Short sellers remain active across the Australian Securities Exchange, with Week 36 delivering some significant shifts in sentiment that savvy investors shouldn’t ignore. The latest data from the Australian Securities and Investments Commission (ASIC) reveals fresh insights into which stocks are attracting bearish bets and which are seeing covering activity.

Remember, this short-selling data operates on a T+4 basis – meaning the figures reflect positions from four trading days earlier. This delay exists because reporting isn’t mandatory until three business days after trades occur.

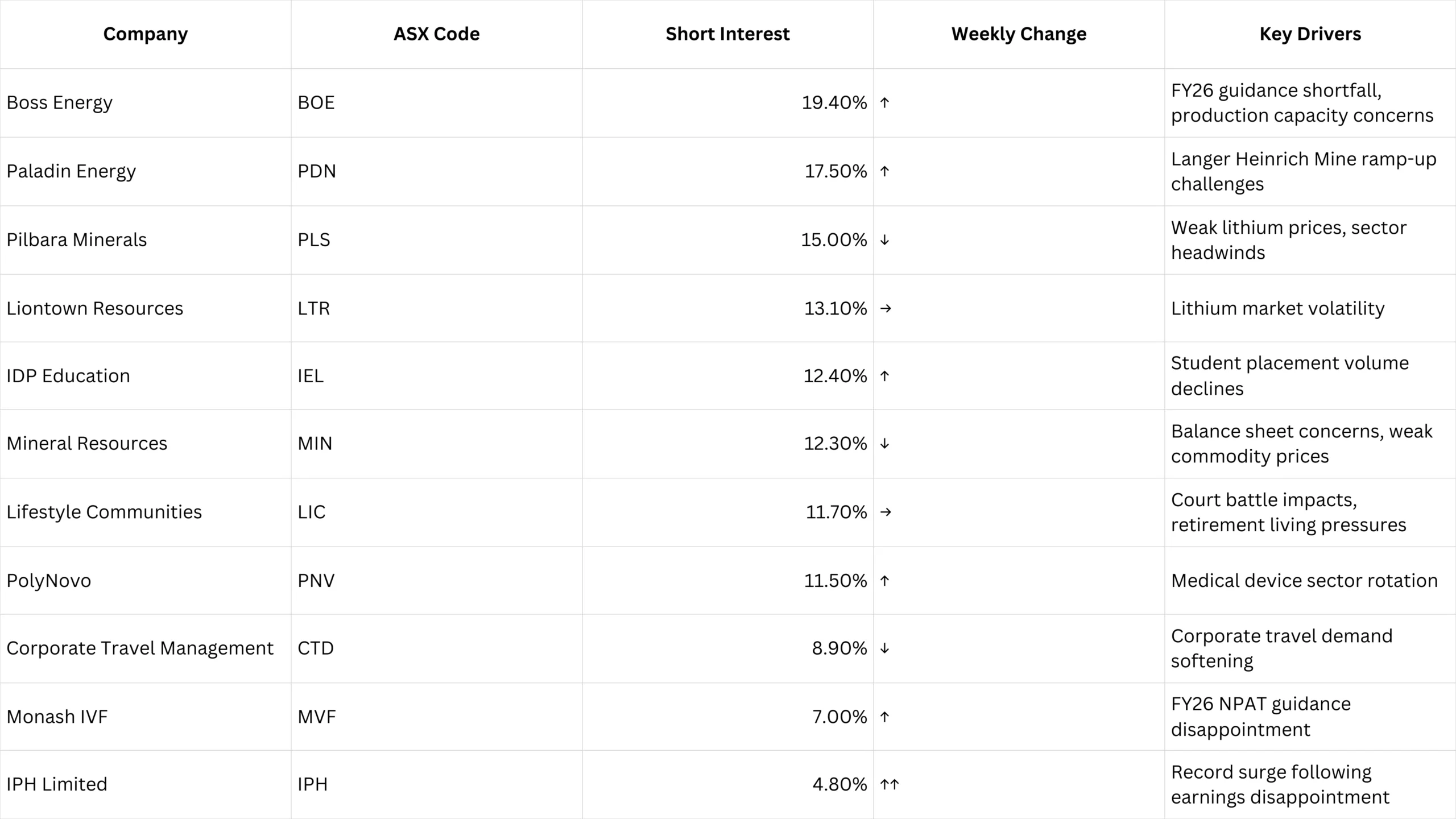

Week 36 ASX Most Shorted Stocks

The following table shows the current short interest levels for the most heavily shorted stocks on the ASX, along with key drivers behind recent movements:

IPH Limited Hits Record Short Interest Levels

The standout move in Week 36 came from IPH Limited, which saw short interest surge from roughly 1.5% to a record 4.80%. This dramatic spike followed the intellectual property services company’s disappointing FY25 earnings release on 21 August.

The market reacted harshly to IPH’s guidance, with shares plunging 19.5% on results day. The company flagged persistent market share losses in Australia and New Zealand, weaker US PCT filings, and a slower-than-expected Asian recovery. While strong Canadian performance and cost-cutting initiatives provided some offset, short sellers clearly weren’t convinced by the turnaround story.

Analysts noted that despite the challenges, IPH’s valuation appears relatively undemanding. However, the structural and regional headwinds facing the business have clearly attracted bearish sentiment.

Boss Energy Maintains Heavy Short Interest

Boss Energy continues to attract significant short interest, remaining near the top of the ASX most shorted stocks list with 19.4% of shares held short. This represents a return to the number one spot for the uranium producer.

The company’s shares crashed deep into the red last month after guidance for FY2026 fell materially short of expectations. Boss flagged potential challenges achieving nameplate capacity due to “potential for less continuity of mineralisation and leachability.” An independent review is underway to assess the impact on feasibility study assumptions, creating ongoing uncertainty that short sellers are capitalising on.

Despite the recent volatility, Boss Energy has been actively expanding its uranium portfolio, recently increasing its stake in Laramide Resources to secure exposure to Queensland’s Westmoreland Uranium Project.

Paladin Energy Faces Continued Pressure

Paladin Energy sits second on the ASX shorted stocks list with 17.5% short interest. The increase appears driven by concerns over the ramp-up of the uranium miner’s Langer Heinrich Mine project in Namibia.

The company faced operational challenges in November 2024, revising its FY2025 production guidance downward to between 3.0 and 3.6 million pounds of U3O8, from the previous estimate of 4.0 to 4.5 million pounds. These setbacks led to a significant share price drop, though the company expects production to increase in the second half of FY2025.

Other Notable Movements in Week 36

Monash IVF experienced a similar short interest spike to IPH, rising from around 5% pre-results to just over 7.0%. While FY25 numbers met market expectations, FY26 NPAT guidance disappointed investors.

Pilbara Minerals saw short interest ease to 15%, though it remains among the most heavily shorted names. Weak lithium prices continue weighing on both sentiment and profitability across the lithium sector.

Interestingly, some covering activity emerged around reporting season disappointments including IGO, Audinate, Origin Energy, and Digico, suggesting short sellers may be taking profits after successful bearish bets.

Market Context: Mining Stocks Under Pressure

The concentration of Week 36 ASX market movers in the resources sector reflects broader challenges facing mining companies. ASX uranium stocks have been particularly volatile, with the sector experiencing significant swings based on commodity price movements and operational updates.

Despite recent weakness, uranium’s long-term fundamentals remain supported by growing global nuclear energy programmes and supply constraints. The World Nuclear Association projects a 28% rise in global uranium demand by 2030, driven by major economies expanding their nuclear energy capacity.

Understanding Short Selling Data

Short selling involves borrowing shares to sell immediately, with the intention of buying them back at a lower price later. The practice is legal in Australia but strictly regulated by ASIC, with all positions above certain thresholds requiring daily reporting.

Investors should view short interest data as one factor among many when making investment decisions. High short interest can sometimes signal fundamental problems with a company, but it can also create conditions for a short squeeze if positive news emerges unexpectedly.

Looking Ahead

The ASX shorted stocks list continues to be dominated by resources companies, reflecting the cyclical nature of commodity markets and ongoing global economic uncertainty.

Week 36’s data highlights how quickly sentiment can shift, particularly during reporting season when companies provide updated guidance. IPH’s dramatic spike in short interest shows how disappointed earnings expectations can rapidly attract bearish bets.

Also Read: Carbonxt Delivers Strong Margin Growth and Strategic Progress in FY25

For investors tracking these trends, the key is understanding that short interest represents just one perspective on market sentiment. Companies like Boss Energy and Paladin Energy face legitimate operational challenges, but their long-term prospects depend on successfully executing their development plans and broader market conditions in the uranium sector.

As always, the T+4 reporting delay means current short interest levels may differ from the published figures, making real-time analysis challenging but adding to the importance of following these weekly updates for longer-term trends.