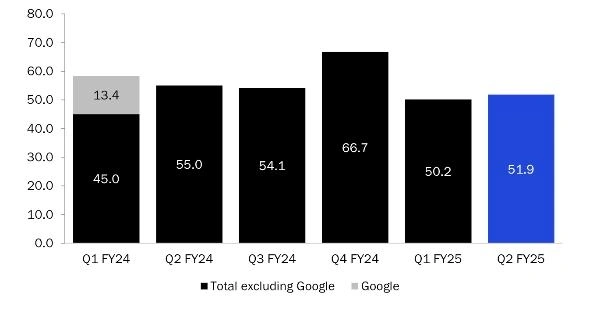

Appen Limited (ASX: APX) is the global leader in data annotation and AI training services, with its headquarters in Sydney, Australia. The company delivers finely human-annotated data to train machine learning models for some of the biggest tech firms. Appen Limited (ASX: APX) gave out a Q2 FY25 quarterly update on 30 July 2025, reporting mixed results across revenue, cost control, and profitability. For the quarter ended 30 June 2025, Appen reported revenue of US$51.9 million, representing a decline of 6 per cent over the year. However, there was a 3 per cent gain when compared with Q1 FY25.

Revenue for the H1 FY25, excluding Google-related work, stood at US$102.1 million, marking a 2 per cent increase from the same period in FY24. Management remarked that non-Google revenue was up for its second consecutive quarter in Q2. Appen’s strategic focus remains on margin recovery and China expansion.

How Did Appen Perform in the Chinese Market?

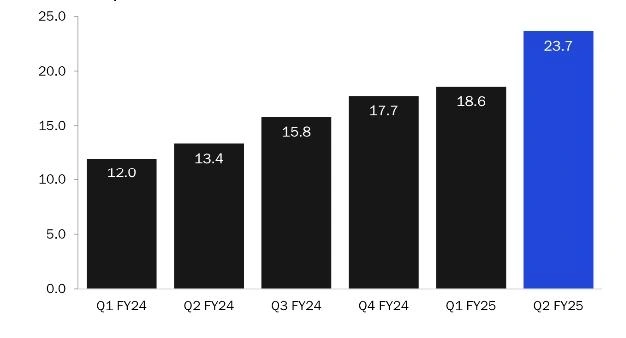

China stood out as Appen’s fastest-growing market. Q2 FY25 China revenues shot up 77 per cent to US$23.7 million. For H1 FY25, revenue in China rose 67 per cent year-on-year and reached US$42.2 million. Appen calls this LLM data demand and a brand-new enterprise deal.

The company also confirmed exiting Q2 with an annualised run-rate for China revenue of more than US$100 million. With the performance of the China segment, it appears to be on a solid upward trajectory. This emphasises the importance of the Asia-Pacific region to the global operations of the company. Investors may perceive China as the foremost pillar for revenue growth going forward.

Are Profit Margins Recovering?

Despite the sustenance of revenue in a few markets, the downstream profitability of Appen went under pressure. Gross margin for Q2 FY25 was 36.6 per cent, another drop from the 37.6 per cent recorded in Q2 FY24. For H1 FY25, the gross margin was 37.0 per cent, down 0.7 percentage points year-on-year.

Underlying EBITDA (excluding foreign exchange impacts) went into a loss of US$0.6 million in the quarter, in comparison to a gain of US$0.6 million during the same period last year. For H1 FY25, the EBITDA loss was US$2.2 million.

The company stated it had either implemented or was planning for approximately US$10 million in annualised cost savings, of which 70 per cent is expected to be realised by Q3 FY25, with the rest by Q4.

What’s Appen’s Current Financial Position?

Appen ended the quarter with US$60.9 million in cash. No borrowings were noted in the quarterly update. The company repeated its pledge for prudent cash management. Operating cash outflow for Q2 FY25 improved to US$3.7 million from US$5.5 million in Q1 FY25.

Capital expenditure remained modest. Appen reported an investing cash outflow of US$1.0 million. The business model remains capital-light. The current cash balance would be able to sustain medium-term strategic initiatives, particularly in technology automation and data delivery.

Can Cost Efficiencies Drive Future Profitability?

Appen will proceed with operational optimisation. The efficiency initiative targets roughly US$10 million of cost savings on an annualised basis. Most of these savings come into effect during Q3 and Q4 of FY25. The initiatives are focused on streamlining operations, automating workflows, and optimising global workforce management.

CEO Armughan Ahmad has expressed that “to be able to claim profitable growth” is what the changes are committed to. Management wants continuous cost control to build the long-term vision for growth. Should these savings be realised on the scheduled dates, one could expect margin recovery to commence sometime in H2 FY25.

What Should ASX Investors Expect Going Forward?

Q2 FY25 results for Appen show stabilising revenue, strong cash reserves, and ongoing margin pressure. Appen witnessed a 3% revenue quarter-on-quarter increase while under-the-surface EBITDA remained negative. Costs are slated for a $10-million annualised reduction, with the majority of these savings contingent in Q3 of FY25. Should they materialise, they could therefore see profitability return in H2.

Considered a key player in the global setting, the US$ 2792.2 billion AI market in the year 2024 is forecasted to reach US$18117.5 billion by 2030, advancing at a CAGR of 35.9% through the years 2025-2030. Thus, positioned as a major data vendor, Appen stands to gain.

The main risk that remains is execution, especially for sustaining growth outside the Google-related contracts. For ASX investors, attention would then be on margin revival, cost control, and earnings consistency. Should these come to pass, Appen may yet regain investor confidence and improve its status as a major tech stock out of Australia on the ASX.

Also Read: Osmond Secures Flagship Project Permit and Prepares to Launch Maiden Drill Program in Spain

Questions for the Future

Can Appen ever restore full-year profits in FY25?

If further margin improvements can be realised and Chinese revenues continue to set records, it may well be that profit will return by year-end.

At what rate can China continue to grow?

In Appen’s view, LLM demand in China is long-term, but macroeconomic changes and local competition might temper such momentum.

Are Appen and related coinvestment vehicles transitioning through global shifts in AI platforms?

With the exclusion of Google from its client base, Appen’s future rests firmly on diversification across clients and delivering improved levels of meeting performance.