Australian families hoping for festive financial relief have been dealt a harsh blow. The Reserve Bank of Australia has killed off any chance of a pre-Christmas rate cut, leaving more than 1.3 million mortgage holders in financial stress.

The decision came after inflation jumped unexpectedly to 3.5% in September, catching policymakers off guard and raising fears that borrowing costs could stay elevated well into 2026.

For thousands of households already stretched thin, this Christmas will be anything but merry.

The Numbers Behind the Pain

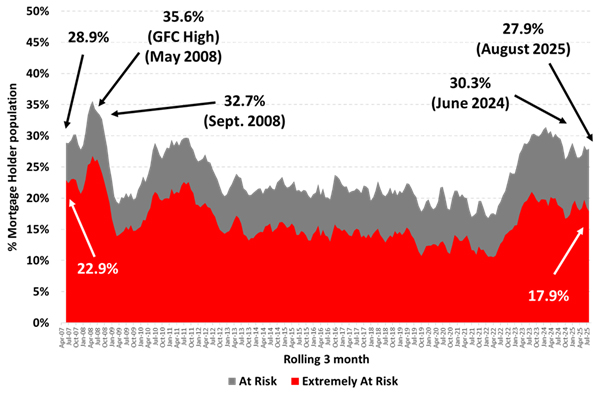

Over 25% of Australian mortgage holders, approximately 1.3 million people, are now considered ‘at risk’ of mortgage stress. That’s a figure that would have been unthinkable just three years ago when interest rates sat at historic lows.

The situation has deteriorated despite three rate cuts earlier this year that brought the cash rate down from 4.35% to 3.60%. Those reductions provided some breathing room, but not enough to offset the sharp increases that began in mid-2022.

Mortgage holders with a $500,000 loan saw their monthly repayments jump by $1,210 between April 2022 and April 2024, assuming lenders passed on the full rate increases.

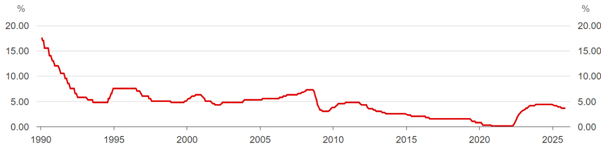

RBA cash rate trajectory showing the sharp increases from 2022 and modest cuts in 2025

Why Christmas Relief Won’t Come

The RBA’s November decision to hold rates steady wasn’t surprising to economists. What caught many off guard was how sharply inflation had risen in just three months, from 1.9% in June to 3.5% in September.

RBA Governor Michele Bullock described the September quarter figures as “materially higher than expected”. The board attributed the spike to higher petrol prices, increased council rates, and the rollback of electricity rebates.

But there’s more to the story. Economists believe stronger consumer demand in travel and recreation sectors is also creating upward pressure on prices.

The central bank’s message was clear: further rate cuts aren’t coming until inflation is firmly under control.

Banks Pull the Rug on Fixed Rates

Adding insult to injury, ME Bank withdrew its competitive 4.99% two-year fixed rate offering on Monday. The move signals that lenders expect rates to stay higher for longer.

Compare the Market economic director David Koch said the withdrawal was “another signal the RBA was unlikely to budge on rates until well into next year”.

For borrowers hoping to lock in low rates, the window is rapidly closing. Fixed rates starting with a ‘4’ are becoming increasingly rare across the banking sector.

What Economists Are Saying

The outlook for 2026 remains mixed. Major banks have revised their forecasts significantly:

- ANZ predicts a 25 basis point cut in March 2026, taking the cash rate to 3.35%

- NAB expects a cut in May 2026 to 3.35%

- Westpac forecasts two cuts in May and August 2026, bringing rates to 3.10%

- Commonwealth Bank currently doesn’t predict any further cuts in the near term

Warren Hogan, chief economic adviser at Judo Bank, warned that expecting the next move in interest rates to be downward is “completely inappropriate” given current economic conditions.

The Global Context Matters

Australia isn’t alone in grappling with persistent inflation. The US Federal Reserve recently cut its policy rate to a target range of 3.75-4.0% in October 2025, but Fed Chair Jerome Powell struck a hawkish tone, warning that further cuts aren’t guaranteed.

The cautious stance from central banks worldwide reflects uncertainty about whether inflation has been truly tamed or is simply taking a breather before rising again.

What This Means for Families

The impact on home loans during Christmas extends beyond just higher monthly repayments. Families are cutting back on discretionary spending, delaying purchases, and reconsidering holiday plans.

Roy Morgan data shows that mortgage stress levels, while down from their August peak, remain elevated at 25.3% of mortgage holders in October.

For a household with a $600,000 mortgage, even a 0.25% rate cut would reduce monthly repayments by approximately $92. But with the RBA’s December 9 meeting, its last chance to act before Christmas, now looking unlikely to deliver relief, those savings won’t materialise.

Percentage of Australian mortgage holders at risk of mortgage stress, October 2025

One Small Silver Lining

Not all hope is lost. The RBA’s updated forecasts show trimmed mean inflation peaking at 3.2% before falling to 2.6% by the end of 2027.

If inflation continues to moderate and economic growth remains subdued, the central bank will eventually have room to cut rates. The question is how long mortgage holders will have to wait.

Governor Bullock stressed that the RBA “can respond where the risks arise”, suggesting the board remains data-dependent and willing to adjust course if conditions warrant.

Also Read: NSW and Queensland Heatwave And Storms: Residents Brace For Catastrophe

The December Decision

All eyes are now on the RBA’s December 8-9 meeting. A monthly Consumer Price Index report due on November 26 will provide crucial data ahead of that decision.

If inflation shows signs of cooling, there’s a slim chance the RBA could deliver a surprise Christmas gift in the form of a rate cut. But based on current signals, most experts aren’t holding their breath.

For Australian mortgage holders, this Christmas looks set to be one of financial strain rather than festive cheer. The combination of stubborn inflation and elevated interest rates means many families will be tightening their belts instead of loosening their purse strings.

FAQs

Q: Will the RBA cut interest rates before Christmas 2025?

A: Based on current economic conditions and recent inflation data, a rate cut at the December 9 RBA meeting is highly unlikely. Most economists expect rates to remain on hold through the end of 2025.

Q: How much could mortgage holders save if rates are cut?

A: A 0.25% rate cut would save approximately $92 per month on a $600,000 mortgage, or $154 per month on a $1 million loan, based on current average variable rates.

Q: What’s causing inflation to remain high?

A: Key factors include higher petrol prices, increased council rates, rollback of electricity rebates, and stronger consumer demand in sectors like travel and recreation.

Q: When will interest rates go down in Australia?

A: Major banks predict the next rate cuts won’t occur until March-May 2026 at the earliest, depending on how inflation trends over the coming months.