borrowers.

Why NAB’s Forecast Matters

NAB’s decision to push back its rate cut forecast carries significant weight. The bank has access to extensive data through its business lending and transaction activity.

Their economists noted that market services inflation – covering everything from professional services to hospitality – remains substantially higher than expected. This suggests domestic price pressures aren’t cooling as quickly as hoped.

The RBA pays close attention to services inflation because it reflects embedded inflation expectations. Unlike goods prices, which can be volatile, service costs tend to be stickier and harder to reverse once they accelerate.

NAB’s forecast implies the RBA will need to see at least two more quarterly inflation readings within the target band before feeling comfortable cutting again. That timeline pushes the next move out to May 2026.

Global Context Adds Complexity

Australia doesn’t operate in isolation. US economic policy, Chinese growth, and European energy costs all influence the domestic outlook.

The US Federal Reserve has signalled its own easing cycle is underway. Chair Jerome Powell’s Jackson Hole speech in August indicated the Fed sees inflation moving toward the target, allowing for rate reductions.

But US conditions differ from Australia’s. American inflation has cooled more convincingly, and labour markets have loosened further. The Fed’s policy path doesn’t dictate the RBA’s decisions.

China’s economic slowdown poses risks to Australia through reduced demand for iron ore and other commodities. Weaker Chinese growth typically translates to lower export revenues and softer business investment.

Trade tensions add another layer of uncertainty. Tariff threats and geopolitical friction create downside risks to global growth, potentially justifying more aggressive easing. But they can also fuel inflation through higher import costs.

What Happens After November?

Even if the RBA does cut in November, questions remain about the final destination for rates. The so-called “neutral rate” – where policy neither stimulates nor restricts the economy – is hotly debated.

Before the pandemic, the neutral rate sat around 0.75%. Post-pandemic, most economists believe it’s risen to between 2.5% and 3.5%.

If the current cash rate of 3.60% sits above neutral, further cuts make sense to avoid unnecessarily restricting growth. But if neutral has risen more than expected, the RBA may need to pause soon to assess the impact of cuts already delivered.

Westpac’s forecast assumes cuts in November, February, and May, taking the cash rate to 2.85%. That would represent a terminal rate slightly below the midpoint of most neutral rate estimates.

Commonwealth Bank sees fewer cuts ahead, with the cycle potentially ending around 3.35%. ANZ’s forecast aligns with CBA’s view.

Bank forecasts diverge on the timing and extent of future rate cuts.

Housing Market Implications

Lower rates typically fuel property price growth. Sydney and Melbourne have already seen values rebound strongly in recent months.

PropTrack data shows the national median house price hit $805,000 in April 2025, with values up 48.6% since March 2020 lows. Further rate cuts could add fuel to this fire.

Some economists warn that aggressive easing risks creating another property boom, making housing affordability worse for first-time buyers. This concern has prompted calls for the government to complement monetary policy with targeted fiscal measures.

The RBA has consistently stated that house prices aren’t a direct target of monetary policy. But officials acknowledge that wealth effects from property values influence consumer spending and financial stability.

The Bottom Line

Today’s decision looks like a foregone conclusion – the RBA will hold. But the real story unfolds in the months ahead.

November’s meeting matters far more. By then, the board will have fresh quarterly inflation data and another month of labour market readings. If services inflation cools and unemployment edges higher, a November cut looks probable.

But if price pressures persist or employment stays surprisingly strong, the RBA may need to extend its pause well into 2026. NAB’s forecast might prove prescient.

For borrowers, patience appears necessary. The era of ultra-low rates won’t return, but further cuts remain likely over the next year. The question is how many and how fast.

RBA’s statement will offer the first real clues since August’s surprise cut. Until then, mortgage holders can only watch and wait.

Also Read: Another Triple-Zero Failure Rocks Optus as Questions Mount Over Network Reliability

FAQs

- When is the RBA’s September decision announced?

The RBA will announce its decision at 2:30pm AEST on Tuesday, September 30, 2025. Governor Michele Bullock will address the media shortly after.

- What is the current cash rate?

The official cash rate sits at 3.60% after the RBA cut by 25 basis points in August 2025. This followed earlier cuts in February and May.

Will the RBA cut rates in September?

Most economists expect the RBA to hold the cash rate at 3.60% in September. Market pricing shows minimal chance of a cut at Tuesday’s meeting.

- When will the next rate cut happen?

Forecasts vary. CBA, ANZ, and Westpac predict November. NAB has pushed its forecast out to May 2026. The decision depends on upcoming inflation and employment data.

- How do RBA decisions affect home loans?

Variable rate mortgages typically adjust within weeks of an RBA decision. Fixed rates respond to market expectations about future moves. Not all banks pass on the full rate change.

- Is inflation under control in Australia?

Headline inflation sits at 3.0% annually as of August 2025. The trimmed mean measure—which the RBA watches closely—is at 2.7%, within the target band but showing recent upward movement.

- What happens if the US cuts rates but Australia doesn’t?

Interest rate differentials affect exchange rates and capital flows. A wider gap between US and Australian rates could strengthen the Australian dollar, making imports cheaper but hurting exporters.