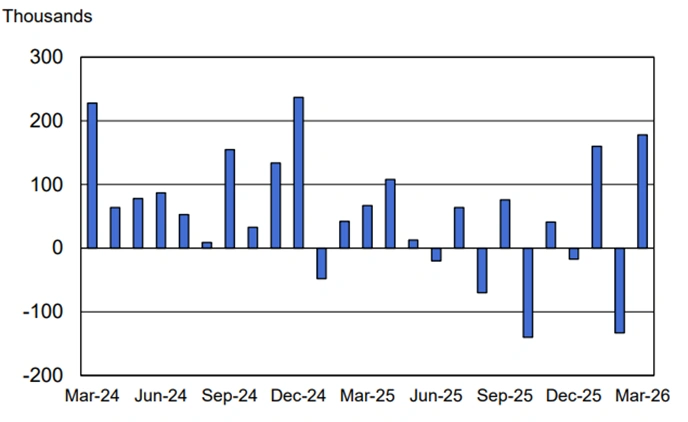

The March 2026 jobs report has delivered a clear rebound for the United States labour market. The US economy added 178,000 jobs in March, recovering sharply from the revised loss of 133,000 jobs recorded in February 2026.

Figure 1: Job listings highlighted in a newspaper under a magnifying glass, a representation of employment trends [Courtesy: Freepik]

The result brings monthly job creation closer to the 160,000 positions added in January 2026. However, the March 2026 jobs report is prompting a deeper conversation within the Federal Reserve about what a genuinely healthy labour market looks like in 2026.

The Fed Interest Rate Outlook Is Being Shaped by a Shifting Labour Market

Federal Reserve officials are revisiting long-held assumptions about job growth benchmarks. The Fed interest rate outlook is increasingly tied to a structural change in workforce dynamics, specifically a sharp decline in net immigration that is pushing labour force growth toward zero.

San Francisco Fed President Mary Daly Reframes What Zero Job Growth Can Mean

San Francisco Federal Reserve Bank President Mary Daly addressed the shifting landscape directly in a blog post published on 4 Apr 2026. Daly wrote that changes in government policies reducing immigration mean that the traditional rules of thumb for labour market health are changing.

“The speed limit of the labor market will likely be different,” Daly wrote. She added that when labour force growth was running at 1% to 2%, a zero job growth month was a warning signal for a potential recession. Under current conditions, that calculation no longer holds.

“Conveying that a zero-job growth economy is consistent with full employment is not easy,” Daly wrote. “But with labor force growth near zero, a ‘zero’ or even a negative month of net job gains could be consistent with expectations and not necessarily a sign of weakness.”

A New Fed Paper Puts the Breakeven Job Growth Rate Near Zero

A new paper published by the Federal Reserve, authored by Seth Murray and Ivan Vidangos, finds that the breakeven pace of job creation in 2026 could fall significantly below even the historic lows reached during the pandemic. Key findings from the paper include:

- The rapid slowing of net immigration may translate into a large drop in labour force growth

- The breakeven pace of job creation could fall to nearly zero in 2026

- Fewer than 10,000 new jobs per month may be sufficient to maintain a stable US unemployment rate 2026

- Fed Governor Chris Waller has independently noted that zero job growth would not necessarily signal an unhealthy labour market

- Waller pointed to the same immigration-driven shift as driving expectations of near-zero labour force growth this year

The March 2026 Jobs Report in Context: Three Months of Volatile Data

The March 2026 jobs report completes a volatile opening quarter for US employment data. January 2026 delivered 160,000 job gains, February 2026 saw a revised contraction of 133,000 positions, and March 2026 has now rebounded to 178,000 additions.

Figure 2: US nonfarm payroll employment monthly changes from March 2024 to March 2026 [Courtesy: Bureau of Labor Statistics]

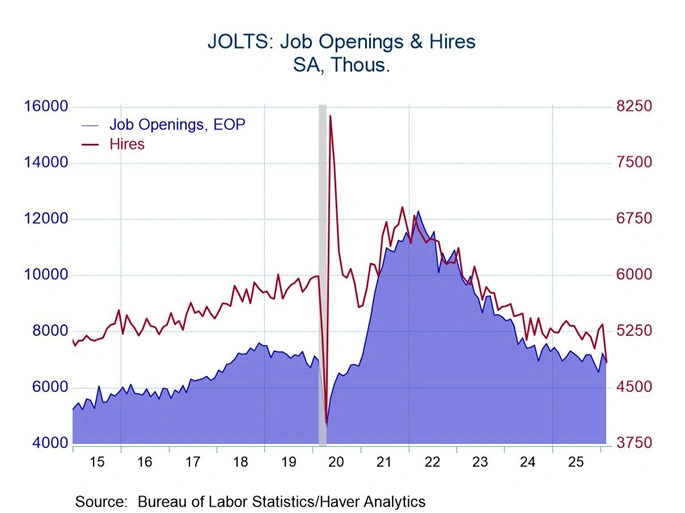

Hiring Rates and Job Openings Are Telling a More Cautious Story

Beyond the headline March 2026 jobs report figure, underlying labour market data paints a more measured picture. The US hiring rate has slowed to 3.1%, the weakest pace since the early days of the pandemic and the lowest level since 2011, according to data from the Labor Department.

JOLTS Data Shows a Decline in Total Hires

The Job Openings and Labour Turnover Survey released by the Bureau of Labor Statistics showed that US hires totalled 4.8 million in the most recent month. That figure is down by 387,000 compared with the same period a year earlier, adding context to the Fed interest rate outlook and reinforcing why policymakers are looking beyond headline job creation numbers.

Figure 3: JOLTS data showing trends in job openings and hires in the United States [Courtesy: Bureau of Labor Statistics]

The US Unemployment Rate 2026 and the Metrics Daly Is Watching Instead

Mary Daly has signalled that job growth alone is no longer a reliable single measure for assessing labour market health. She is placing greater emphasis on a broader set of indicators that better account for changes in workforce size.

Four Indicators Replacing the Old Jobs Growth Rule of Thumb

The metrics Daly is prioritising as alternatives to headline job creation are the employment-to-population ratio, the US unemployment rate 2026 trend, the quits rate, and the hiring rate. These measures account for shifts in the size of the workforce and offer a more accurate picture of whether the labour market is genuinely in balance.

Daly also acknowledged that fewer job gains are likely to translate into slower economic growth overall. She noted that productivity improvements could help offset some of that slowdown, but only if those gains prove persistent over time.

Industry Outlook

The US labour market is entering a period of structural recalibration. Declining net immigration is fundamentally altering the growth rate of the workforce, which in turn is shifting the benchmarks that economists and policymakers use to assess full employment.

For investors and businesses, a lower breakeven pace of job creation reduces the risk of the Federal Reserve interpreting soft monthly job numbers as recessionary. This recalibration may allow the Fed interest rate outlook to remain more accommodative than historical models would suggest, even in months where job gains are modest or near zero.

Future Direction and Impact on the US Economy and Financial Markets

The March 2026 jobs report has stabilised near-term sentiment about the US labour market. However, the broader shift in how the Federal Reserve interprets employment data will have lasting implications for the Fed interest rate outlook throughout 2026 and beyond.

If labour force growth remains near zero and job creation follows, the Fed may have more flexibility to hold or reduce rates without triggering concerns about an overheating or weakening economy. The US unemployment rate 2026 will remain a key indicator, but it will be read alongside a wider set of metrics that better capture the structural changes now underway.

For financial markets, the central question is whether this recalibration of benchmarks provides the Fed with the confidence to ease monetary conditions, or whether persistent inflation concerns keep the Fed interest rate outlook on hold regardless of what the labour market data shows.

Frequently Asked Questions

Q1. What did the March 2026 jobs report show?

Ans. The US economy added 178,000 jobs in March 2026, rebounding from a revised loss of 133,000 jobs in February and broadly in line with the 160,000 jobs created in January 2026.

Q2. Why is the Fed saying zero job growth could be acceptable?

Ans. A sharp decline in net immigration is pushing labour force growth toward zero. With fewer workers entering the workforce, fewer new jobs are needed each month to maintain a stable US unemployment rate 2026.

Q3. What is the breakeven pace of job creation in 2026?

Ans. The breakeven pace could fall to nearly zero, meaning fewer than 10,000 new jobs per month may be sufficient to hold unemployment steady this year.

Q4. What metrics is the Fed now prioritising over headline job growth?

Ans. San Francisco Fed President Mary Daly is focusing on the employment-to-population ratio, the US unemployment rate 2026 trend, the quits rate, and the hiring rate as more reliable indicators of labour market health.

Q5. How does this affect the Fed interest rate outlook?

Ans. A lower breakeven pace of job creation may give the Federal Reserve more flexibility to hold or ease rates, even in months where job gains are modest, without interpreting weak numbers as a sign of recession.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on reporting available online, and data from the Bureau of Labor Statistics, the Federal Reserve, and the Job Openings and Labour Turnover Survey. Figures reflect data available at the time of the original source publication. Readers should conduct their own research and seek independent financial advice before making any investment or financial decisions. Colitco does not hold any position in the organisations or institutions mentioned.

Sources

https://www.bls.gov/news.release/jolts.nr0.htm

https://www.federalreserve.gov

Last modified: April 4, 2026