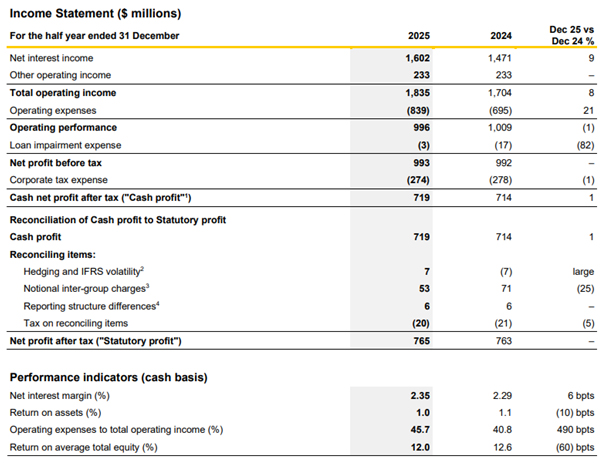

Commonwealth Bank of Australia (ASX: CBA) has released its ASB Bank subsidiary results for the six months ended 31 December 2025. The CBA half-year results show ASB posted cash net profit after tax of NZ$719 million, up 1 per cent on the prior comparative period.

Figure 1: Commonwealth Bank of Australia headquarters building [Source: Retail Banker International]

The New Zealand banking subsidiary delivered solid lending growth across home, business, and rural sectors despite ongoing economic uncertainty. ASB’s statutory net profit after tax reached NZ$765 million for the half-year period, whilst total customer deposits increased 5 per cent.

CBA Half-Year Results Show Strong ASB Lending Performance

Commonwealth Bank half-year results reveal ASB’s home lending portfolio grew 8 per cent since December 2024. Business and rural lending expanded 4 per cent over the same period. Total customer deposits increased 5 per cent, demonstrating continued customer confidence in the subsidiary.

Net Interest Margin rose 6 basis points to 2.35 per cent, driven by higher earnings from timing effects related to interest rate hedges. ASB Chief Executive Vittoria Shortt stated the bank is seeing more confidence in the economy, supported by lower interest rates and good export earnings in key sectors.

Commonwealth Bank Half-Year Results Include Significant Expense Increase

The CBA half-year results showed ASB’s operating expenses jumped 21 per cent to NZ$839 million. The increase was largely driven by settlement of Credit Contracts and Consumer Finance Act 2003 class action proceedings, plus investments in people, technology modernisation, digital experience, and regulatory compliance.

Figure 2: ASB Bank income statement and key performance indicators for the half year ended 31 December 2025 [Source: Commonwealth Bank of Australia]

Operating performance declined 1 per cent to NZ$996 million as expense growth outpaced revenue increases. The expense ratio deteriorated to 45.7 per cent from 40.8 per cent, whilst return on average total equity declined 60 basis points to 12.0 per cent.

CBA Shareholder Update Highlights Digital Investment Strategy

The CBA shareholder update emphasised ASB’s continued investment in customer experience and technology modernisation. The subsidiary extended digital home loan application functionality in November 2025 to include joint applications through the ASB Mobile App. Customers can track application progress and view indicative pricing at every step.

ASB now manages more than NZ$31 billion for investors across five products. The ASB KiwiSaver Scheme grew funds under management by more than NZ$1.7 billion to exceed NZ$20.6 billion. Four ASB KiwiSaver Scheme funds achieved top quartile performance for the 12 months ended 31 December 2025.

Balance Sheet Strength in Commonwealth Bank Half-Year Results

Commonwealth Bank half-year results showed ASB’s total assets increased 6 per cent to NZ$139.7 billion as at 31 December 2025. Advances to customers grew 6 per cent to NZ$118.7 billion, whilst deposits and other borrowings remained flat at NZ$94.5 billion.

Figure 3: ASB statutory balance sheet highlights showing asset and lending growth as at 31 December 2025 [Source: Commonwealth Bank of Australia]

The balance sheet expansion demonstrates ASB’s ability to support customer lending demand whilst maintaining funding stability. Loan impairment expense dropped 82 per cent to NZ$3 million, indicating improved credit quality across the portfolio.

ASB Business Banking Initiatives Support Productivity

ASB is backing business customers to boost productivity through artificial intelligence and technology partnerships. Following a successful pilot, the programme with the New Zealand Product Accelerator and universities is scaling up this year to match up to 100 ASB business customers with AI, business analytics, and data science master’s students.

ASB grew rural lending more than any other bank in the 12 months to September 2025, according to Reserve Bank of New Zealand data. The subsidiary doubled its commitment to NZ$1 billion to accelerate development of social and affordable housing, with NZ$517 million committed to date.

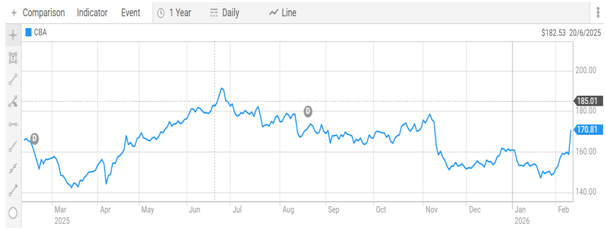

CBA Share Price and Market Performance

Commonwealth Bank of Australia shares last traded at $170.75 on the Australian Securities Exchange. The Company has a market capitalisation of $265.64 billion. The 52-week range for CBA shares is $140.21 to $192.00 per share.

Figure 4: Commonwealth Bank of Australia share price performance over the past year [Source: Australian Securities Exchange]

Final Thoughts

The CBA half-year results demonstrate ASB’s resilient performance in challenging conditions. Steady profit growth of 1 per cent reflects the balance between revenue expansion and necessary expense investments in technology, compliance, and customer experience.

The CBA shareholder update shows ASB is well-positioned to support customers as economic conditions improve. Strong lending growth across home, business, and rural segments indicates improving demand, though the elevated expense ratio and margin pressure warrant monitoring as the subsidiary navigates ongoing digital transformation.

FAQs

Q1. What profit did ASB Bank report in the CBA half-year results?

Ans. ASB Bank reported cash net profit after tax of NZ$719 million for the six months ended 31 December 2025, up 1 per cent on the prior comparative period. Statutory net profit after tax was NZ$765 million.

Q2. How much did ASB’s lending grow in the Commonwealth Bank half-year results?

Ans. ASB’s home lending grew 8 per cent since December 2024, whilst business and rural lending expanded 4 per cent. Total customer deposits increased 5 per cent over the same period.

Q3. Why did ASB’s operating expenses increase significantly?

Ans. Operating expenses rose 21 per cent to NZ$839 million, largely driven by the settlement of Credit Contracts and Consumer Finance Act 2003 class action proceedings.

Q4. What is ASB’s Net Interest Margin in the CBA shareholder update?

Ans. ASB’s Net Interest Margin increased 6 basis points to 2.35 per cent, driven by higher earnings due to timing effects from interest rate hedges.