DroneShield Limited (ASX: DRO) shares suffered their steepest single-day plunge in over a year after revelations that Chief Executive Officer Oleg Vornik sold his complete holding in the counter-drone technology company.

The stock dropped as much as 31% to $2.45 on 13 November 2025, marking the worst performance since July 2024. Trading volumes surged in early sessions as investors reacted to news that Vornik had disposed of 14.8 million shares worth $49.5 million between 6 November and 12 November.

The selloff sent shockwaves through the ASX defence sector. DroneShield now trades more than 60% below its October peak of $6.60.

Three Directors Exit for $67 Million

Vornik wasn’t alone in heading for the exit. Chairman Peter James sold 3.7 million shares for $12.4 million, while director Jethro Marks offloaded 1.5 million shares for $4.9 million over the same period.

Oleg Vornik, CEO at DRONESHIELD

Oleg Vornik, CEO at DRONESHIELD

The combined insider selling totalled approximately A$67 million. All three executives converted vested performance options to fully paid ordinary shares on 5 November before selling into the market.

Those options vested after DroneShield achieved a performance hurdle of $200 million in cash receipts over a rolling 12-month period. The milestone was announced on 4 November when 44.5 million performance options converted.

PAC Partners institutional equity sales analyst James Nicolaou didn’t mince words. “That’s about $50 million worth of conviction heading straight for the exit,” he said in a statement.

“What do they still own? Just performance shares and a few options. The CEO’s remaining 900k options are described as ‘significant’, which is generous, bordering on comedy.”

Perfect Storm of Bad Timing

The massive insider selling came just days after an embarrassing administrative bungle. On 10 November, DroneShield incorrectly announced it had secured three new contracts worth $7.6 million with the US Government.

Hours later, the company withdrew the announcement. The contracts weren’t new business at all. They were orders previously issued earlier in 2025 that the customer had reissued due to regulatory updates.

The stock briefly jumped 8.5% on the incorrect news before retreating when the announcement was pulled. Investors who bought on that spike got burned twice in quick succession.

“The November contracts were inadvertently marked as new contracts rather than revised contracts due to an administrative error,” DroneShield noted in its retraction statement. “DroneShield is taking steps to prevent this error from reoccurring.”

The timing couldn’t have been worse. The share price was already under pressure. The withdrawn announcement eroded confidence. Then came news of the insider exodus.

From Meme Stock Hero to Falling Knife

Droneshield shares have delivered a rollercoaster ride in 2025. The stock surged more than 500% through most of the year, making it the best performer among global defence stocks tracked by major indices.

Retail traders embraced the company alongside traditional defence investors betting on counter-drone demand. The meme stock frenzy coincided with genuine business momentum.

DroneShield reported quarterly revenue jumped 1,091% in Q3 to $92.9 million. Year-to-date committed revenues reached A$193.1 million. The company secured major defence contracts including $7.9 million from the US Department of Defense in September and a A$62 million delivery to a European military customer in June.

Despite the selloff, Droneshield shares remain up 226.7% year-to-date. But recent buyers are nursing severe losses. Anyone who purchased near the October peak is down 60%.

The share price now sits below its 200-day moving average, a technical indicator watched closely by traders.

What CEO Vornik Left on the Table

Vornik still holds 193,167 vested performance options and 709,361 unvested performance options. He previously sold his entire shareholding in early 2024, just as the stock hit record highs amid the escalating Ukraine war.

That sale came before retail traders sent the company’s valuation into orbit. Vornik missed out on paper gains that would have exceeded $150 million if he’d held until the October 2025 peak.

Asked about that decision earlier this year, Vornik told media: “I said last year when we became a meme stock that the share price level didn’t bother me.”

The latest selling spree suggests the CEO remains focused on converting performance-based compensation into cash rather than betting on further share price appreciation.

Vornik founded DroneShield in 2014 and has spent nearly a decade building the company into a leading counter-drone technology provider. His willingness to repeatedly sell significant stakes raises questions about his long-term confidence in valuation levels.

Business Fundamentals Remain Strong

Stepping back from the share price carnage, DroneShield’s operational performance tells a different story. The company is winning repeat contracts from customers including the US Department of Defense, European militaries, and Australian law enforcement.

In 2025, DroneShield secured 78 purchase orders with a median value of around $400,000. That compares favourably to 66 orders last year with a median value of $200,000.

The doubling of average deal size, combined with an 18% increase in total orders, points to commercial traction. Customers are stepping up from small evaluation purchases to full-scale procurement.

DroneShield is expanding production capacity to meet demand. The comp $2.4 billion worth of systems by the end of 2026.

Cash receipts hit an all-time high of $77.4 million in Q3. Operating cashflow turned positive at $20.1 million. A year ago, the company was burning $19.4 million per quarter.

The company’s technology has proven effective in Ukraine, where Australia provided $10.4 million worth of DroneShield equipment through government aid packages in 2023.

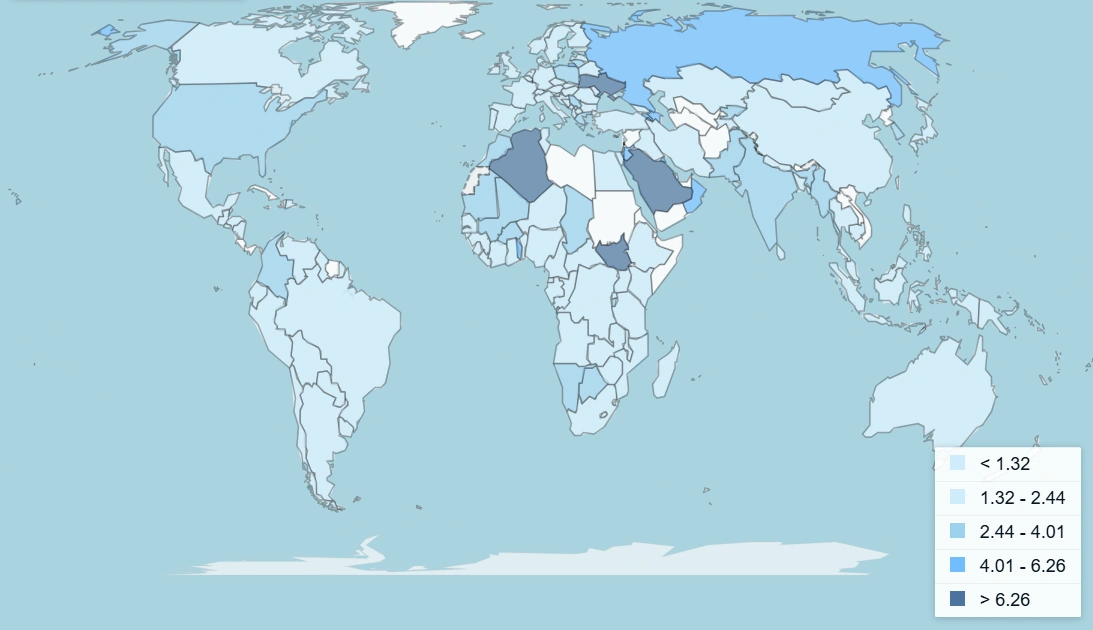

Counter-Drone Market Booms Amid Global Conflicts

Global defence spending continues climbing. The counter-drone market is forecast to reach US$7.05 billion by 2029, expanding at a 26.7% compound annual growth rate from US$2.16 billion in 2024.

Global Military expenditure (% of GDP)

Rising drone threats in Ukraine, the Middle East, and along contested borders have accelerated procurement. Military forces and civilian infrastructure operators are racing to deploy detection and neutralisation systems.

DroneShield offers portable, AI-powered solutions that deploy faster and cost less than traditional integrated systems from major defence contractors. The company’s modular approach has won favour with customers seeking rapid deployment.

Products like the DroneGun Tactical rifle-shaped disruptor and DroneSentry autonomous detection system have become staples in conflict zones and sensitive installations worldwide.

The company entered the S&P/ASX 200 Index during the September rebalance, bringing automatic inflows from index funds and increased institutional coverage.

Investor Reactions Split

Market reactions to the insider selling have been divided. Some investors see the exodus as a red flag signalling overvaluation. Others view it as a chance to buy the dip on a company with strong fundamentals.

“For a high-flying ASX stock like DroneShield, it’s normal for there to be volatility,” one market commentator noted. “But a fall of around 30% is very painful.”

The question facing investors is whether the underlying business has changed or whether the selloff simply forced short-term holders out. Insider sales can be driven by many personal factors including liquidity needs, tax planning, or portfolio diversification.

The market rarely waits to understand the motive. It reacts first and rationalises later.

What matters for long-term investors is whether fundamentals remain intact. DroneShield’s contracts, demand profile, and strategic momentum appear unchanged despite the short-term volatility.

Market Data

As of midday on 13 November 2025, Droneshield shares traded at $2.185, down 33% on the day.

Key metrics:

- 52-week range: $0.585 – $6.705

- Market capitalisation: Approximately $2.97 billion (as of close 12 November)

- Volume: 905 million shares (13 November), highest daily volume in recent trading

The stock closed at a peak of A$6.60 on 9 October before beginning its steep descent.

Also Read: Far East Gold Intersects Bonanza-Grade Gold and Visible Gold at Sua Prospect

What Happens Next

DroneShield faces a credibility test. The administrative error with the withdrawn announcement exposed weaknesses in internal controls. The insider selling has shaken investor confidence.

CEO Vornik and the board will need to restore trust through consistent operational performance and transparent communication. The company has committed to implementing measures to prevent similar mistakes in future announcements.

From a fundamental perspective, DroneShield remains well-positioned. Defence budgets are rising globally. Counter-drone technology demand is accelerating. The company has proven products, growing revenues, and positive cashflow.

Whether the share price has found a bottom remains uncertain. Technical indicators suggest further downside is possible until a new pivot point emerges. The stock is oversold on some measures, which typically precedes a bounce.

For investors, the combination of a 60% drawdown from recent highs and strong operational momentum creates a difficult valuation puzzle. Is DroneShield a bargain after the selloff or does the insider exodus signal more pain ahead?

The answer may depend on your investment timeframe. Short-term traders face continued volatility. Long-term investors betting on the structural growth of counter-drone technology may view current levels as an entry opportunity.

One thing is certain: DroneShield’s dramatic ascent and equally dramatic correction have provided a masterclass in the risks and rewards of momentum stocks in the defence sector.