Australia’s flagship carrier has soared to new financial heights. Qantas Airways reported a stellar FY 2025 underlying profit $2.4 billion, marking its second-highest annual profit on record and cementing its position as a dominant force in the global aviation recovery.

The airline’s underlying profit before tax reached $2.39 billion, representing a robust 15% increase from the previous year’s $2.08 billion. This impressive Qantas FY 2025 performance reflects the sustained rebound in travel demand following the pandemic disruption.

Record-Breaking Financial Performance Highlights Recovery

The numbers tell a compelling story of resilience and strategic execution. Statutory profit after tax climbed 28% to $1.61 billion, while total revenue increased 8.6% to $23.8 billion.

Passenger revenue emerged as the primary growth driver, surging to $20.4 billion from $18.9 billion in FY2024. This 7.9% increase demonstrates the airline’s ability to capitalise on pent-up demand for both domestic and international travel.

CEO Vanessa Hudson emphasised the significance of these results. “The numbers speak for themselves,” she stated, highlighting the company’s focus on balancing financial strength with investments in customer experience and employee welfare.

| Metric | FY2024 | FY2025 | Change |

| Underlying Profit Before Tax | $2.08B | $2.39B | +15% |

| Statutory Profit After Tax | $1.25B | $1.61B | +28% |

| Total Revenue | $21.9B | $23.8B | +8.6% |

| Passenger Revenue | $18.9B | $20.4B | +7.9% |

Source: Qantas Airways Financial Reports

Jetstar Emerges as Standout Performer

The budget subsidiary delivered exceptional results that exceeded all expectations. Jetstar’s underlying earnings skyrocketed 54% to $769 million, driven by record passenger numbers reaching 16 million domestic travellers.

This performance reflects the strategic wisdom of Qantas’s dual-brand approach. While the premium Qantas brand captures high-yield business and leisure travellers, Jetstar successfully targets price-sensitive segments without cannibalising the parent company’s market position.

The subsidiary’s success stems from several key factors:

- Record domestic passenger volumes of 16 million

- Enhanced operational efficiency and cost management

- Strategic route optimisation targeting underserved markets

- Improved load factors across the network

International Operations Drive Growth Momentum

Qantas’s international segment contributed significantly to the stellar results. International operations delivered a 20% earnings increase, supported by a 6% capacity expansion that aligned perfectly with recovering demand patterns.

The International Air Transport Association (IATA) projects global air travel demand growth of 5.8% in 2025, measured in Revenue Passenger Kilometres. This forecast supports Qantas’s optimistic outlook for continued international expansion.

Key international performance drivers included:

- Strategic capacity increases on high-demand routes

- Premium cabin revenue growth exceeding economy segments

- Cargo operations maintaining strong yields

- Partnership agreements enhancing network connectivity

The airline’s Project Sunrise initiative, featuring ultra-long-haul flights to New York and Europe, remains on track for Q1 2027 commencement. These routes will position Qantas as the only carrier offering non-stop services between Australia’s east coast and major European destinations.

Also Read: US Tariffs on Palladium & Silver: Markets Underestimate 2025 Risk Premium

Fleet Modernisation Supports Long-Term Strategy

Qantas announced a significant fleet expansion with an order for 20 additional Airbus A321XLR aircraft, bringing the total order to 48 units. These narrow-body aircraft offer an impressive 8,700-kilometre range, enabling new route possibilities across Southeast Asia and the Pacific.

The A321XLR deliveries, scheduled from 2028, will replace ageing Boeing 737-800s while providing enhanced fuel efficiency and passenger comfort. Initial deployment will focus on high-frequency domestic routes including Sydney-Melbourne and Sydney-Perth from mid-September 2025.

This forms part of a broader $20 billion capital expenditure programme spanning five years, with $3-3.5 billion allocated for FY2026. The investment demonstrates management’s confidence in long-term demand recovery and positions the airline for sustainable growth.

Challenges and Controversies Cloud Success

Despite the impressive financial performance, Qantas faced significant operational and legal headwinds during FY2025. The Federal Court imposed a $90 million penalty for the unlawful outsourcing of 1,800 ground staff in 2020.

This penalty followed a separate $120 million compensation settlement with affected workers, proposed by the Transport Workers Union. The court ruling described the outsourcing as a “deliberate bid to cripple union bargaining power,” highlighting ongoing tensions between management and employee representatives.

Additionally, a cyber attack exposed 5.7 million customer records, prompting substantial investments in data security infrastructure. While no direct compensation was required, the incident damaged customer trust and necessitated costly remediation efforts.

Union representatives representing over 30,000 employees criticised the profit announcement. They argued the results were “built on the back of an underpaid, disrespected workforce” and demanded fairer profit-sharing arrangements.

Industry Context Supports Optimistic Outlook

The aviation sector continues its steady recovery trajectory, with multiple forecasts supporting Qantas’s positive outlook. Boston Consulting Group projects 6.5% air travel growth, while McKinsey emphasises sustained momentum from resurgent business and leisure travel.

Regional dynamics particularly favour Australian carriers. Airports Council International anticipates 9.9 billion global passengers representing 4.8% year-over-year growth. The Asia-Pacific region, including Australia, is expected to lead this expansion due to robust inbound tourism and economic recovery.

| Source | Projected Growth | Metric |

| IATA | 5.8% | Revenue Passenger Kilometres |

| BCG | 6.5% | Overall Air Travel |

| ACI World | 4.8% | Passenger Traffic |

| Bain | 108% | Relative to 2019 Levels |

Global Aviation Demand Forecasts 2025. Source: Various Industry Reports

Several factors underpin these optimistic projections:

- Economic recovery momentum across key markets

- Reduced geopolitical tensions compared to 2024

- Corporate travel budgets returning to pre-pandemic levels

- Leisure travel demand remaining resilient despite economic headwinds

Shareholder Returns and Employee Benefits

Management balanced profit maximisation with stakeholder rewards through a comprehensive distribution strategy. Shareholders received a fully franked final dividend of 16.5 cents per share plus a special dividend of 9.9 cents, totalling $400 million in distributions.

This marked the first dividend payments since FY2019, reflecting management’s confidence in sustainable earnings recovery. The market responded enthusiastically, with shares reaching record highs following the results announcement.

Employees benefited from a new share plan providing $1,000 in Qantas shares annually for 25,000 staff members. The programme links rewards to financial performance, aligning employee interests with shareholder returns while addressing union concerns about profit distribution.

Also Read: Google to Invest $9 Billion in Virginia for Cloud and AI Expansion

Strategic Positioning for Future Growth

Looking ahead, Qantas FY 2025 results position the airline strongly for continued expansion. Management guides 3-5% domestic unit revenue growth into FY2026, supported by sustained demand across all market segments.

The company’s strategic priorities focus on several key areas:

- Fleet modernisation through the A321XLR programme

- International network expansion, particularly in Asia-Pacific

- Premium product enhancement to capture high-yield segments

- Operational excellence initiatives to improve reliability

- Sustainability investments to meet environmental targets

Project Sunrise represents the flagship growth initiative, with ultra-long-haul capabilities opening new market opportunities. The programme requires sophisticated logistics coordination, with aircraft assembly completion targeted for October 2025.

Market Response and Analyst Commentary

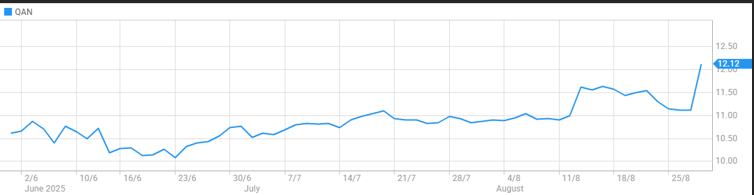

Financial markets demonstrated strong confidence in the results, with Qantas shares jumping 13% to $12.60 on announcement day. Trading volumes exceeded average levels as institutional investors repositioned portfolios.

Analyst coverage has been predominantly positive, with Seeking Alpha highlighting fair valuation metrics despite elevated earnings expectations. The consensus view suggests Qantas trades at reasonable multiples relative to earnings growth prospects.

Key analyst observations include:

- Strong execution of dual-brand strategy across market segments

- Effective capacity management balancing supply with demand

- Robust balance sheet supporting growth investments

- Premium positioning in domestic market providing pricing power

Operational Metrics Demonstrate Excellence

Beyond financial performance, operational indicators showcase the airline’s execution capabilities. Load factors improved across both domestic and international networks, while on-time performance maintained industry-leading standards.

The dual-brand strategy proved particularly effective in capturing diverse market segments. Premium Qantas services attracted business travellers willing to pay higher fares for service quality, while Jetstar successfully competed in price-sensitive leisure markets.

Customer satisfaction metrics showed steady improvement throughout FY2025, despite occasional service disruptions from industrial action and weather events. The airline’s Net Promoter Score increased across all customer segments, reflecting investment in service quality improvements.

Sustainability Initiatives and Future Challenges

Environmental considerations increasingly influence airline operations and investment decisions. Qantas committed to net-zero emissions by 2050, requiring substantial investments in sustainable aviation fuels and aircraft technology.

The A321XLR order partially addresses these concerns through improved fuel efficiency compared to older aircraft. However, achieving long-term sustainability targets will require continued fleet renewal and operational optimisation initiatives.

Industry-wide challenges remain significant:

- Rising fuel costs impacting operational margins

- Regulatory compliance costs for environmental standards

- Infrastructure constraints at major airports

- Skills shortages in technical and operational roles

CAE’s talent forecast predicts demand for 1.465 million new aviation professionals by 2034, highlighting workforce development as a critical success factor.

Investment Implications and Market Outlook

The Qantas $2.4 billion profit demonstrates the airline’s successful navigation of post-pandemic recovery challenges. Strong demand fundamentals, strategic fleet investments, and operational excellence position the company well for sustained growth.

However, investors should monitor several risk factors including fuel price volatility, regulatory changes, and competitive pressures from international carriers. The airline’s premium market positioning provides some protection against price competition but requires continued service quality investments.

The broader aviation recovery trajectory supports optimistic medium-term prospects. With international borders fully reopened and business travel patterns normalising, Qantas appears well-positioned to capitalise on sustained demand growth across its network.

Frequently Asked Questions

What drove Qantas’s strong FY2025 profit performance?

Strong travel demand recovery, effective dual-brand strategy, and international capacity expansion were primary drivers.

How does Qantas’s profit compare to pre-pandemic levels?

The $2.39 billion underlying profit represents the second-highest in company history, approaching 2023’s record $2.46 billion.

What is Qantas’s dividend policy going forward?

The company paid its first dividends since 2019, totalling $400 million, indicating confidence in sustainable earnings.

When will Project Sunrise flights commence?

Ultra-long-haul flights to New York and Europe are scheduled to begin in Q1 2027.

How many new aircraft is Qantas ordering?

The airline has 214 aircraft on order, including 48 A321XLR units, with deliveries every three weeks over two years.