Cepheus-1-108Q Cepheus computation computer is yet to be launched by Rigetti Computing, following technical challenges. This move came at a time when competitor IonQ was hastening its production drive.

The uncertainty regarding timelines and execution also led to a swift reaction by investors. This pressure was seen on the Rigetti Computing stock price nearly instantly. The business recorded a 1-day share price change of 12.89%.

The 30-day share price turnover was 41.00%. In spite of the said moves, the year-to-date share price return is in the red at 36.55%. The longer-term figures are also stronger, having 1 year total shareholder return of 12.68.

The total shareholder return over the past 3 years is over 13x. These are mixed signals that indicate volatility in the quantum sector.

The quantum hardware hopes of Rigetti are met with new launch setbacks. [The Economic Times]

Market Expectations Reset Across Quantum Names

The delay has caused a more comprehensive reappraisal of quantum computing stocks. Commercial preparedness is also being questioned by the traders in the short term. The defeat by Rigetti made investors draw more comparisons between peers.

Some have 22 quantum computing stock screenings. The market participants desire companies that have better-defined delivery channels.

The delay also changes the mood towards execution risk as opposed to bare growth stories. This setting tends to reduce the valuations in the short run. Nevertheless, the quantum solutions are still demanded in relation to defence and enterprise.

Governments are still aggressive in terms of research and development. The support can soften the long-term outlook. The present weakness is then a time issue, but not an industry meltdown.

Is Rigetti Computing Valuation Now Too Cheap To Ignore?

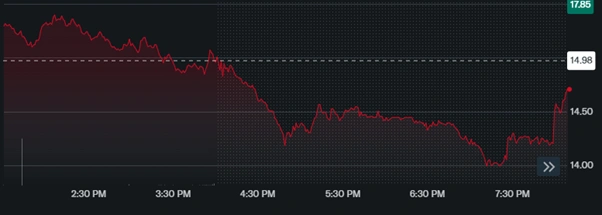

Rigetti closed at 14.98 at the end of the day. Narrative fair value is 24.50. This gap implies a 38.9% discount. This kind of disparity puts the Rigetti Computing valuation centre stage.

Analysts contend that the market can be charging years of risk ahead. It is viewed by others as a desirable entry point for patient investors.

The Company continues to be in a high-growth technology niche. Adoption may proceed faster with policy support, such as research funding related to defence.

But still, profitability is far off. The losses continue, and this is what makes many institutions suspicious. Opportunity, as well as the execution risk, is therefore reflected in the discount.

Rigetti SHare Trend. [Yahoo Finance]

Growth Assumptions Still Drive The Bull Case

The proponents of the stock concentrate on growth measures. Rigetti aims at fast revenue growth in the context of commercial relations. It is projected to grow revenue by 54.63 per cent per annum.

That rate is not common even with high-technology companies. The margin will also improve with time, as anticipated by analysts. Scale benefits might be succeeded by a higher future earnings multiplier.

These levers favour the fair value estimation that is higher. In the event of an increase in cash flow, trust can be restored soon. Revenue visibility could be stabilised by defence and enterprise contracts.

Nevertheless, it is still important to transform growth into profits. In the absence of this change, the arguments of valuation become weak. The solution will be whether the optimism is warranted.

Can Rigetti Reduce Its Losses Fast Enough?

The Company has a net loss of US$350.964 million. The implementation of this number will be a focus when it comes to investor confidence.

Further heavy expenditures with no results can push patience to the limit. The management should be disciplined when investing in research. The shortening of the cycle of loss might happen because of partnerships and customer wins.

Close business relationships could also enhance cash flow. Analysts anticipate that 2025 will make relations stronger. The next year may be a turning point in terms of operations.

Nevertheless, failures such as the Cepheus delay test are a blow to credibility. Recurring delays are usually penalised in markets. Investors are currently demanding more definite milestones and transparency.

Investors monitor losses and cash flow to take turnaround signals. [ScanX]

Rigetti Computing Stock Faces A Critical Crossroads

The Rigetti Computing stock is now in the stage of promise and reality. Quantum computing is a strategic issue at the global level. The industry may still be sustained by public-private funding. But the short-term volatility may remain.

Rigetti Computing’s stock price will be sensitive to the news flow. The most important are delivery schedules, alliances and margins.

Discount may be reduced in no time in case the targets are achieved. Pressure can increase in case of further delay.

This is a risk and a potential reward with regard to global investors. The next quarters can be the determinant of the credibility and valuation trend of the Company.

Also Read: Global Stock Market Fall Triggers Trillion-Dollar Tech Rout

FAQs

Q1: Why did Rigetti delay the Cepheus-1-108Q launch?

A1: Technical setbacks forced the Company to postpone the quantum computer rollout.

Q2: What is Rigetti’s current fair value estimate?

A2: Narrative fair value stands at $24.50 versus a $14.98 last close.

Q3: How fast is Rigetti expected to grow revenue?

A3: Analysts forecast 54.63% annual revenue growth.

Q4: What is the Company’s current loss position?

A4: Rigetti reports a US$350.964 million net loss base.