ASX and NYSE battery metals miners are at the forefront of an accelerating industrial shift. The vehicle sector is going electric. This shift is remapping global supply chains for strategic metals. They are lithium, nickel, and copper.

The Accelerating Shift to Electrification

The automobile industry is changing very fast. Cars with electrification accounted for 43% of global auto sales. This is what occurred in the first quarter of 2025. This is up by a big margin from 9% in 2019. Internal combustion engines have fallen. They now account for 57% of sales. The transformation is changing global supply chains. It is creating enormous demand for battery metals.

The demand for electric vehicles is geographically dependent. China is the leader with 57% of global EV registrations. It contributes to their incentives and leadership in the production of batteries. Europe comes in second with a market share of 22%. The United States has a 12% share. Emerging economies are also showing growth. Southeast Asian sales of electric cars rose by almost 50% in 2024. Brazil doubled its EV sales over the same timeframe. Such trends reflect growing demand for battery metals. They also highlight the strategic importance of a guaranteed supply.

Metals at the Heart of the Energy Transition

Australia’s lithium mines fuel global EV demand

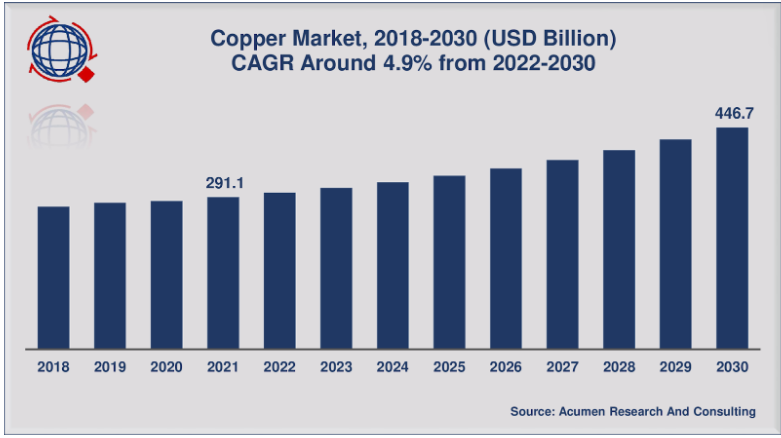

Demand for lithium will quadruple by 2040. Demand for copper is likely to increase by 30% over the next decade. Nickel, cobalt, and rare earths are also of note. They form the basis of battery technologies. Supply issues remain, however. The International Energy Agency sees looming shortages. Copper and lithium supply could fall 30-40% short in the 2030s. It will happen because new mining projects lag behind demand. Trade restrictions and price volatility also hinder material flow. Geopolitical tensions like tariffs cause uncertainty.

Against this backdrop, major mining companies are changing tack. ASX mining giants include BHP and Rio Tinto. NYSE-listed powerhouses are Freeport-McMoRan and Albemarle. They are scaling down their portfolios to meet the growing demand. Their strategies are at the heart of the EV supply chain revolution. They will also determine the investment climate between 2025 and 2030.

BHP’s Strategic Priority on Nickel and Copper

ASX and NYSE battery metal companies are cementing their ground. BHP is a global leader in this field. BHP’s Nickel West business is placed in the EV market. It exports approximately 85% of its nickel output to EV makers. An association with BYD is part of a two-pronged approach. It aims to boost nickel production and become carbon neutral. The West Musgrave Project was acquired from OZ Minerals. The West Musgrave Project will almost double BHP’s premium nickel output. It will secure future supply to EV leaders like Tesla.

Copper makes up a large part of BHP’s portfolio, too. Copper production rose 8% in fiscal 2025. Production was 2.017 million tonnes. The Escondida operation in Chile provided a record 1.305 million tonnes. The company is coping with tightening demand from electrification. It is also facing near-term commodity headwinds. These are softer iron ore prices. There is also nickel volatility in the market. This is due to Indonesian oversupply. Investor interest, however, is attracted to BHP’s long-term growth strategy. It is especially attractive to ESG strategy funds.

Freeport-McMoRan’s Dominance in Copper

Copper remains vital for EVs and global infrastructure

Freeport-McMoRan is a copper supply leader on the NYSE. It estimates 4.2 billion pounds of annual production. Its core assets are its Cerro Verde and Grasberg mines. They fund electrification around the world. The importance of copper can be seen in EVs. An EV uses nearly three times more copper than an ordinary car. Copper is also important for renewable power systems. Such systems use tonnes of copper per installation.

Copper demand growth is outpacing new supply

Freeport-McMoRan is also investing in emerging technology. It is using leaching technology and expansion plans. These are intended for future demand. Policy windfalls in the U.S. also give it an advantage. The imposed U.S. tariffs on imported copper are a case in point. The company’s large size gives it resiliency. This holds even in the presence of commodity cycle risks. It is even true in the presence of geopolitical tensions.

Challenges to European Battery Production

European efforts to create a pool of battery supply have turned sour. Porsche AG, the German automaker, has canceled plans. It is no longer going to be manufacturing high-performance batteries in Cellforce. It said that it had experienced a drop in demand for EVs. It also mentioned changing situations in America and China. The decision will result in 200 jobs being lost. Cellforce will be turned into a research and development facility.

Oliver Blume, CEO of Volkswagen

Oliver Blume, CEO of Volkswagen and Porsche, described the reason. Porsche does not produce its own batteries. It’s due to volume and a lack of economies of scale. The collapse of Swedish electric car battery producer Northvolt has also hurt European prospects. These are developments that show the difficulty of filling the void left by Asia’s supremacy. A Porsche executive, Michael Steiner, explained the reason simply. He stated that it is not possible to produce more. This is because there is a limited world volume.

Hyster’s Electrification Strategy for Forklifts

The industrial sector is also decarbonizing. Replacing diesel and LPG-driven forklifts has been one of them. Electric equivalents are needed for extreme outdoor conditions. Adaptalift Group bought the only Hyster New Zealand Dealer, the exclusive agency rights. This made Adaptalift the region’s exclusive distributor of Hyster. This consolidation makes it simpler to sell and service.

The Hyster XTLG Outdoor Electric range fits this purpose. It attempts to replicate the ability of a standard truck. It does it without the emissions. Mark Chaffey of Hyster explained the design. They employed an internal combustion truck. They transformed it into an electric truck. The new design replaces the engine with a battery and motor. This gives customers IC-like performance. The XTLG range features enhanced traction capability. It features enhanced handling as well. It is built for rugged outdoor operation.

Innovations in Electric Forklift Design

Previous electric trucks were unsuitable for operating outdoors. They were built around massive lead-acid battery boxes. They would wheel spin with ease on loose ground. The XTLG range has a true outdoor-capable design. It fills a gap in the market. Launch of the XTLG series falls under Hyster’s strategy. It encompasses research into hydrogen-powered units. It also includes electrified terminal units. Hyster’s ultimate goal is to provide feasible alternatives. They want to help customers reduce their carbon footprint.

Adam Duncan from Adaptalift Group sees good customer demand. Almost all customers now want to electrify. This range gives them a product that is as capable as an IC truck. It gives customers an option to transition to electric. Most businesses are committing to sustainability programs. They are doing full conversions to electric fleets. The Hyster trucks are designed for flexibility. They have little need for infrastructure. Just a typical three-phase power plug is all they require. The run time is at least five hours per charge.

The Battery Show 2025: Connecting the Supply Chain

Battery Show 2025 is a major event. It is occurring from October 6-9 in Detroit. The event brings together key stakeholders. These stakeholders are part of the battery and EV supply chain. It unites engineers and product developers. It also includes OEM executives and materials scientists. The event involves underlying decisions in energy storage. It also considers manufacturing processes.

EV acceptance is picking up pace. Massive investments are being placed in manufacturing batteries. This event offers direct access to price-sensitive buyers. Visitors are thinking about new suppliers. They are also establishing strategic partnerships. Sales and marketing executives can leverage the attendee list. It helps them identify decision-makers. They can segment contacts. They can even arrange meetings before the event. This gives an edge over the competition.

Market Outlook: Energy Transition and Critical Minerals

Demand for battery metals around the world will increase significantly. It is expected to be four times larger in 15 years. That is according to BloombergNEF. The metal weight in batteries will be greater. It will increase from 12 million tons in 2025 to 53 million tons in 2040. That is for net-zero targets. Copper, lithium, and aluminum will have the greatest share. Passenger EV sales are also expected to rise. BloombergNEF anticipates 22 million global sales in 2025. That is 25% higher than 2024. Sales could be over 39 million by 2030.

China will remain the largest EV market. It will represent nearly two-thirds of overall demand. Europe and the United States will be second. Growth in the U.S. and Europe has decelerated. Emerging markets are converting to EVs at a faster pace. These are Brazil and Thailand. This is making the world’s demand for metals diversified. Bottlenecks in supplies pose a major challenge. My investment rose by 80% in 2024. It was a record $29 billion. Permitting delays and geopolitical tensions can restrain output. Copper has been seen as the most important bottleneck. A supply deficit of 30% by 2030 is likely.

Concentration and Vulnerabilities of Supply Chains

Weaknesses were identified by the International Energy Agency. Refining and processing capacity is highly concentrated. The three largest suppliers provide over 80% of global capacity. China dominates refining for 19 of 20 strategic minerals. It has built two-thirds of global battery recycling capacity since 2020. This type of concentration increases the potential for supply shocks. It is especially concerning with further export restrictions. China’s supremacy in EV manufacturing is a major factor. EVs are more affordable for buyers there than internal combustion vehicles. This boosts demand in the home market. It also facilitates expansion by Chinese automobile makers.

Policy uncertainty in the United States has cooled momentum. BloombergNEF lowered its estimate of U.S. EV sales. The revised 2030 forecast is 4.1 million units. That’s below earlier estimates. Policy shifts and reduced federal incentives have hurt investor confidence. The administration is concentrating on alternative mineral sources. This includes fresh foreign alliances. It also involves suggestions to speed up mine licensing. Europe will most likely remain on a stable trajectory. The UK and Nordic nations lead in adoption there. The continent is reliant on imported key minerals. This creates risks in energy security.

Investor Takeaway for ASX and NYSE Companies

ASX and NYSE battery metal companies are at the core of this shift. Policy and resource depth underpin investor demand. ASX remains a strong hub for mining capital. Industry sources predict 2025 new listings. This is supported by Australia’s A4.1 trillion pension system. That system penetrates capital to domestic equities. This makes ASX an appealing platform. It is a good choice for Australian and overseas miners.BHP ′

Shift from its London listing in 2022 supported the ASX. It injected A96 billion into the exchange. Rio Tinto is also under similar investor pressure. Developers like Marimaca Copper are negotiating with ASX listings. It is to diversify from political volatility. The ASX is poised for investors seeking stable resource exposure.

NYSE miners benefit from strong policy momentum. It is due to the U.S. Inflation Reduction Act. The act has encouraged domestic investments. Australian miners provide access to raw resources. U.S.-listed firms take advantage of downstream integration. They also have better ties to car manufacturers. Albemarle’s Nevada operations add lithium capacity domestically. Freeport-McMoRan is a copper powerhouse supplier. It wields global clout through its Grasberg mine. This offers varied strategies for investors. ASX giants provide access to stable regimes. NYSE companies provide growth based on U.S. industrial policy.

Risks and Regional Investment Guidance

The biggest threat is commodity cycles. This is for ASX and NYSE companies. Iron ore, copper, and lithium prices change. This is linked to Chinese demand and infrastructure spending. Geopolitical tensions contribute to volatility as well. These tensions range from trade wars to resource nationalism. ESG risk focus is also an element. Rio Tinto has had cultural heritage problems. Fortescue has an ambitious green hydrogen plan.

For Australian investors, listed mining opportunities have diminished. This is due to acquisitions and mergers. This creates scarcity value in major producers. For U.S. investors, policy risk is present. The trajectory of the Inflation Reduction Act can influence project economics. For Australian investors, BHP, Rio Tinto, and Fortescue are core holdings. BHP offers diversification in an array of commodities. This makes it a less volatile choice. Rio Tinto is attractive for its dividend resilience. Fortescue is attractive to yield-strapped investors. It exposes the investor to more concentration risk.

The Global Strategy of Large Miners

U.S. investors look to Albemarle for lithium. They look to Freeport-McMoRan for copper dominance. This aligns with the domestic focus on secure supply chains. UK and European investors use ADRs or ETFs. The Global X Lithium & Battery Tech ETF (LIT) is popular. It has exposure to both bourses. Geographic preferences drive investor positioning. Those seeking stability and dividends prefer ASX leaders. Those looking for growth aligned with U.S. policy could prefer NYSE miners. The group has exposure to short cycles. It has exposure to long cycles of energy transition as well.

Also Read: https://colitco.com/pacgold-limited-reports-strong-gold-drilling-results/

A Look at Future Demand and Supply

The battery industry faces pressure on prices. World battery prices dipped sharply in 2024. This was due to China’s overcapacity. It was also due to falling raw material prices. Chinese battery plants are operating below 50% capacity. This is a short-term imbalance. Analysts are forecasting a moderation of prices in the short term. Long-term demand will accelerate.

New technologies like solid-state batteries may transform demand. Copper, lithium, and aluminum will, however, remain central materials. This will be so at least until 2040. More will be provided by recycling. It will only meet part of the long-term demand. It will only meet 27% of the 2050 EU copper demand. Primary extraction will still be needed. ASX and NYSE company comparison is different. Each exchange offers a different strategic position. The industry is set to develop as the world undergoes the energy transition.

{kind=link}

{kind=link}

{kind=link}