The global mining landscape is undergoing a significant transformation, with gold and copper mining in 2025 emerging as a central theme driving investment flows and strategic decisions across major stock exchanges. Mining companies listed on the ASX, NYSE, and TSXV are implementing diverse strategies to capitalise on unprecedented demand patterns that reflect both traditional safe-haven investing and the modern energy transition.

Gold prices have surged 26% in the first half of 2025, reaching multiple record highs above USD 3,400 per ounce, while copper maintains strength around USD 9,700 per tonne despite periodic volatility. These price levels are creating distinct opportunities for miners across different market segments and geographical regions.

Global Market Dynamics Reshaping Mining Strategies

The convergence of multiple macroeconomic factors is driving exceptional demand for both metals. Central bank gold purchases reached 244 tonnes in Q1 2025, maintaining momentum from record-setting buying in previous years. This institutional demand reflects growing concerns about currency stability and geopolitical uncertainty.

Meanwhile, copper consumption is being revolutionised by the energy transition. Electric vehicle production requiring 80-100 kg of copper per vehicle compared to just 23 kg for traditional cars is creating structural demand that mining companies must address through expanded production capacity.

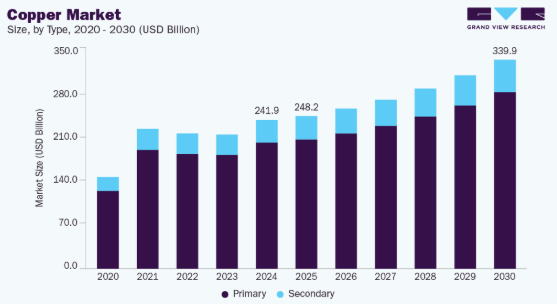

The global copper market is projected to reach USD 339.95 billion by 2030, growing at a CAGR of 6.5% from 2025. This growth trajectory is underpinned by infrastructure modernisation programs and renewable energy installations requiring substantial copper inputs for electrical systems.

Global copper market projection

Safe-Haven Strategies Meet Infrastructure Buildouts

Gold’s role as a hedge against inflation and uncertainty has intensified in 2025. Goldman Sachs forecasts gold reaching USD 3,700 per ounce by year-end, citing continued geopolitical tensions and central bank diversification away from dollar-denominated reserves.

This safe-haven demand coincides with copper’s critical importance in global infrastructure buildouts. The International Energy Agency projects that copper demand from electrification and renewable energy applications will grow at a compound annual growth rate of 10.7%, including 14.3% growth in the EV sector and 5.6% in solar power applications.

These complementary demand drivers are creating opportunities for mining companies to develop strategies that address both defensive and growth-oriented investor requirements.

How ASX Gold Miners Are Capitalising on Record Prices

ASX gold miners are experiencing a renaissance despite historically undervalued share prices relative to gold’s performance. The S&P/ASX All Ordinaries Gold Index surged 12.91% in late July, highlighting renewed investor interest in Australian gold producers.

Strategic Responses from Major Producers

Newmont Corporation (ASX: NEM) continues to dominate with a market capitalisation of $94.2 billion and production targets of 6.8 million ounces annually. The company’s Tier 1 asset strategy, focused on operations with mine lives exceeding 10 years in politically stable jurisdictions, positions it well for sustained high gold prices.

Northern Star Resources (ASX: NST) has expanded its operations across Western Australia and Alaska, maintaining all-in sustaining costs of $1,853 per ounce while benefiting from operational leverage to rising gold prices.

Evolution Mining (ASX: EVN) has positioned itself as a mid-tier producer capable of delivering consistent returns through disciplined capital allocation and strategic acquisitions. The company’s recent performance demonstrates how focused gold producers can outperform diversified miners during precious metals rallies.

Exploration and Development Trends

Australian gold exploration companies are benefiting from renewed investor interest. Our coverage of ASX mining performance highlights how exploration success stories are driving share price appreciation as investors seek leverage to gold price movements.

Companies like Genesis Minerals, which increased its total ore reserves to 3.7 million ounces in April 2025, exemplify how successful resource expansion is being rewarded by the market.

NYSE Copper Companies Scale Production for Energy Transition

NYSE copper companies are implementing capital-intensive strategies to meet surging demand from electric vehicles and renewable energy infrastructure. The scale of investment required reflects the structural nature of copper demand growth and the challenges of bringing new production online.

Major Producer Expansion Strategies

Freeport-McMoRan Inc. (NYSE: FCX) reported copper sales of 1,016 million pounds in Q2 2025, exceeding guidance as the company benefits from premium pricing in domestic markets. The company controls 43% of U.S. domestic copper reserves, positioning it strategically as governments prioritise supply chain security.

BHP Group’s copper division continues expanding production through operational improvements and strategic acquisitions. The company’s acquisition of OZ Minerals for $9.6 billion demonstrates the premium valuations being placed on copper assets with long-term production profiles.

Southern Copper Corporation (NYSE: SCCO) has maintained its position as one of the world’s lowest-cost copper producers while investing in expansion projects across Mexico and Peru. The company’s integrated approach, controlling mining through refining, provides operational flexibility during periods of strong demand.

Technology and Sustainability Initiatives

NYSE-listed copper companies are investing heavily in sustainable mining practices and technological improvements. Advanced processing techniques achieving 85% recovery rates through innovations like bioleaching are becoming industry standards.

Water stewardship and carbon reduction initiatives are particularly important for companies operating in Chile and Peru, where environmental regulations are becoming more stringent. These investments in sustainability infrastructure are viewed as necessary for securing long-term operating licences.

TSXV Exploration Trends Focus on High-Grade Discoveries

TSXV exploration trends reflect a renewed focus on high-grade copper and gold discoveries as junior mining companies benefit from improved access to capital. The TSX Venture Exchange hosts 905 mining companies among 1,572 total listings, representing the world’s most important venue for early-stage mining finance.

Canadian Gold and Critical Minerals Strategy

The Canadian Securities Exchange and TSXV are balancing safe-haven gold demand with critical mineral supply chains. This dual focus reflects Canada’s strategic positioning as both a traditional gold producer and a supplier of minerals essential for the energy transition.

Companies like Tudor Gold, Thesis Gold, and Spanish Mountain Gold have maintained exploration momentum despite commodity price volatility. These companies represent the exchange’s commitment to advancing Canadian gold resources through systematic exploration programs.

Copper and Nickel Junior Success Stories

Power Nickel (TSXV: PNPN) dominated the TSX Venture 50 rankings with a 630% share price increase, demonstrating how successful exploration results can create exceptional shareholder returns in junior mining markets.

The company’s Nisk Project in Quebec has delivered outstanding results across multiple mineralised zones, with recent acquisitions expanding the land package to enhance scale and development potential.

Canada Nickel Company (TSXV: CNC) has strategically consolidated the Timmins Nickel District, positioning it as potentially the world’s largest nickel sulphide district based on Wood Mackenzie metrics.

Capital Markets and Partnership Trends

TSXV exploration companies are pursuing strategic partnerships with major producers to advance projects through development stages. These partnerships provide technical expertise and financial backing while allowing juniors to retain upside exposure to exploration success.

Exploration budgets on the TSXV reached USD 3.2 billion in 2024, the highest level since 2013, with particular focus on Latin America and Canada for copper-gold systems.

EV Demand Transforms Copper Consumption Patterns

EV demand is fundamentally altering copper consumption patterns and creating new investment themes across all major exchanges. Electric vehicle production is projected to exceed 20 million units globally by 2025, compared to 3.2 million in 2020, according to International Energy Agency projections.

Infrastructure Requirements and Charging Networks

The development of EV charging infrastructure represents a significant additional source of copper demand beyond vehicle production itself. Each charging station requires substantial copper inputs for power distribution systems, with rapid charging installations being particularly copper-intensive.

Goldman Sachs estimates rising EV usage will power higher copper demand as the transportation sector’s share of total copper consumption increases from 11% in 2021 to over 20% by 2040.

Battery Technology Evolution

Advances in battery technology are creating both opportunities and challenges for copper demand. Solid-state battery developments could require significantly more copper per vehicle than current lithium-ion systems, while improvements in charging efficiency may reduce infrastructure requirements.

Mining companies are monitoring these technological developments closely to ensure production planning aligns with evolving demand patterns.

Also Read: AI and Big Tech on NYSE and LSE: The Next Wave of Global Business Transformation

Supply Chain Challenges and Market Opportunities

Supply chain security has become a strategic priority for mining companies across all exchanges. China’s control over 80% of critical mineral processing in the Democratic Republic of Congo and dominance in graphite and lithium processing creates supply concentration risks that mining companies are addressing through geographic diversification.

Processing and Refining Capacity

The development of processing and refining capacity outside China has become a key investment theme. Companies with integrated operations controlling both mining and processing are commanding premium valuations as investors recognise the strategic value of supply chain control.

Recycled copper represents 32% of total supply, creating opportunities for companies investing in secondary recovery technologies. This circular economy approach helps address supply constraints while reducing environmental impact.

Geographic Diversification Strategies

Mining companies are prioritising projects in politically stable jurisdictions with established mining codes and infrastructure. This preference for Tier 1 jurisdictions is reflected in higher valuations for assets in Australia, Canada, and Chile compared to projects in higher-risk regions.

Infrastructure access and renewable power availability are becoming increasingly important selection criteria for project development decisions.

Investment Outlook and Strategic Positioning

The investment outlook for gold and copper mining 2025 remains constructive despite periodic volatility. Multiple factors support continued strength in both commodities, though the specific drivers differ significantly between metals.

Gold Market Fundamentals

J.P. Morgan Research forecasts gold averaging USD 3,675 per ounce in Q4 2025, climbing toward USD 4,000 by mid-2026. This outlook reflects continued central bank buying, geopolitical uncertainty, and gold ETF inflows as interest rates decline.

Gold’s performance as an inflation hedge and currency alternative positions it well for an environment of fiscal expansion and monetary accommodation in major economies.

Copper Supply-Demand Dynamics

Copper faces a structural supply deficit estimated at 200,000-300,000 metric tons annually through 2027. This deficit reflects the combination of surging demand from electrification and the challenges of bringing new mine production online.

The 17-year average timeframe from discovery to production for new copper mines means that current high prices may not result in meaningful supply responses until the early 2030s.

Exchange-Specific Opportunities

Each major exchange offers distinct advantages for mining sector exposure:

ASX advantages:

- Proximity to Asian markets and infrastructure

- Established mining code and regulatory framework

- Strong performance in critical minerals exploration

NYSE benefits:

- Access to institutional capital and global investors

- Established producer track records and operational scale

- Dividend-paying capabilities for income-focused investors

TSXV opportunities:

- Exploration leverage and early-stage discovery potential

- Government support for critical minerals development

- Strategic location for North American supply chains

Technology and Innovation Driving Efficiency

Mining companies across all exchanges are investing in technology and innovation to improve operational efficiency and reduce production costs. Artificial intelligence applications in mineral processing are achieving recovery rates up to 85%, while automated mining systems are reducing labour costs and improving safety outcomes.

Digital Mining Technologies

Advanced analytics and machine learning applications are transforming mineral exploration and mine operations. Companies using these technologies are achieving faster discovery timelines and more accurate resource estimation, providing competitive advantages in project development.

Remote sensing and satellite imagery analysis are enabling more targeted exploration programs, reducing costs and environmental impact while improving success rates.

Environmental and Social Governance

ESG considerations are becoming increasingly important for mining company valuations and access to capital. Companies demonstrating strong environmental stewardship and community engagement are accessing capital at lower costs and securing better project approval timelines.

Water management and carbon reduction initiatives are becoming standard requirements for new mining projects, particularly in water-stressed regions where copper mines are typically located.

Regional Market Analysis and Growth Projections

Regional market dynamics vary significantly across major mining jurisdictions, creating different opportunities and challenges for companies operating in each area.

Asia-Pacific Dominance

Asia Pacific accounts for 74.7% of global copper market share, with China and India driving infrastructure development and renewable energy initiatives. This regional concentration creates both opportunities and risks for mining companies serving these markets.

Australian mining companies benefit from proximity to these high-growth markets while operating under stable regulatory frameworks that protect investor interests.

North American Market Integration

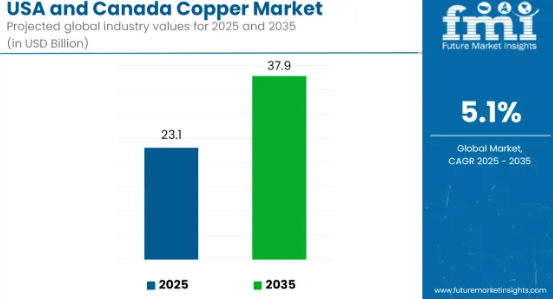

The USA copper market is expected to grow at 5.1% CAGR between 2025 and 2035, driven by infrastructure investment and domestic manufacturing initiatives. Trade policy changes are creating premiums for domestically produced copper, benefiting North American miners.

Canadian companies are particularly well-positioned to serve integrated North American supply chains while maintaining access to both domestic and export markets.

USA copper market is expected to grow at 5.1% CAGR

European Energy Transition

The European Union’s Green Deal is accelerating investments in wind and solar energy projects, creating substantial copper demand for electrical infrastructure. European mining companies and those serving European markets are benefiting from policy support for renewable energy deployment.

Market Risk Factors and Mitigation Strategies

Despite positive fundamentals, mining companies face several risk factors that could impact performance in 2025 and beyond.

Economic and Policy Risks

Global economic slowdown could reduce industrial copper demand, though infrastructure spending programs provide some downside protection. Trade policy changes and tariff adjustments create both opportunities and risks for companies serving international markets.

Interest rate policies affect both gold and copper markets, though through different mechanisms. Rising rates typically pressure gold prices while potentially reducing infrastructure investment that drives copper demand.

Operational and Technical Risks

Mining operations face ongoing challenges from declining ore grades, deeper deposits, and more stringent environmental regulations. Companies investing in technology and operational efficiency are better positioned to manage these challenges.

Geopolitical risks in major producing regions create supply disruption potential that could benefit companies operating in stable jurisdictions, though at the cost of higher operational expenses.

Future Outlook and Strategic Recommendations

The outlook for gold and copper mining 2025 remains positive despite periodic volatility and operational challenges. Companies that can successfully balance growth investment with operational discipline are likely to outperform in the current environment.

Successful mining companies are focusing on several key strategic initiatives:

Asset Quality Enhancement: Prioritising high-grade, long-life assets in politically stable jurisdictions while divesting marginal properties.

Technology Integration: Implementing advanced mining technologies to improve productivity and reduce environmental impact.

Financial Discipline: Maintaining strong balance sheets while investing in growth opportunities as they arise.

ESG Leadership: Demonstrating environmental and social responsibility to ensure continued access to capital and operating licences.

Also Read: Australia’s Inflation Surge: Implications for ASX Blue-Chip Companies and Global Investors

Investment Timing Considerations

Current market conditions present opportunities for both production exposure and exploration leverage. Established producers offer dividend yields and operational cash flows, while junior explorers provide leverage to commodity price appreciation and discovery potential.

Investors should consider portfolio diversification across different exchanges and company stages to capture various aspects of the gold and copper investment theme while managing risk exposure.

Frequently Asked Questions

Q: Which exchange offers the best exposure to gold and copper mining in 2025?

A: Each exchange offers distinct advantages – ASX for proximity to Asian markets, NYSE for established producers with dividends, and TSXV for exploration leverage and discovery potential.

Q: How much copper does an electric vehicle actually require?

A: Electric vehicles require 80-100 kg of copper compared to 23 kg for traditional internal combustion engine vehicles, creating significant incremental demand as EV adoption accelerates.

Q: Why are central banks buying so much gold in 2025?

A: Central banks purchased 244 tonnes in Q1 2025, continuing a trend of reserve diversification amid geopolitical uncertainty and concerns about currency stability.

Q: What’s driving copper prices higher despite economic uncertainty?

A: Structural supply deficits of 200,000-300,000 tonnes annually combined with growing demand from electrification and infrastructure projects support copper prices.

Q: Are gold mining stocks undervalued relative to gold prices?

A: Yes, many analysts believe gold mining stocks remain undervalued despite gold reaching record highs, creating opportunities for investors seeking leverage to gold price appreciation.

Q: How long does it take to develop a new copper mine?

A: The average timeframe from discovery to production is 17 years for copper mines, meaning current high prices won’t result in significant new supply until the early 2030s.

Q: What role does recycling play in copper supply?

A: Recycled copper represents 32% of total supply and is growing in importance as companies invest in secondary recovery technologies to address supply constraints.

Q: Which countries are most important for copper production?

A: Chile, Peru, China, and the Democratic Republic of Congo are the largest copper producers, with supply concentration creating both opportunities and risks for mining investors.