Light & Wonder has delivered a masterclass in operational efficiency. The gaming technology powerhouse reported third-quarter earnings that sent shares climbing despite falling short on revenue expectations.

The numbers tell a compelling story. Adjusted earnings per share soared 35% to $1.81, crushing analyst forecasts of $1.33. Net income jumped 78% year-over-year to $114 million. These gains came even as consolidated revenue of $841 million missed the $849.8 million target by a modest margin.

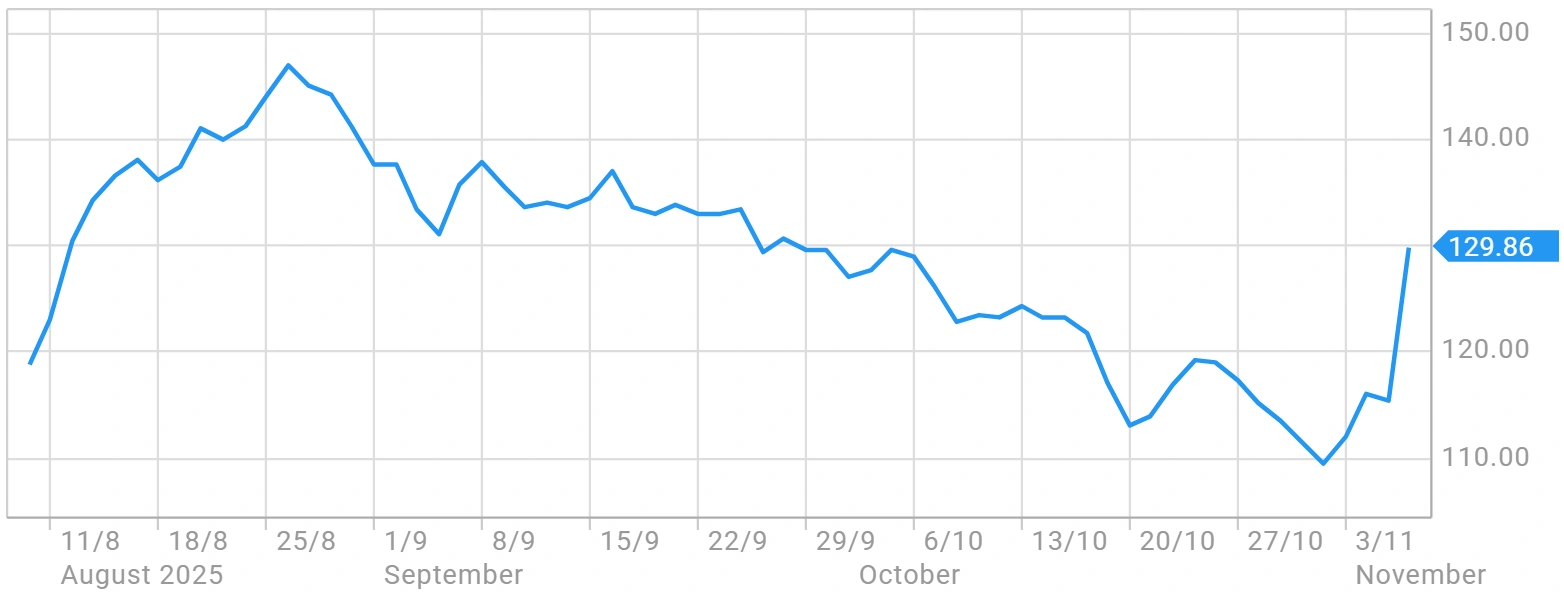

Wall Street seems willing to overlook the revenue shortfall. Light & Wonder’s stock rose 2.35% in aftermarket trading to $75.05 on 5th November 2025. Investors clearly focused on margin expansion and bottom-line growth rather than top-line misses.

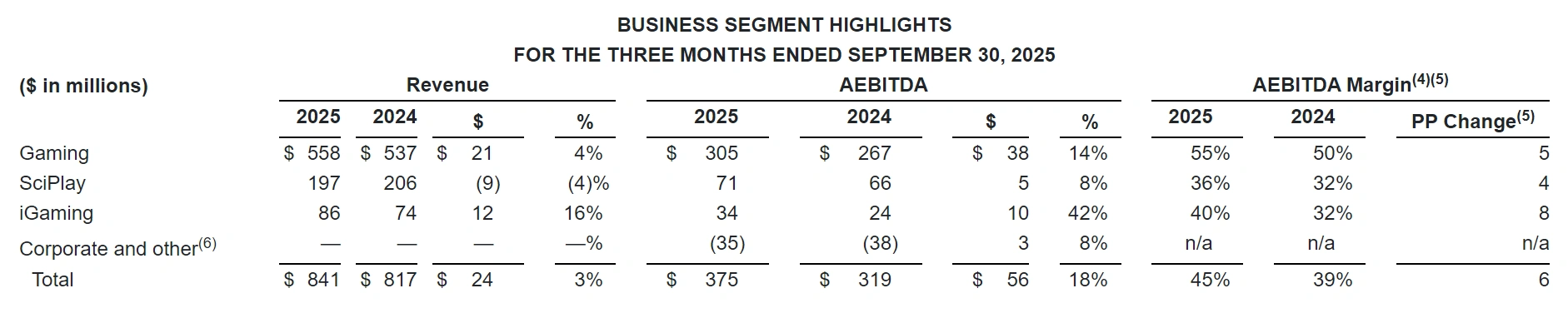

Gaming Operations Deliver 21 Straight Quarters of Growth

Light & Wonder’s gaming division continues its remarkable streak. The company marked its 21st consecutive quarter of growth in North American premium installed base.

Gaming revenue climbed 4% year-over-year to $558 million. The segment added 639 gaming operations units during the quarter, bringing the total to over 34,500 units across North America.

The recently acquired Grover charitable gaming business contributed $40 million to the quarter’s performance. Grover added 229 units sequentially, demonstrating successful integration ahead of schedule.

Key gaming metrics included:

- Gaming AEBITDA rose 14% to $305 million

- Margins expanded 500 basis points to 55%

- Base gaming operations revenue increased 15% year-over-year

- 21st consecutive quarterly increase in premium installed base

Business Segments Key Highlights

iGaming Sets Quarterly Records

The standout performer in Light & Wonder Q3 earnings was undoubtedly the iGaming segment. Revenue hit a quarterly record of $86 million, representing 16% growth compared to the prior year period.

AEBITDA in iGaming surged 42% to $34 million. The company attributed this success to sustained momentum in North America, first-party content proliferation, and partner network expansion.

Wagers processed through the iGaming platform reached unprecedented levels. Seven out of the top ten games across Light & Wonder’s Open Gaming System network were first-party titles, highlighting the effectiveness of the company’s content strategy.

The online gaming sector continues to experience explosive growth globally, with North American markets leading the charge.

Margin Expansion Drives Profitability

Light & Wonder’s ability to expand margins while growing revenue demonstrates operational excellence. Consolidated AEBITDA increased 18% to $375 million, with margins reaching 44.6%.

Operating margins improved dramatically from 19.5% in Q3 2024 to 27.2% in Q3 2025. Free cash flow margins also expanded significantly, rising from 5.9% to 16.2% year-over-year.

The company generated $184 million in net cash from operating activities during the quarter. Free cash flow reached $136 million, representing 55% and 64% year-over-year growth respectively.

Strategic ASX Listing Transition Progressing

Light & Wonder is moving forward with its transition to a sole primary listing on the Australian Securities Exchange. The company announced in its earnings release that the NASDAQ delisting is expected to be effective on 14th November 2025.

As of 4th November 2025, holders of 46.4 million shares, representing approximately 57% of total outstanding shares, had converted their shares to CHESS Depositary Interests tradable on the ASX.

Light & Wonder Share Price Performance Chart

President and CEO Matt Wilson stated: “This move simplifies our listing structure for shareholders and further enhances Light & Wonder’s profile within a gaming-attuned Australian market.”

SciPlay Shows Mixed Results

The SciPlay segment presented a more nuanced picture. Revenue declined 4% year-over-year to $197 million, primarily due to a decrease in average monthly payers at Jackpot Party Casino.

Despite the revenue dip, AEBITDA increased 8% to $71 million thanks to margin expansion. The direct-to-consumer platform reached record revenues of $40 million, representing 20% of total SciPlay revenue.

Social casino gaming companies continue to focus on quality player monetization through dynamic Live Ops and the SciPlay Engine, similar to strategies employed by other social gaming leaders.

Capital Return and Future Outlook

Light & Wonder returned $111 million to shareholders through share repurchases during the quarter. An additional $101 million was returned subsequent to quarter-end through 31st October 2025.

This brings the company to approximately 51% utilisation of its authorised $1.5 billion share repurchase program.

The company maintained its FY2025 consolidated adjusted AEBITDA target of $1.4 billion. Looking further ahead, Light & Wonder has set ambitious targets for fiscal year 2028, including consolidated AEBITDA of $2.0 billion and adjusted EPS of $10.55.

Matt Wilson emphasised: “Our R&D engine continues to deliver world-class content, reflected in another strong quarter for gaming operations and record iGaming performance.”

Also Read: Ticketmaster Joins Forces with Monumental Sports to Build America’s Most Advanced Arena Experience

Market Context and Competitive Landscape

Light & Wonder operates in an increasingly competitive environment. The gaming technology sector continues to evolve rapidly with artificial intelligence, virtual reality, and blockchain technologies reshaping player experiences.

The company showcased its latest innovations at G2E and AGE trade shows during the quarter, reinforcing its commitment to cross-platform strategy and robust content development.

Over the past five years, Light & Wonder has grown sales at a 4.7% compounded annual growth rate. The company’s annualised revenue growth of 7% over the last two years exceeds its five-year trend, suggesting accelerating momentum.

Wall Street analysts maintain generally positive outlooks for the stock, with 13 analysts offering a consensus price target of $186.89, implying significant upside from current levels.