Futures Indicate Strong Start

The S&P/ASX 200 futures rose 27 points or 0.31% on Friday morning, suggesting the index will open at record highs. The movement follows a strong overnight session on Wall Street, which closed early ahead of Independence Day. The S&P 500 gained 0.83%, while the Nasdaq climbed 1.02%, both hitting new record levels.

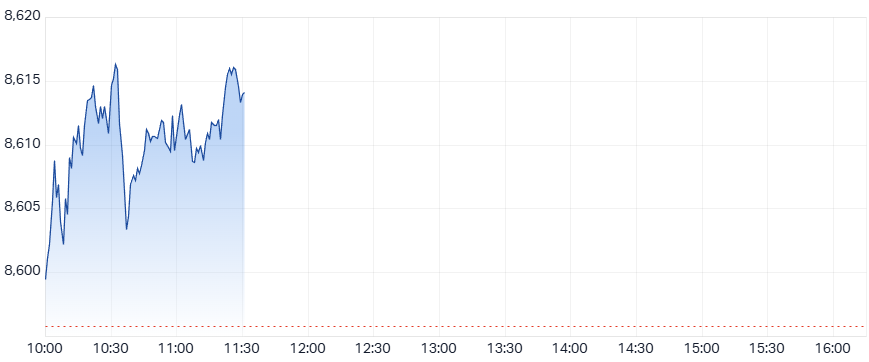

ASX 200 chart as of 11:31 AM AEST

Trump’s Tax Bill and Market Sentiment

US markets digested key policy developments, including the passage of Trump’s “Big, Beautiful Bill.” The legislation extends individual and estate provisions from the 2017 tax cuts and jobs act. The bill now heads to Trump’s desk just in time for the July 4 deadline. Meanwhile, Bessent issued a warning on tariff reintroduction to trading partners. China responded sharply, pledging retaliation if the US-Vietnam deal damages its interests.

Strong US Jobs Data Lifts Yields

US nonfarm payrolls rose by 147,000, well above consensus expectations. The unemployment rate unexpectedly dropped to 4.1% from 4.2%, confounding all 77 Bloomberg-surveyed economists. The decline was driven by people leaving the workforce. Government hiring surged with 73,000 new jobs, led by state and local levels. Federal jobs fell for the fifth consecutive month. However, private payrolls added only 74,000 jobs, marking the weakest result since October’s natural disasters.

Services PMI Disappoints Despite Positive Indicators

The ISM Services Index reached 50.0 in June, missing the 51.0 forecast but improving from May’s 49.9. New orders rebounded, rising to 51.3 from 46.4, indicating returning demand. The Employment Index contracted to 47.2, marking its third drop in four months. Prices remained elevated, slipping to 67.5 but remaining at a high not seen since November 2022. Business activity increased to 54.2, showing some resilience. Respondents highlighted economic uncertainty, affordability issues, and tariffs as business challenges.

Durable Goods and Factory Orders Rebound

May factory orders rose 8.2% month-on-month, aligning with expectations. Durable goods orders increased in five of the past six months. The sector hit its strongest level since July 2014.

Bell Potter Adjusts Ratings and Targets

Bell Potter released several equity updates on Friday morning. Hub24 retained a Buy rating with a target increase to $100 from $75. Jumbo Interactive kept a Hold rating, though its target dropped slightly to $11.00 from $11.10. Lynas Rare Earths remained a Sell with a reduced target of $6.05 from $6.25. Pro Medicus was downgraded to Hold from Buy, though its target rose to $320 from $280, citing valuation concerns.

Citi Hits The Lottery Corp with Double Downgrade

Citi downgraded The Lottery Corp from Buy to Sell and slashed the target to $5.00 from $5.60. FY25 EBIT is expected to drop 13% to $628 million, with results due on 20 August 2025. Powerball sales dropped 9% to June, underperforming the previous estimate of 4%. Oz Lotto saw strength from two $70 million jackpots, potentially diverting interest from Powerball. Planned Powerball changes in FY26 include a 20% price hike, which is forecast to lift turnover by only 10% in FY27.

Citi Cuts Ratings for Wealth Platforms After Rally

Following strong share price performance in 2025, Citi downgraded Hub24 and Netwealth to Neutral from Buy. Hub24 is up 29% this year, trading at 63 times forward earnings. Netwealth rose 19%, with a forward price-to-earnings of 62 times. Citi raised Hub24’s target to $89.80 from $71.50 and Netwealth’s to $33.65 from $27.30, reflecting improved earnings assumptions.

Capricorn Metals Hits FY25 Guidance

Capricorn Metals reported fourth-quarter gold production of 32,216 ounces at its Karlawinda Gold Project. This took FY25 output to 117,076 ounces, near the top of its 100,000–120,000 guidance range. Costs are expected to fall within the AISC range of US$1,370–US$1,470 an ounce.

Monadelphous Wins $100 Million Energy Contracts

Monadelphous Group secured over $100 million in energy sector contracts. The Shell Crux contract involves hook-up and commissioning of the offshore platform northeast of Broome, supporting the Prelude FLNG facility, with completion expected in late 2026. The Inteforge agreement with Origin Energy extends a long-term equipment supply contract for Australia Pacific LNG. The company, valued at $1.7 billion, sees this as an incremental earnings driver.

Pro Medicus Secures Key US Contracts

Pro Medicus announced two new US contract wins. UCHealth became its second largest deal to date, adopting its full imaging stack and the first cardiology module. Franciscan Missionaries of Our Lady Health System renewed its agreement with a more than twofold increase in contract size. The stock closed 7.8% higher at $307.39. Analysts responded favourably. Morgan Stanley maintained an overweight rating and raised its target to $320. Bell Potter also increased its target to $320 but downgraded to Hold, citing delays in FY26 earnings. Goldman Sachs kept its $310 target and Buy rating, highlighting the strategic nature of the UCHealth win.

ACCC Clears Cleanaway Acquisition

The ACCC will not oppose Cleanaway’s $377 million acquisition of Contract Resources Group. “The review found Contract Resources primarily provides specialist industrial services, such as catalyst handling, which Cleanaway does not supply,” the ACCC said. Contract’s FY25 EBITDA is forecast at $52 million. The acquisition is valued at 7.3 times FY25 EBITDA or 4.9 times including synergies. Cleanaway expects the acquisition to be high-single digit EPS accretive and will fund it with debt.

Argosy Minerals Enters Trading Halt

Argosy Minerals was halted on Friday pending a proposed capital raise, effective until Tuesday, 8 July. The move follows a 78.9% share surge on Thursday amid a sector-wide lithium rally.