April has brought fresh broker conviction to two names on the ASX. Bell Potter and Morgans have both issued buy ratings on stocks they believe carry meaningful upside from current levels.

Figure 1: ASX market screen showing stock price movements and volatility [Courtesy: Market Index]

The recommendations span retail and alternative asset management. Both analysts see near-term risks, but believe the underlying fundamentals remain intact and compelling for investors willing to look past the noise.

1. Harvey Norman Earns a Buy as Bell Potter Spots Value After the Sell-Off

Harvey Norman Holdings Limited (ASX: HVN) is among the best ASX growth stocks flagged by analysts this month. Bell Potter has retained its buy rating despite acknowledging the headwinds facing the broader retail sector.

![]()

Figure 2: Harvey Norman Holdings Limited logo [Courtesy: Website Files]

Geographic Spread and Property Assets Are the Core Argument

Bell Potter believes Harvey Norman’s exposure to multiple product categories presents risks in the current environment. However, the broker argues that geographic diversification and a substantial property portfolio help offset those concerns considerably.

The broker pointed to Harvey Norman’s international store expansion across the United Kingdom, Malaysia, and Croatia as a driver of new store-led growth. It also highlighted the ongoing refit programme in Australia and the Company’s position as the single largest owner of large format retail property in Australia, with a global portfolio valued at approximately A$4.6 billion.

Valuation Has Become Attractive After a Sharp Decline

Bell Potter noted that Harvey Norman shares have fallen sharply since October 2025. The broker believes this sell-off has created an attractive entry point for investors tracking top ASX dividend shares and growth opportunities alike.

Bell Potter has set a price target of A$6.70 per share on Harvey Norman and rates the stock a buy. The broker stated:

“While our preference skews to category specialists with balance sheet strength, we see HVN’s well balanced geographical diversification somewhat offsetting the multi-category risks. Following the sharp sell-off in the name since Oct-25, HVN’s 1-year forward P/E of ~13x appears attractive considering the new store driven growth in international retailing, refit program in Australia and opportunities to grow their real estate portfolio.”

2. Navigator Global Investments Earns a Buy on Georgian Acquisition

Navigator Global Investments Limited (ASX: NGI) is the second of the ASX buy-rated shares to attract broker attention in April. Morgans has retained its buy rating on the Company following its recent acquisition of Georgian, a Toronto-based AI-focused growth equity firm.

![]()

Figure 3: Navigator Global Investments Limited logo [Courtesy: Wikimedia Commons]

Georgian Acquisition Aligns With Key Investment Trends

Morgans believes the Georgian deal is a strong strategic fit for Navigator Global Investments. The broker sees the acquisition as earnings accretive and aligned with the Company’s flagged acquisition criteria.

Morgans has forecast that Navigator Global Investments’ earnings per share for FY26, FY27, and FY28 will increase by approximately one to three per cent following the Georgian transaction. The broker views the deal as supportive of the Company’s long-term growth outlook among the best ASX growth stocks in the alternative asset management space.

Target Price Trimmed but Fundamentals Remain Solid

Morgans has reduced its price target on Navigator Global Investments to A$2.98 per share, down from A$3.35 previously. The broker attributed this reduction to a contraction in global peer trading multiples and a more conservative valuation multiple of 12.5 times price-to-earnings, compared to 15 times previously.

Despite the target trim, Morgans does not believe the Company’s core fundamentals have deteriorated. The broker noted that current market volatility may actually be supportive of Navigator Global Investments’ stable of alternative asset fund managers. Morgans stated:

“NGI’s recent sell-off appears to be mainly tied to Private Credit concerns around its key strategic partner Blue Owl. We think NGI’s fundamentals are largely unchanged, and current market volatility is arguably conducive to its stable of alternative asset fund managers. We rate NGI a Buy.”

Share Price Snapshot

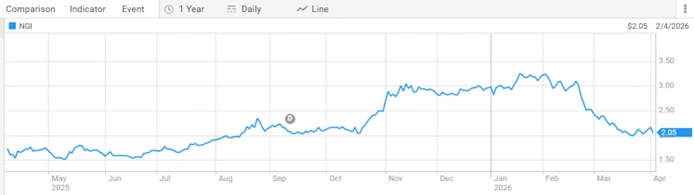

Navigator Global Investments Limited (ASX: NGI) is currently trading at A$2.050 per share, with a market capitalisation of A$1.06 billion and a 52-week range of A$1.450 to A$3.340.

Figure 4: Navigator Global Investments Limited (ASX: NGI) share price performance over the past year [Courtesy: ASX]

Harvey Norman Holdings Limited (ASX: HVN) is trading at A$4.730 per share, with a market capitalisation of A$6.06 billion and a 52-week range of A$4.530 to A$7.700.

Figure 5: Harvey Norman Holdings Limited (ASX: HVN) share price performance over the past year [Courtesy: ASX]

Industry Outlook

The Australian retail and alternative asset management sectors are both navigating a period of meaningful transition. Consumer spending patterns remain mixed, while institutional capital continues to seek diversified, non-correlated asset exposures.

Among the top ASX dividend shares and growth names, brokers are increasingly favouring companies with geographic scale, strong balance sheets, and exposure to structural themes such as artificial intelligence and critical minerals. The ASX buy-rated shares flagged this month reflect that broader pivot toward quality and resilience in uncertain market conditions.

Future Direction and Impact on ASX Investors

For investors tracking the best ASX growth stocks, the two names flagged by Bell Potter and Morgans this April represent different but complementary investment propositions.

Harvey Norman’s appeal rests on valuation recovery, international store rollout, and the enduring strength of its real estate assets. Navigator Global Investments’ appeal is tied to its expanding alternative asset management platform, the strategic value of the Georgian acquisition, and its ability to generate stable earnings through volatile market cycles.

Both stocks carry risks that brokers have acknowledged openly. For Harvey Norman, multi-category retail exposure remains a concern in a softening consumer environment. For Navigator Global Investments, sentiment around Private Credit and its relationship with Blue Owl continues to weigh on the share price despite the broker’s confidence in underlying fundamentals.

Investors watching top ASX dividend shares and ASX buy-rated shares should monitor both names closely as earnings updates and macro conditions evolve through the remainder of the financial year.

ALSO READ: St Barbara Seals A$389 Million Lingbao Deal

Frequently Asked Questions

Q1. What are the best ASX growth stocks flagged by analysts in April 2026?

Ans. Bell Potter has flagged Harvey Norman (ASX: HVN) and Morgans has flagged Navigator Global Investments (ASX: NGI) as buy-rated shares this April.

Q2. Why is Harvey Norman rated a buy by Bell Potter?

Ans. Bell Potter sees value after a sharp share price decline, citing international store growth, the Australian refit programme, and a large property portfolio as key supports.

Q3. What is Bell Potter’s price target for Harvey Norman?

Ans. Bell Potter has set a price target of A$6.70 per share on Harvey Norman.

Q4. Why has Morgans trimmed its price target on Navigator Global Investments?

Ans. Morgans reduced the target to A$2.98 per share due to a contraction in global peer trading multiples and a more conservative valuation multiple applied to the stock.

Q5. What is the Georgian acquisition and why does it matter?

Ans. Georgian is a Toronto-based AI-focused growth equity firm acquired by Navigator Global Investments. Morgans views it as earnings accretive and strategically aligned with key investment trends.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on broker research and analyst commentary available as of 3 Apr 2026 and sourced from publicly available reporting. Share price data should be verified independently via the ASX website at the time of reading. Investing in securities involves risk, including the possible loss of principal. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.

Sources

https://www.fool.com.au/2026/04/03/why-these-asx-shares-are-rated-as-buys-in-april

https://www.asx.com.au/markets/company/HVN

https://www.asx.com.au/markets/company/NGI

Last modified: April 3, 2026