The Australian property market faces a significant correction risk. Experts warn that the local housing sector is highly vulnerable. Recent price drops in London serve as a stark warning. The United Kingdom’s capital saw a major downturn in late 2025.

Local analysts now monitor signs of similar stress in Australian cities. Australia’s residential property values reached nearly $12 trillion by the end of last year. This massive valuation creates a high-stakes environment for the national economy. High debt levels make many households sensitive to any market shifts.

London Property Values Tumble

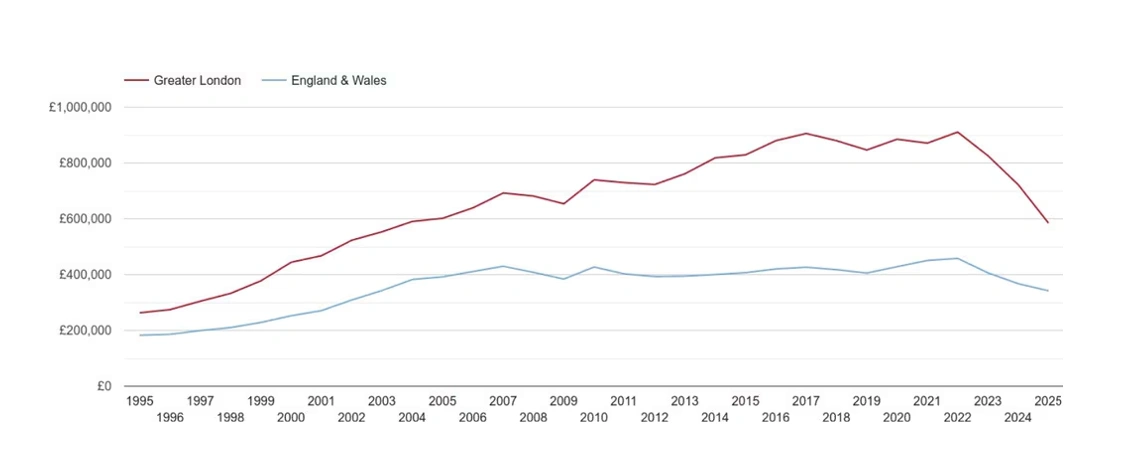

London house prices fell by 2.4% during 2025. Some wealthy districts experienced even sharper declines. Kensington and Chelsea recorded a massive drop of 16.5%. Prices in the City of London plummeted by 18%.

These figures show that even premium markets can collapse quickly. Higher service charges and interest rates drove many owners to sell. The London market now sees more sellers taking losses on their properties. This trend signals a major shift in global property sentiment.

London’s real house prices have fallen dramatically since 2022

London’s real house prices have fallen dramatically since 2022

Australian Markets Under Pressure

Australian house prices rose by 8.6% in 2025. However, this momentum is now slowing down significantly. The median value in Sydney sits above $1.28 million. High prices continue to stretch the budgets of ordinary Australians.

Many families now spend more on interest than in the 1980s. This occurs even though interest rates were much higher back then. Modern debt levels are far higher relative to household incomes. This creates a fragile foundation for future price growth.

Key Market Indicators

The following factors influence the current market stability:

- National residential debt reached $12 trillion recently.

- The median Sydney house price exceeds $1.28 million.

- Interest repayments consume a record portion of household income.

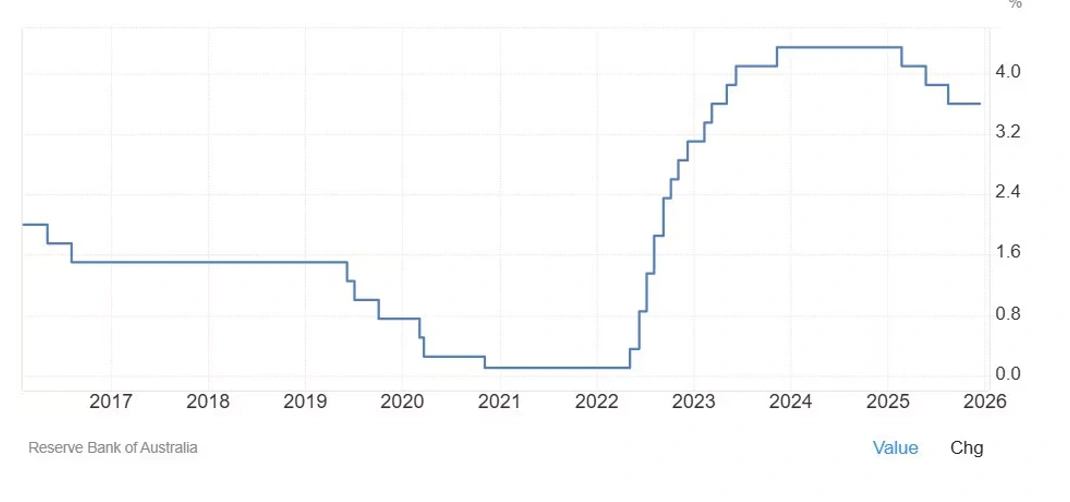

- The Reserve Bank of Australia cash rate remains at 3.60%.

Vulnerability to Global Shocks

Global economic trends often impact the local property landscape. The London crash proves that high valuations are not permanent. Australian property is currently estimated to be 40% overvalued. This makes it one of the priciest assets globally.

Investors now question whether growth can continue at previous rates. Stocks may actually outperform residential property over the next decade. Rental yields remain low at roughly 3.5% in capital cities. This yield is lower than many variable mortgage rates.

Regulatory Crackdown Commences

The Australian Prudential Regulation Authority is taking direct action. New debt-to-income limits start on 1 February 2026. Banks must limit high-risk lending to 20% of new loans. This policy targets buyers who borrow six times their annual income.

These rules will reduce the borrowing power of many investors. The crackdown aims to prevent a total market collapse. However, it may also reduce demand in the short term. Lower demand often leads to stagnant or falling property prices.

Expert Forecasts Slashed

CoreLogic research director Tim Lawless recently issued a sobering forecast. He slashed his 2026 growth expectations to 5% or lower. Lawless cites high value-to-income ratios as a primary constraint. Buyers simply cannot afford to pay more at current rates.

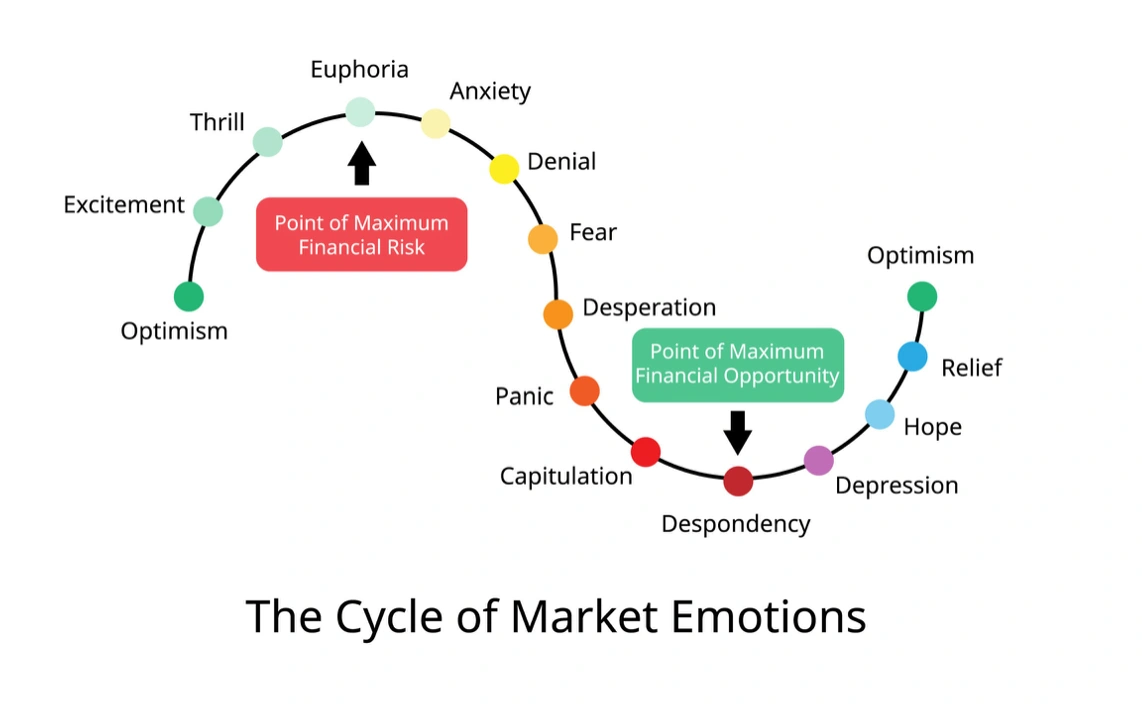

The cycle of market emotions

The cycle of market emotions

AMP chief economist Shane Oliver also expects more modest growth. He predicts a range between 5 and 7% for 2026. These figures are much lower than the gains seen in 2025. The era of rapid price increases appears to be ending.

Major Bank Rate Predictions

The “Big Four” banks remain divided on interest rate directions:

- ANZ: Predicts the cash rate will remain steady.

- CBA: Forecasts a 0.25 percentage point rise in February.

- NAB: Tips two rate hikes in February and May.

- Westpac: Expects rates to stay at current levels.

The Affordability Ceiling

Affordability acts as a firm handbrake on the Australian market. It takes over a decade to save a 20% deposit. This is double the time required during the 1990s. Younger generations struggle to enter the market without parental assistance.

Government schemes currently support the lower end of the market. The First Home Guarantee allows for 5% deposits. While this helps some, it also adds to overall demand. Artificial demand can inflate prices above their fundamental value.

Also Read: Australian Politics Coalition Breakdown: How It Unfolded

Regional Performance Divergence

Not all Australian cities face the same level of risk. Perth and Brisbane performed strongly throughout 2025. Values in Perth increased by nearly 16% last year. These markets benefit from strong migration and tight supply.

In contrast, Melbourne and Sydney show signs of exhaustion. Melbourne was the weakest performer among major capitals in 2025. Prices there rose only marginally over the twelve-month period. High supply in some areas continues to weigh on values.

Rising Inflation Concerns

Headline inflation recently hit 3.4% in Australia. This figure remains above the central bank’s target range. Sticky inflation makes interest rate cuts highly unlikely this year. Some economists actually fear further rate hikes are necessary.

Higher rates place immediate pressure on variable loan borrowers. A 0.25% hike adds $90 to monthly repayments for some. Many households already live on very tight margins. Any further increases could trigger a wave of forced sales.

Australia embarked on a rate-raising cycle in 2022

Australia embarked on a rate-raising cycle in 2022

Future Outlook for Homeowners

The second half of 2026 will be a testing period. Borrowing capacity will likely remain stagnant across the country. Buyers will hit an affordability ceiling by mid-year. This should lead to a more balanced market environment.

Investors must remain cautious of speculative risks in 2026. Experts suggest focusing on high-quality assets with good amenities. Avoid outer suburban developments with high investor concentrations. These areas are often the first to see price drops.