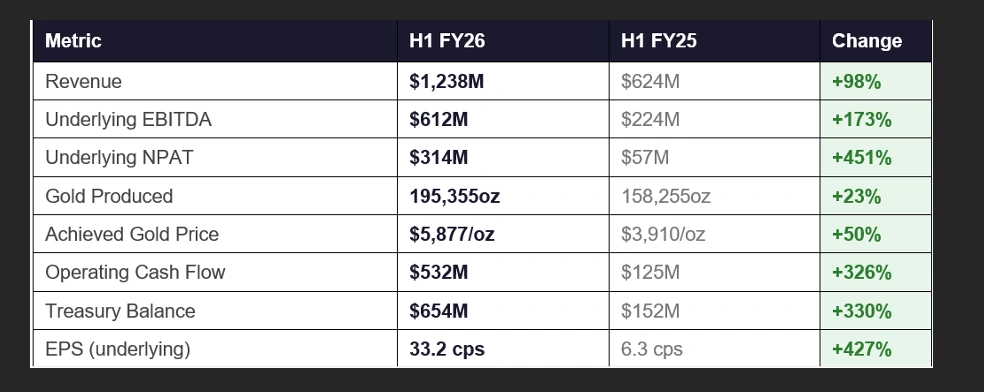

Gold mining on the ASX has had no shortage of winners in the current bull market, but few companies have captured investor attention quite like Westgold Resources Limited (ASX/TSX: WGX). The Perth-based gold producer delivered its half-year results for the period ending 31 December 2025 today, and by virtually every measure, the numbers were extraordinary.

Revenue nearly doubled to $1.238 billion. Underlying net profit after tax surged more than fivefold to $314 million. The company is now 100% debt free, sitting on a treasury balance of $654 million. And with full-year production guidance maintained at 345,000 to 385,000 ounces, there is no sign of the company resting on its laurels.

So what exactly is driving the investor conviction behind Westgold in 2026? We break down the key reasons the market keeps backing this mid-tier gold miner.

H1 FY26 at a Glance — Key Financial Results

Figure 1: Financial Results of Westgold Resources in H1 FY2026

Figure 1: Financial Results of Westgold Resources in H1 FY2026

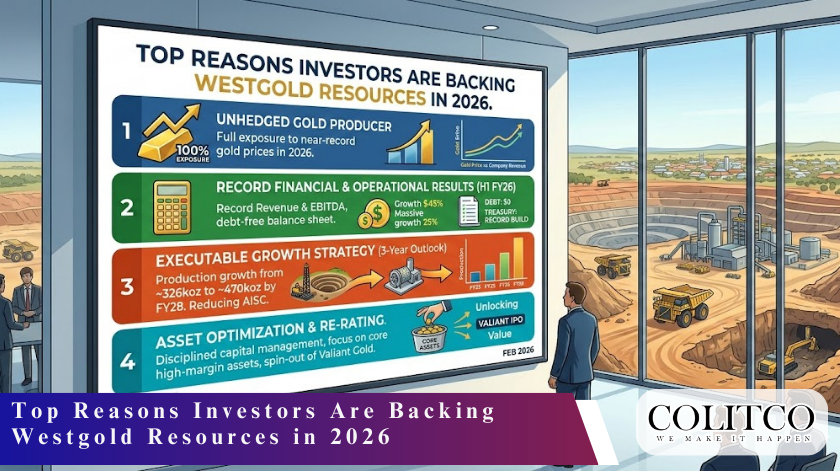

1. A Gold Price Tailwind That Westgold Is Perfectly Positioned to Exploit

The single biggest driver of Westgold‘s extraordinary H1 FY26 results is unmistakably the gold price. The company achieved an average realised gold price of $5,877 per ounce during the period — a 50% increase from $3,910 per ounce in the prior corresponding period. When you are producing nearly 200,000 ounces in a half year, that kind of price uplift flows directly to the bottom line.

Crucially, Westgold operates as an unhedged gold producer. This is not a company that has locked in forward sales at prices below current spot levels. When gold runs, Westgold runs with it — fully and without reservation. That decision to remain unhedged has proven spectacularly prescient in the current environment, and it is a key reason the company delivered what management described as record returns for shareholders.

“As an unhedged gold producer operating within a strong market environment, we delivered record returns for shareholders in H1 FY26.” — Wayne Bramwell, MD & CEO, Westgold Resources.

For investors who believe the structural case for gold remains intact — whether driven by geopolitical uncertainty, central bank buying, or ongoing concerns around fiat currency debasement — Westgold represents a high-leverage, pure-play exposure to the yellow metal at a scale that increasingly matters.

2. A Balance Sheet That Has Gone From Leveraged to Fortress

Not long ago, Westgold was carrying debt on its books following its transformative merger with Karora Resources in 2024. Today, after repaying the last $50 million of its credit facility in December 2025, the company is completely debt free.

The treasury balance, comprising cash, bullion, and liquid investments, stood at $654 million as at 31 December 2025, up from just $152 million a year prior. That is a fourfold increase in twelve months. Even after absorbing $76 million in Karora-related stamp duty, $129 million in growth and exploration capital, $29 million in dividends and share buybacks, and $50 million in debt repayment, the underlying treasury build for the half was $550 million.

A fortress balance sheet matters for gold investors for several reasons. It provides the capital firepower to pursue accretive acquisitions when the cycle turns. It insulates the company from the kind of financial stress that has plagued over-leveraged miners in past downturns. And it allows management to continue investing in organic growth without the constraining hand of a bank hovering over its shoulder.

Cash Generation That Speaks for Itself

Net cash flow from operations reached $532 million for the half, up from $125 million in the prior period. Investing cash outflows fell to $136 million from $257 million as the company moves from acquisition mode into operational execution. The combination of surging operating cash flow and disciplined investment spending means Westgold is generating cash at a rate that is genuinely transformational for its market capitalisation of approximately $7.2 billion.

3. The Karora Merger Is Delivering — and Then Some

The $2.5 billion all-scrip merger with Canadian gold miner Karora Resources, completed in 2024, was the defining corporate event that elevated Westgold into the mid-tier category. At the time, sceptics questioned the price paid and the integration complexity. Eighteen months on, the results are doing the talking.

The integration of Karora’s Southern Goldfields assets, including the Beta Hunt mine and the Higginsville processing hub, has expanded Westgold’s operational footprint to cover approximately 3,200 square kilometres across Western Australia’s most prolific gold regions.

The Murchison operations contribute the majority of group revenue, but it is the Southern Goldfields segment that is poised for the most significant production growth heading into the second half of FY26 and beyond.

Beta Hunt, in particular, is a mine that has attracted considerable attention. Development investment in H1 FY26 has been deliberately front-loaded to position the operation for a production ramp-up in H2 FY26. While this contributed to a higher AISC figure for the period, it reflects investment in future output rather than operational inefficiency.

Murchison Driving the Bus, Goldfields in the Wings

In the Murchison region, the expansion of the Bluebird–South Junction mine at Meekatharra is progressing well, while the Great Fingall mine near Cue has commenced commercial production. These organic growth catalysts, funded entirely from operating cash flow, represent exactly the kind of accretive self-funded investment that creates long-term shareholder value.

4. A Disciplined Portfolio Rationalisation Strategy

One of the more underappreciated aspects of Westgold’s strategy in 2026 is the systematic divestment of non-core assets. Rather than accumulating a sprawling portfolio and hoping it all works out, the company is actively pruning assets that do not fit its core operational focus.

The sale of the Mt Henry–Selene Gold Project to Alicanto Minerals is a case in point. While the transaction generated a one-off, non-cash accounting loss of $178 million at the half-year balance date (due to the provisional valuation of Alicanto shares at $0.15), by early February 2026 the value of Westgold’s resulting 19.9% stake in Alicanto had appreciated such that the share consideration increased from $64.6 million to $110 million.

The company also received $15 million in immediate cash proceeds, with up to $30 million in deferred consideration tied to project milestones.

The planned Valiant IPO, through which Westgold is spinning out its Reedy’s and Comet assets into a separately-listed vehicle, is scheduled to commence trading on the ASX in March 2026. The divestments of the Chalice and Peak Hill assets are also progressing.

Each transaction cleans up the portfolio, potentially unlocks hidden value, and allows management to allocate its attention and capital more efficiently to its highest-return operations.

“Our outlook is supported by a defined strategy: to enhance and optimise outputs from our core assets while identifying opportunities to create additional value for shareholders from select non-core projects.” — Wayne Bramwell, MD & CEO

5. Three-Year Outlook Provides Rare Visibility

In a sector notorious for short-term thinking and guidance that is perpetually ‘under review’, Westgold has taken the unusual step of publishing a Three-Year Outlook through FY28. This level of forward visibility is genuinely rare among mid-tier Australian gold producers, and it is a signal of management’s confidence in the quality and predictability of its asset base.

For the current financial year, production guidance of 345,000 to 385,000 ounces at an AISC of $2,600 to $2,900 per ounce has been maintained without change. With the gold spot price currently trading well above $5,000 per ounce (Australian dollars), even the top end of the AISC guidance still implies margins that are the envy of the sector.

The three-year outlook includes anticipated production growth driven by the Beta Hunt ramp-up, the Bluebird–South Junction expansion, Great Fingall’s commercial production, and the Higginsville processing hub optimisation. If management executes to plan, Westgold will be meaningfully larger and more profitable by FY28 than it is today — and it is already posting record results.

6. Share Price Performance That Has Outpaced the Market — With More Road Ahead

Over the twelve months to 26 February 2026, Westgold shares have risen approximately 221%, compared to around 11% for the S&P/ASX 200 over the same period. This is the kind of outperformance that has attracted attention from investors well beyond the traditional resources sector.

The 52-week range for WGX has been $2.41 to $7.93, with the stock trading at approximately $7.61 at the time of writing. The current market capitalisation of roughly $7.2 billion reflects a company that has undergone a genuine re-rating as its earnings quality has improved. The consensus analyst view among the five to eight analysts covering the stock is a Buy, with an average price target of approximately $8.56, suggesting further upside from current levels.

It is worth noting, however, that Westgold is not immune to the risks that come with any resources investment. AISC increased 12% year-on-year (excluding the OPA), driven in part by higher royalty payments reflecting the stronger gold price, and increased development activity at key mines. Gold price volatility remains the key swing factor. And while the balance sheet is pristine, the company’s geographic concentration in Western Australia means exposure to the labour cost pressures and operational challenges endemic to the Western Australian mining sector.

7. Capital Returns: Active Buyback, Dividend Policy Intact

Westgold’s Board elected not to pay an interim dividend for H1 FY26, a decision management framed as prioritising near-term growth investment over a cash distribution. This will disappoint some income-focused investors, though the company’s dividend policy remains in place — targeting an annual minimum of 2 cents per share, up to 30% of free cash flow.

The share buyback programme remains active and continues to purchase stock on market, subject to trading restrictions. For investors, an active buyback at a time when the company is generating record free cash flow is arguably a more capital-efficient use of funds than a one-off dividend, as it reduces the share count and concentrates future earnings per share.

The combination of a buyback, maintained dividend policy, and a treasury balance of $654 million gives Westgold considerable flexibility in how it returns capital to shareholders over the remainder of FY26 and into FY27.

The Risks Investors Cannot Ignore

No investment analysis is complete without a candid assessment of the risks, and Westgold carries several that warrant careful consideration.

The gold price is the primary lever on which all of Westgold’s financial outcomes hinge. A meaningful pullback in the gold price, whether driven by a stronger US dollar, rising real yields, or a shift in market sentiment, would directly compress margins. Given the company’s unhedged position, there is no floor protecting earnings from a gold price correction.

AISC has risen 12% year-on-year and, while the current gold price more than compensates, cost discipline will be critical if the price environment becomes less supportive. The inclusion of the ore purchase agreement (OPA) with New Murchison Gold, which contributed 25,000 ounces at an AISC of $5,644 per ounce, is a useful reminder that not all production is created equal.

The statutory profit of $190.7 million also notably reflects a one-off, non-cash accounting loss of $178 million on the Mt Henry–Selene divestment. While this does not affect cash flows, it does cloud the headline statutory earnings figure for investors who do not dig into the underlying metrics.

The Bottom Line

Westgold Resources has evolved from a modestly-sized Western Australian gold producer into a genuinely significant mid-tier miner in the space of just a few years. The Karora merger gave it scale. The gold price gave it earnings power. And disciplined capital management has given it a balance sheet that virtually no gold company of its size can match.

The H1 FY26 results are, by any measure, exceptional, but the more intriguing question for investors is whether Westgold can sustain and build on them. The combination of organic growth catalysts, portfolio rationalisation proceeds, and a favourable gold price environment suggests that the answer may well be yes.

With the Valiant Gold IPO approaching, Beta Hunt ramping, and a treasury flush with cash, 2026 is shaping up to be a pivotal year for the company. For investors with exposure to gold as a portfolio theme, Westgold remains one of the more compelling ways to express that conviction on the ASX.

WGX shares have risen 221% over the past twelve months. If the H1 FY26 results are any guide, the underlying business has only just begun to hit its stride.

Sources

- Westgold Resources — Official ASX Announcement: “Half Year Financial Results Summary – H1 FY26” Westgold Resources Limited, 26 February 2026: https://www.westgold.com.au/pdf/02a68350-3bbf-4f90-afc1-9c6c4d82db66/Half-Year-Financial-Results-Summary-H1-FY26.pdf

- The Motley Fool Australia: https://www.fool.com.au/2026/02/26/westgold-resources-posts-record-profit-and-revenue-for-h1-fy26/

- Westgold Resources — Investor Presentation (Official): “FY26 Half Year Results Presentation” Westgold Resources Limited, 26 February 2026 https://www.westgold.com.au/pdf/d403714d-b9f1-4853-a7e5-5c7626c67475/FY26-Half-Year-Results-Presentation.pdf