ASX 200 futures fell 25 points, or 0.28%, following the enforcement of new tariffs in the United States. The move lifted the US’s average effective tariff rate to 15.2%. Bloomberg stated this is the highest US tariff rate in almost a century. Countries with special trade deals such as the EU and Japan faced lower rates, while others like Switzerland saw significant increases.

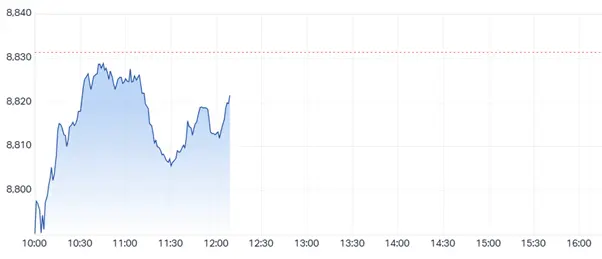

ASX 200 Chart as of 12:09 PM AEST

Sezzle Plunges on Disappointing Guidance Despite Revenue Beat

Sezzle shares dropped 19% in after-hours trading after its Q2 report. Revenue reached $98.7m, 4.0% above consensus. Adjusted EBITDA came in at $37.9m, a 13.8% beat. However, full-year EPS guidance excluding items landed at $3.25, missing consensus by 5.3%. Full-year revenue guidance of 60-65% sat in line with the consensus of 63%. FY adjusted EBITDA guidance of $170.0-175.0m missed slightly, falling 1.9-4.7% below consensus.

Iress Engaged by Blackstone and Thoma Bravo

Iress entered into negotiations with Blackstone for a potential buyout valued around $1.9b. An offer could exceed $10 per share, according to the AFR. Thoma Bravo, another private equity firm, expressed interest, adding competitive pressure to the bidding process. Recent buyouts of Australian-listed software firms included Infomedia ($651m), Nearmap ($1.1b), Altium ($9b), Nitro Software (over $500m), and Bigtincan (undisclosed).

QBE Delivers Above Expectation 1H25 Results but Slides

QBE reported a 1H25 result that beat most estimates. Gross written premium increased 6% to $13.82bn, topping expectations by 0.4%. The combined operating ratio fell to 92.8%, 0.3 percentage points better than estimated. Catastrophe claims ratio stood at 5.4%, resulting in net catastrophe claims of $479m below the allowance of $549m. Adjusted net profit surged 25.7% to $997m, beating consensus by 18.5%. The interim dividend jumped 29% to 31c per share, missing estimates by 2.8%. Guidance for the full year projected mid-single digit growth for gross premiums written and a combined operating ratio of 92.5%. Exit core fixed income yield posted at 3.8%. Despite positive results, shares fell 5.1% to $22.25, citing factors such as a prior strong run, absence of capital management initiatives, and yields at the lower end of expectations.

AMP Posts Mixed 1H25 Results as Analysts Respond

AMP reported a 1H25 underlying NPAT up 9.2% to $131m, but missed consensus by 5.1%. Revenue grew 1.8% to $632m, missing by 0.6%. Asset under management climbed 3.7% to $153.9bn. Shares fell 4.1% at open but rebounded for a 4.7% gain by close. Brokers presented cautious optimism. JPMorgan raised its target to $1.65, highlighting a simplified model and adviser trends but cited margin and litigation risks. Jarden moved its target to $1.60, noting revenue margin recovery remains slow and bank outlook depends on digital product adoption. UBS upped its target to $1.80, seeing strong business execution but flagged capital constraints from ongoing litigation.

Fortescue Secures Pioneering Yuan Loan

Fortescue secured a 14.2b yuan (US$2b) syndicated loan, the first of its kind for an Australian firm. The loan features a 5-year tenor and a fixed 3.8% per annum interest rate. Bank of China’s Sydney branch and Industrial and Commercial Bank of China arranged the deal. Dr Andrew Forrest said, “This isn’t just a financial transaction. It’s a signal of what is possible when partners are aligned in ambition. As the United States steps back from investing in what will be the world’s greatest industry, China and Fortescue are advancing the green technology needed to lead the global green industrial revolution.”

Block Delivers Q2 Results and Positive Outlook

Block held its Q2 results call, signalling strong operating momentum. Q3 gross profit will reach $2.6b with adjusted operating income at $460m and a margin of 18%. The company’s Borrow product now counts 6m monthly users. Cash App’s post-purchase BNPL surpassed 1m users. Square’s sales efforts doubled growth rates since Q4 2025, showing strong customer acquisition economics. Full-year 2025 gross profit is forecast at $10.17b, representing 14% annual growth, with adjusted operating income of $2.03b and a 20% margin. Longer-term, Block expects strong growth from Cash App’s post-purchase BNPL and continued strong sales performance.

GQG Experiences Drop in Funds Under Management

GQG reported funds under management of US$166.6b at 31 July, down 3.3% from the prior month. The company stated, “As an tariffs investment manager for our clients, we remain defensively positioned in our strategies in an effort to reduce risk within client portfolios … As a result of this tariffs positioning, we continued to experience underperformance across all strategies as compared to their respective benchmarks year to date.”

Nick Scali Earnings Dip but Market Reacts Positively

Nick Scali posted a slightly weaker FY25 result. Group revenue rose 5.8% tariffs to $495.3m, falling 2.3% short of tariffs estimates. Gross margin declined 200 basis points to 63.5%, beating Macquarie estimates by 0.5 percentage points. Underlying NPAT fell 24.4% to $62m, 2.2% below estimates. tariffs Statutory NPAT dropped 28.3% to $57.7m. Dividend fell 11.8% to 60c, surpassing estimates by 11.1%. July sales in ANZ increased 7.7% year-on-year. The company tariffs forecast continued losses in its UK business until store refurbishments and sales improvements take hold. Shares traded up 9% to $20.91. UK gross margin improved over the period; for May and June, it reached 58% in Nick Scali stores, while the ANZ gross margin was 65.6% in 2H, lifting from 64.4% in the first half.

RBA Readies August Rate Cut tariffs Amid Cooling Inflation

The Reserve Bank of Australia prepares to cut rates by 25bps to 3.60% at its 12 August meeting. All tariffs polled economists expect the move and most predict another cut in the following quarter. Australian inflation eased to 2.1% last quarter, nearing a four-year low and tariffs sitting within the central bank’s 2-3% target range.