The Productivity Commission suggests the introduction of a net cash flow tax to encourage investment. The reform would try to reverse the slowdown in Australia’s productivity with corporate tax reform.

Understanding the Net Cash Flow Tax Proposal

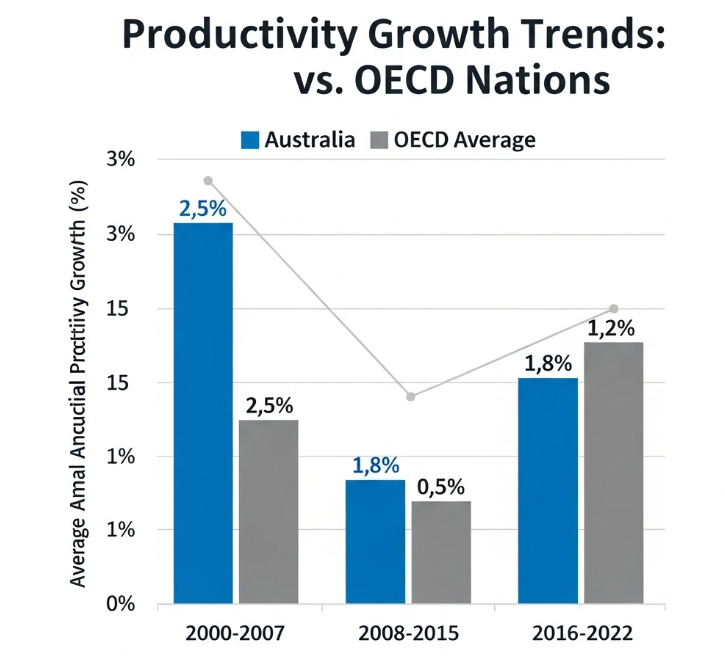

Australia is facing a grave economic issue. Its productivity growth has decelerated sharply. Economists identify “capital shallowing” as a key issue. This is where investment lags behind workforce growth. The company tax structure is being pushed to reform.

Hence, the Productivity Commission proposes a major overhaul. It calls for introducing a Net Cashflow Tax (NCFT). This would be along with a reduced company tax rate. The proposal is to stimulate investment and innovation.

The Problem: Australia’s Productivity Slowdown

Australia experienced strong economic performance for decades. Wealth was fueled by resource export and population growth. Recent history, however, shows alarming trends. Living standards are currently threatened by productivity slowdown.

The corporate tax system is to blame for this. Australia’s statutory rate of 30% is high in the world. This raises the problem of competitiveness. It deters investment in industry that is capital-intensive.

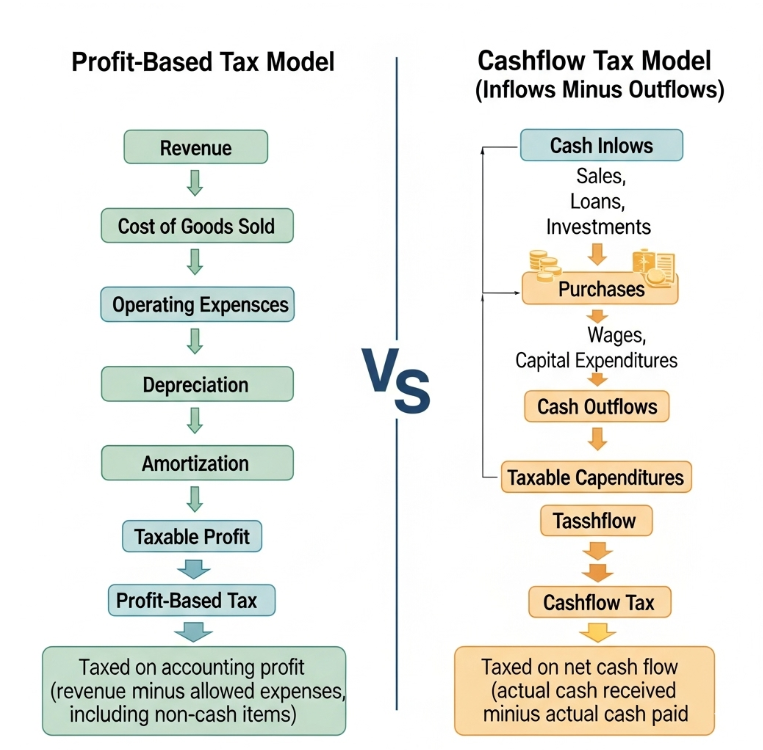

Mechanics of the Proposed Net Cash Flow Tax

The NCFT proposal offers a new paradigm. It would tax large firms’ net cash flows at 5%. It replaces traditional profit-based taxation.

The Net Cashflow Tax would tax cash inflows and outflows instead of traditional profit measures

One aspect is immediate expensing of capital investment. Firms deduct expenses in full upon payment. The model bars interest expense deductibility. It aims to capture supernormal profits, or economic rents, in particular.

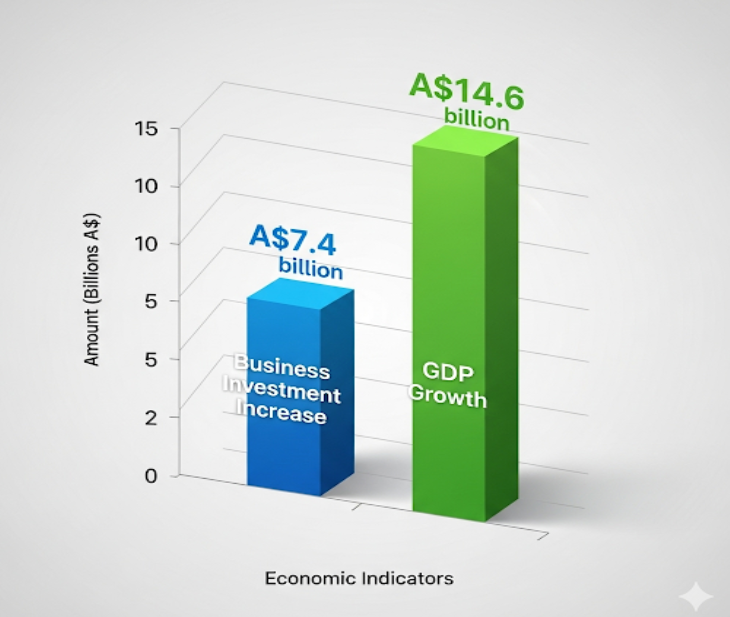

Projected Economic Gains from the Net Cashflow Tax Plan

Economic modelling proposes enormous benefits. The Productivity Commission suggests a significant increase in investment. Business investment would rise by A$7.4 billion per annum.

Modeling by the Productivity Commission suggests the Net Cashflow Tax could lift annual business investment by A$7.4 billion

Long-term GDP could increase by A$14.6 billion. Labor productivity would also substantially increase. These gains are the basis for wage rises and increased living standards. The federal budget would be zero-sum.

Implications for Small and Medium-Sized Enterprises

Small and medium-sized businesses immediately gain from this plan. Their effective tax rate would be cut to 20%. This renders them more competitive immediately.

Lowering the corporate tax rate to 20% would give smaller firms more room to expand and innovate.

Lower taxation frees up funds to drive business expansion. Start-ups and growing businesses receive necessary support. This could stimulate innovation and entrepreneurship.

Economic Theory Supporting the Net Cashflow Tax Model

Several theoretical benefits are highlighted by economists. NCFT is aligned with efficient tax principles. It targets rents instead of normal profit, lowering investment distortion.

https://www.youtube.com/watch?v=On4B4ILdUZ4&t=2s

Spendings are financed immediately, which boosts reinvestment cash flow. Firms receive costs upfront, relieving financing stress. It also puts funding channels on an even basis.

Overcoming the Capital Shallowing Difficulty

The reform addresses capital shallowing directly. By inducing investment, it boosts asset-per-worker ratios. This is crucial for long-term productivity growth.

The strategy is not a short-term fix, it is a structural reform. It addresses underlying causes of weakness in investment. This offers a sustainable path to regained prosperity.

Concerns Raised by the Business Council of Australia

There can be advantages, but there is great resistance. The Business Council of Australia warns against discouraging investment. It is fearful of uncertainty and capital flight.

Industry groups caution the Net Cashflow Tax could discourage large-scale investment projects.

Large companies are particularly vocal. They argue the tax deters reinvestment and low-margin growth. It can discourage long-term investment projects.

Challenges of Implementation and Administrative Costs

Transition woes create the biggest realistic problem. A shift towards a cash flow method entails a high level of adjustment. Accounting systems require radical revamps.

The Australian Taxation Office necessitates new systems of compliance. Administrative expenses could be significant at first. These expenses plague many observers.

Balancing Global Competitiveness and Domestic Priorities

Global tax competition drives this discussion. Corporate tax rates have fallen in many countries recently. Australia needs to stay competitive as an investment destination.

Multinationals are comparators of jurisdictions. Any suggestion that a country does not treat them well might steer investment elsewhere. This is especially true for large, footloose companies.

Comparisons with International Tax Experiments

There are relevant case studies across other countries. Norway has imposed a rent tax on petroleum income successfully. However, this is on a narrow high-return industry.

The United Kingdom entertained more widespread cashflow taxation but recoiled. Volatility and administration issues limited take-up. The above examples refer to implementation issues.

Political Obstacles to Corporate Tax Reform in Australia

Tax reform is faced with political challenges time and again. Business Council opposition is heavy. Bipartisan support is rarely available for wholesale overhaul.

Also Read: Good Friday Appeal 2025 Smashes Record, Raising $24 Million for Royal Children’s Hospital

Company tax reduction is questioned by the public. Reform fatigue can hold back comprehensive policy overhaul. Sufficient explanation of benefit is essential to success.

Potential Transitional Measures to Ease Adoption

The plan is a policy trade-off of the traditional sort. Theoretical efficiency is being weighed against practical business realities. Economically refined in theory, risk in implementation is high.

Phase-in could reduce some fears. Feasibility can be supported by sector-specific adaption. Institutional capacity needs to be strong.

The Global Tax Context and Australia’s Position

Domestic policy is affected by global tax trends. The OECD global minimum tax affects planning drivers. Australia must coordinate domestic reform with global norms.

This eliminates double taxation concerns. Taking advantage of potential loopholes is also forestalled. Effective design can potentially balance national and international objectives.

Also Read:Ancient Rocks in Australia Reveal New Niobium Deposit for Clean Energy and Steel

Future Outlook for the Net Cashflow Tax Proposal

The introduction of the Net Cashflow Tax is revolutionary reform. It addresses fundamental productivity issues directly. Economic modeling suggests tremendous potential advantages.

The future of the Net Cashflow Tax depends on political consensus, business support, and careful phased implementation

Implementation difficulties of a significant order do exist. Resistance from business creates political obstacles. Phased-in introduction over time and effective design could alleviate opposition.

Australia’s productivity future requires innovative solutions. Whether this proposal advances depends on multiple factors. Practical feasibility must balance theoretical economic advantages.

The debate continues among policymakers and stakeholders. Further refinement may improve the proposal’s acceptability. Ultimately, Australia needs solutions that boost investment sustainably.