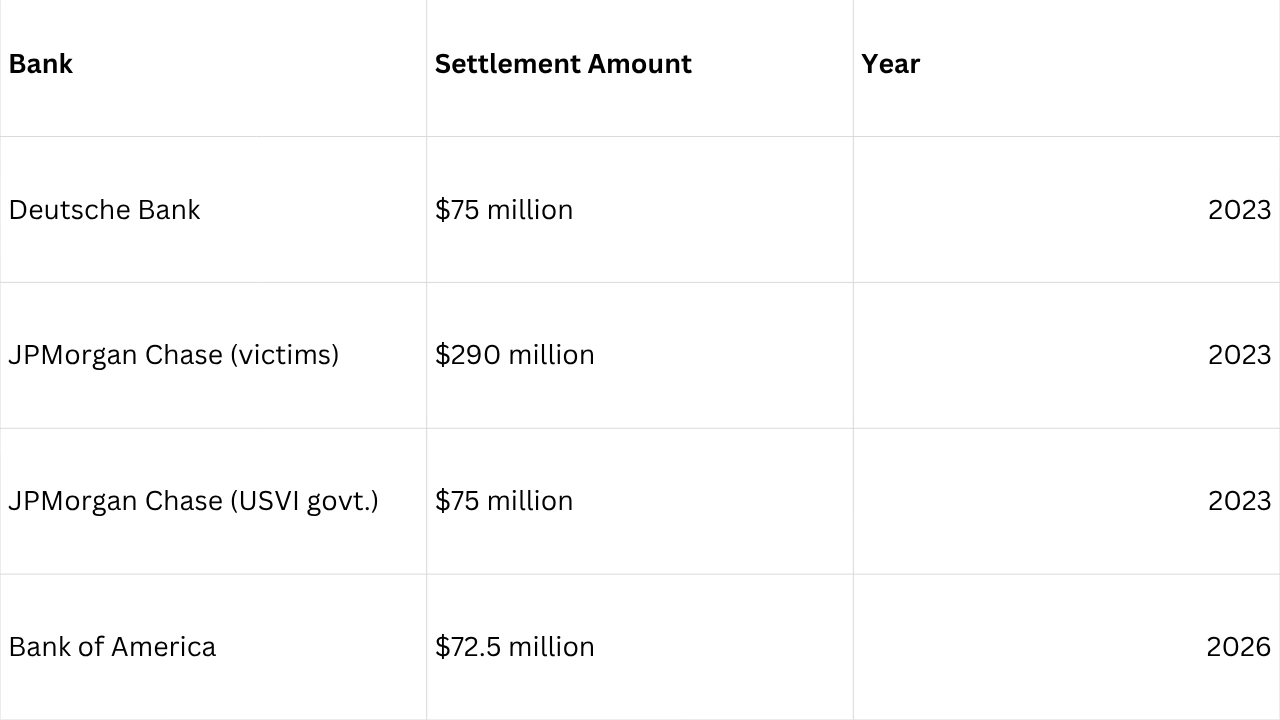

Bank of America has agreed to pay $72.5 million to settle a federal class-action lawsuit filed by women who accused the bank of facilitating Jeffrey Epstein’s sex-trafficking operation. Court records confirmed the deal on 27 March 2026, marking yet another significant moment in the long legal reckoning over who enabled Epstein’s crimes.

The Bank of America Epstein settlement still requires approval from US District Judge Jed Rakoff in Manhattan, who has scheduled a hearing for 2 April. The bank issued a statement saying the resolution “allows us to put this matter behind us and provides further closure for the plaintiffs,” while maintaining it did not facilitate sex-trafficking crimes.

This is not an admission of guilt. But for survivors, it is something else entirely — a financial acknowledgement that a powerful institution looked the other way.

The Women Behind the Case

The lawsuit traces back to a Florida woman, referred to in court documents only as Jane Doe. She alleged Epstein abused her “on at least 100 occasions” between 2011 and 2019. Epstein’s business team directed her to open two Bank of America accounts in 2013, which the lawsuit claims the bank then allowed Epstein and his associates to exploit for years.

Importantly, there is no single “Jane Doe” in the Jeffrey Epstein case; rather, the lawsuits involve dozens of women identified by pseudonyms. The most prominent accuser who has identified herself publicly is Virginia Giuffre (formerly Virginia Roberts), often referred to in early court documents as Jane Doe No. 102.

Colitco reported the suicide of Virginia Giuffre in 2025. Read the full news below.

Also Read:The Light That Fought the Shadows: Virginia Giuffre Dies at 41

The proposed class action sought to represent all women trafficked or abused by Epstein and his associates. Lawyers in the case noted at least 60 women fell victim during the period covered by the complaint.

Attorney Sigrid McCawley, who represents the survivors, described the settlement as:

- “One more step on the road to much-deserved justice”

- A vindication for women whose voices drove the entire legal reckoning

- The result of a road that has been “long and trying”

Attorneys David Boies and Bradley Edwards added that the settlement gave their clients the best possible outcome, particularly because “many Class Members suffered harm many years ago and are in need of financial relief now.”

How the Bank Allegedly Looked the Other Way

The $170 Million Problem

At the centre of the Bank of America Epstein settlement sits a staggering financial trail. The lawsuit alleged that billionaire Apollo Global Management co-founder Leon Black transferred $170 million to Epstein from his Bank of America accounts — ostensibly for “tax and estate planning advice.”

The transfers came in massive instalments, often $10 million or $20 million at a time. The lawsuit argued these transactions had “no apparent business or lawful purpose” and represented “the primary means by which the sex-trafficking venture was funded.”

Senate Finance Committee Ranking Member Ron Wyden put it plainly: Bank of America’s employees “repeatedly failed to conduct due diligence and report suspicious transactions to the US Treasury Department, as required by law under the Bank Secrecy Act.”

Red Flags the Bank Allegedly Ignored

The complaint accused the bank of ignoring a “plethora” of warning signs, including:

- Large, irregular wire transfers from Black’s accounts to Epstein

- Accounts held by Epstein victims used at his direction

- Epstein’s well-documented 2008 state-level sex crimes conviction

- Ongoing transactions with no clear legitimate business purpose

Judge Rakoff dismissed some claims in January but allowed the core allegations to proceed — that the bank knowingly benefited from Epstein’s conduct and obstructed enforcement of the federal Trafficking Victims Protection Act.

When the Walls Closed In

A Timeline of Legal Pressure

The lawsuit hit court in October 2025. By March 2026, the Bank of America Epstein settlement had taken shape — driven in part by the mounting pressure of an imminent trial date (11 May) and a scheduled deposition that would have put one of Wall Street’s most powerful figures under oath.

Leon Black, billionaire co-founder of Apollo Global Management, was scheduled to sit for eight hours of closed-door testimony on 26 March. The settlement announcement came just days before that deposition. Black’s lawyer had already persuaded the judge to postpone it once, citing the likelihood of a deal.

Black stepped down as Apollo’s CEO in March 2021 after an internal inquiry found he had paid Epstein $158 million. His attorney has stated Black “had no awareness of Epstein’s criminal activities.”

Which Banks Have Now Paid; and What It Tells Us

Bank of America becomes the third major financial institution to settle Epstein-related claims brought by his victims:

The earlier JPMorgan and Deutsche Bank cases centred on Epstein’s personal banking relationships. The Bank of America Epstein settlement is different — it focused primarily on accounts used by Epstein’s associates, co-conspirators, and victims themselves.

Bank of New York Mellon faced a similar lawsuit, but Judge Rakoff threw it out in January, finding the complaint did not sufficiently allege BNY had actual knowledge of Epstein’s activities.

The pattern across these cases is hard to ignore: major institutions processed unusual, high-value transactions tied to a man with a known conviction for sex crimes — and survivors say those institutions chose profit over protection.

Why the Fallout Goes Beyond the Courtroom

Senate Scrutiny Isn’t Over

Senator Wyden made clear the Bank of America Epstein settlement does not end the political reckoning. His office has been conducting an ongoing investigation into how Wall Street banks enabled Epstein’s crimes, and he stated he would “continue to put out more findings on the matter in the near future.”

Wyden also criticised Attorney General Pam Bondi and Treasury Secretary Scott Bessent for failing to hold Bank of America and other banks accountable at the federal level.

The broader political fallout from the DOJ’s release of 3 million pages of Epstein files has kept the case firmly in the public eye. Those documents showed Epstein had regular contact with CEOs, scientists, journalists, and prominent politicians long after his 2008 conviction.

The Push for Deeper Disclosure

Public pressure for transparency has not let up. Lawmakers have debated the scope of document releases, and the debate over Epstein file disclosures has drawn fierce political divides. Meanwhile, photographs and records linking high-profile figures to Epstein continue to surface, keeping the story relevant far beyond Wall Street boardrooms.

What Comes Next

The 2 April hearing before Judge Rakoff will determine whether the $72.5 million settlement wins court approval. If approved, the Bank of America Epstein settlement would join a growing pool of payouts, alongside the Epstein estate’s own restitution fund, which has reportedly paid out $121 million to victims separately.

For survivors, each settlement represents a measure of financial relief. For Wall Street, each one adds a data point to a damning pattern of institutional failure.

Senator Wyden’s investigation continues. Lawyers for the victims are still appealing the dismissal of their lawsuit against Bank of New York Mellon. And the political scrutiny of Epstein’s financial network shows no sign of cooling.

The money matters. But so does the question no settlement can fully answer: how did it go on for so long?

Sources

- https://www.reuters.com/world/bank-america-agrees-pay-725-million-settle-epstein-accusers-lawsuit-2026-03-27/

- https://www.pbs.org/newshour/nation/bank-of-america-settles-lawsuit-brought-on-behalf-of-jeffrey-epstein-victims

- https://www.cnbc.com/2026/03/27/jeffrey-epstein-bank-of-america-lawsuit-settle.html

- https://abcnews.com/US/bank-america-reaches-proposed-binding-settlement-suit-alleging/story