Evolution Mining Limited’s share price rose by a strong 6.74% after the Company reported its strongest half-year result to date for the period ending 31 December 2025. As of 1:15 pm AEDT on 11 February 2026, the Company’s market capitalisation stood at nearly A$32.47 billion, up from A$30.41 billion the previous day.

Record results, delivered with discipline

In the six months to December 2025, Evolution moved decisively from recovery to acceleration.

The Company reported:

- Underlying profit after tax of $785 million, up 104% year-on-year.

- Record Group cash flow of $608 million, up 123%.

- Record underlying EBITDA of $1.6 billion with a sector-leading margin of 57%.

- Production of 365,000 ounces of gold and 36,000 tonnes of copper, on track with guidance.

- All-in sustaining cost (AISC) of $1,493/oz, maintaining a competitive cost position.

Managing Director and CEO Lawrie Conway framed the result as the product of consistent execution rather than luck.

Evolution’s balance sheet now looks markedly stronger. Gearing has fallen to 6%, cash has climbed to $967 million, and the Company has no debt repayments due until FY29.

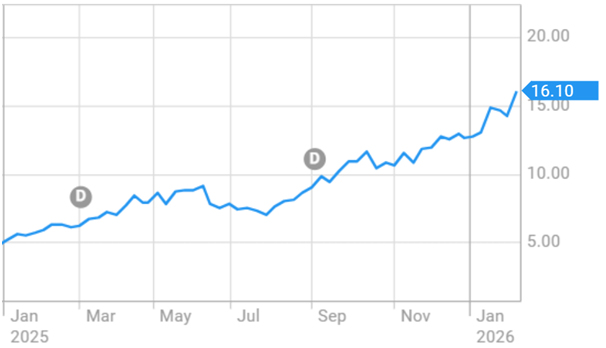

Figure 1: ASX: EVN performance snapshot for 1 year

Operations: every mine in the black

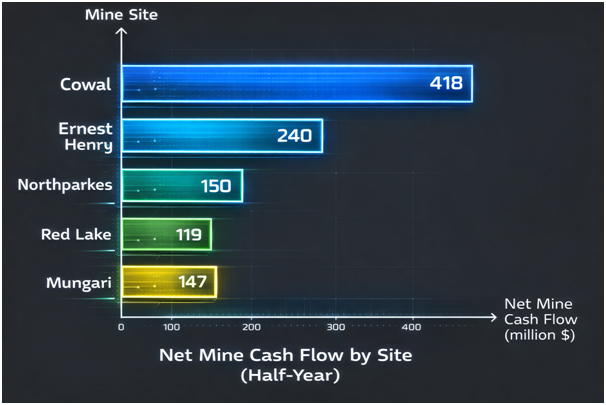

All six operating sites delivered positive net mine cash flow, a notable achievement in a sector often characterised by volatility.

Half-year net mine cash flow highlights included:

- Cowal: $418 million (up 56%)

- Ernest Henry: $240 million (up 65%)

- Northparkes: $150 million (up 216%)

- Red Lake: $119 million (up 171%)

- Mungari: $147 million, reversing a prior period loss

Collectively, Evolution’s operations generated $1.093 billion in net mine cash flow, more than double the prior corresponding period.

The results reflect stable costs, strong operational discipline and the benefit of higher metal prices rather than one-off gains.

Figure 2: All six Evolution mines generated positive cash flow, led by Cowal, while Northparkes, Ernest Henry, Red Lake and Mungari lifted net cash to $1.093 billion.

Northparkes: the next wave of growth

Northparkes has emerged as a central pillar of Evolution’s growth strategy.

The Board has approved the E22 block cave project, a long-life, low-cost underground development designed to support plant utilisation at around 7.4 million tonnes per annum and enable a transition to 8 Mtpa.

Some important features are:

- $545 million in capital spread over five years.

- Initial production targeted from the end of FY30.

- Forecast internal rates of return of 28% at base prices and 38% at upside prices.

- A twin-decline design, revised ventilation and four tipping points to lift crusher productivity.

Alongside E22, Evolution will advance the Coarse Particle Flotation Project, expected to improve copper and gold recovery by about 2%, lift throughput and reduce energy intensity. Commissioning is slated for the second half of FY28.

The Company is also undertaking an expansion study to examine options for materially increasing mill capacity, with results due by the end of FY27.

Figure 3: Location of the Northparkes Mine in Australia [Evolution Mining]

Ernest Henry and Bert: extending and enhancing production

At Ernest Henry, Evolution has approved development of the Bert deposit, an incremental satellite mine that will unlock latent mill capacity and add both gold and copper to the production profile.

The Bert project involves $160 million in investment, offers an estimated seven-year mine life from FY29 and is expected to generate returns of 23% at base prices and 48% at upside prices.

Separately, a mine continuation study has confirmed that Ernest Henry can operate to around 2040 while maintaining its current production rate of 6.8Mtpa, with potential to extend further at depth.

Cowal: a cornerstone asset through 2042

Cowal continues to underpin Evolution’s portfolio as a long-life, low-cost producer.

Recent approvals have extended open pit mining by a decade, pushing operations out to 2042. Underground development is progressing ahead of schedule, with early access to the E46 orebody and construction of a southern bund to support lake protection.

At full scale, underground mining will account for around one-third of mill feed and half of total gold output at Cowal.

Mungari and Red Lake: optionality and resilience

Mungari has rebounded strongly, delivering $147 million in half-year cash flow and tracking toward a 200,000oz per annum run rate in the second half of FY26.

Evolution has invested in sealed haul roads, new accommodation hubs and a partnership with contractor MLG to improve logistics from Castle Hill and Kundana.

Red Lake in Canada has generated roughly $200 million in net mine cash flow over the past 18 months. The creation of a surface stockpile has strengthened operational resilience and provided greater flexibility across three active mining fronts.

Shareholders rewarded: a record dividend

Evolution has declared its 26th consecutive dividend, a fully franked 20 cents per share interim payment, nearly three times the prior half.

- Record date: 4 March 2026

- Payment date: 2 April 2026

The Company has maintained its policy of distributing around 50% of annual Group cash flow and has now declared more than $2 billion in dividends since FY13.

The Dividend Reinvestment Plan remains in place, with the previous discount removed.

Market reaction

Evolution Mining’s share price performance has shown massive strength over the past year. On the day of the announcement itself, the share price grew by 6.74%.

Share Price Activity (ASX):

- Last price: $15.99

- Change: +1.01 (+6.74%)

Performance:

- 1 week: +10.58%

- 1 month: +24.73%

- 2026 YTD: +26.10%

- 1 year: +157.07% (outperforming both the sector and the ASX 200)

Market capitalisation now stands at $32.47 billion, placing Evolution firmly among Australia’s largest gold producers.

Figure 4: Evolution Mining’s stock has shown steady growth over the past year and has continued this momentum into 2026. [ASX]

FY26 guidance: steady and credible

Evolution has reaffirmed FY26 production guidance of 710–780koz of gold and 70–80kt of copper, with Group AISC expected between $1,640 and $1,760 per ounce.

Capital plans reflect the newly approved projects at Northparkes, Ernest Henry and Cowal, while sustaining capital remains unchanged.

Also Read: CSL CEO Exits Hours Before Earnings Release: What It Means for Investors

Investors Outlook

Evolution Mining enters the second half of FY26 from a position of unusual strength.

The Company combines three rare qualities: robust cash generation, a deleveraged balance sheet and a clear, fully funded growth pipeline. Northparkes and Bert should lift production and margins over time, while Cowal and Ernest Henry provide long-life stability.

Near term, elevated gold and copper prices offer a meaningful tailwind. Even if prices ease, Evolution’s low cost base and disciplined capital approach should protect returns.

Risks remain, including project execution, commodity volatility and permitting timelines, but the portfolio now looks better balanced than at any point in the past decade.

For income-focused investors, the rising dividend track record stands out. For growth investors, the approved projects and Canadian exploration create genuine upside optionality.