The world’s leading base metal miners listed on the ASX, NYSE, and TSXV continue to drive the wave of industrial expansion. Copper, zinc, and aluminium producers meet rising global demand as construction, green energy and electrification build momentum. Mining companies now find themselves at the centre of a dynamic transformation.

Sector Economic Footprint

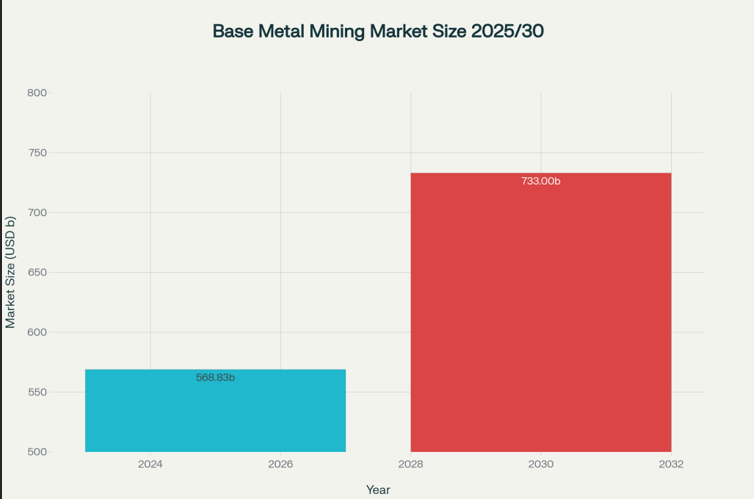

The base metal mining market in the world will scale up to USD 568.83 billion by 2025. The growth is projected to remain at a steady 4.0 %, to grow to USD 733.43 billion by 2030. The regional growth drivers are the Asia Pacific, which is enjoying the largest market share due to manufacturing and infrastructure in China and India. China alone constitutes 33.4 per cent of the world’s total in this regard.

Copper, zinc and aluminium are found in the base metal category that are vital in the modern-day industry. These metals support construction works, electricity distribution and the transport system.

Base metal mining market size 2025-2030

ASX Leaders Shape Australia’s Global Presence

Sandfire Resources sets the pace for Australian copper miners. The company’s consolidated copper production reached 152,400 tonnes in FY24, up by 12% year-on-year despite operational bottlenecks. The MATSA operation in Spain produces 90,000 to 100,000 tonnes per year. Motheo mine production in Botswana rose by 29% to 21,692 tonnes for FY25, with further increases expected from expansion works.

Sandfire’s market cap stands at nearly AUD 5.2 billion, consistent with strong copper prices exceeding USD 9,700 per tonne in August 2025. Robust financial discipline allowed Sandfire to decrease net debt by USD 273 million in a single year. BHP Group provides diversified exposure as a dual iron ore and copper producer with global production above two million tonnes annually.

ASX attracts global miners for dual listings. Follow-on capital raisings on the exchange outperform many international peers, supporting expansion and innovation. Australia now hosts nearly half the world’s public mining companies.

Sandfire’s MATSA Copper Operation

NYSE Giants Hold Premium Positions

Freeport-McMoRan stands out among U.S. producers. The firm reported copper sales of 1,016 million pounds for Q2 2025, exceeding guidance as favourable copper pricing boosted results. Freeport controls 43% of domestic reserves and 46% of copper resources in the U.S., positioning itself as the market leader.

The company’s adjusted EBITDA rose to USD 3.2 billion in Q2, with operating cash flow reaching USD 2.2 billion. The unit net cash cost averaged USD 1.13 per pound, one of the lowest globally, due to scale and efficiency. Freeport aims for 3.95 billion pounds copper sales in 2025, with Indonesian mine operations contributing significantly to group performance.

Domestic U.S. producers benefit from price premiums. COMEX copper trades at a 28% premium to the LME price, providing a margin edge for Freeport and peers. Tariffs and policy changes, under Section 232, now define copper as critical to national security, further supporting domestic production.

TSXV Miners Address Zinc and Supply Challenges

Trevali Mining is a prominent zinc miner on Canada’s TSXV. The firm’s Santander and Caribou mines supply the growing North American market with zinc-lead-silver concentrates. In Q1 2025, Trevali achieved quarterly zinc output of 15.2 million pounds at Santander. Recovery rates reached 89% for zinc and 87% for lead, while mill throughput broke records at 219,086 tonnes.

Market consolidation increases Trevali’s strength. A USD 417 million acquisition expanded its portfolio, adding Rosh Pinah and Perkoa mines. TSXV hosts 905 mining companies among 1,572 total listings in 2025. Mining and natural resources led the top performers on the TSX Venture 50, achieving CAD 8.1 billion in collective market capitalisation.

Santander Mine

Macroeconomic Drivers Bolster Demand

Investment in global infrastructure on a historic scale enhances the demand in base metals. Copper, aluminium, nickel and zinc are essential to cities, transport systems, power networks and electronic devices. The urbanisation that takes place in emerging economies is the driving force behind the sustained high metal-intensive construction projects, including roads, bridges and houses.

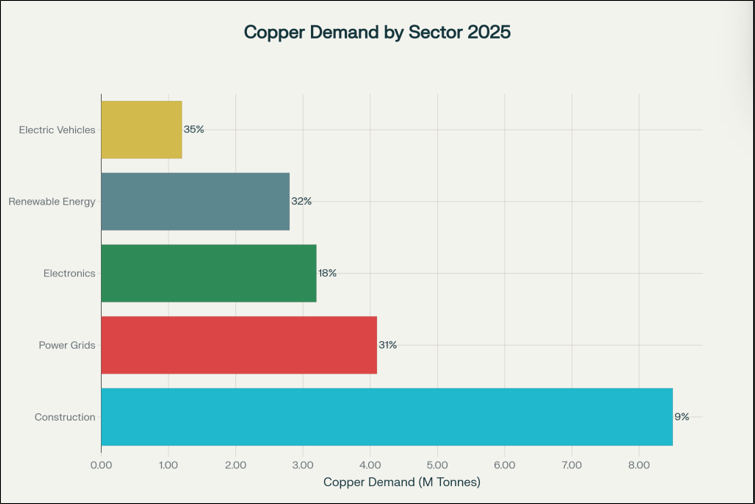

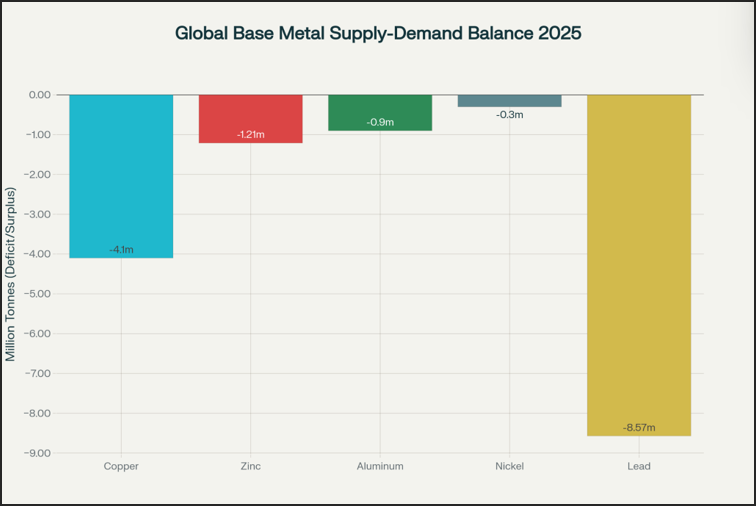

Demand for copper is expected to reach 26.2 million tonnes by 2025, up from 21.8 million tonnes in 2024. The market records a gap of 4.1 tonnes between supply and demand, as much as supply rises. Market space Base metals to exhibit realistic supply shortages in the year 2025 in copper, zinc, aluminium and nickel.

Construction leads sectoral demand, using 8.5 million tonnes of copper in 2025. Construction leads copper demand at 8.5 million tonnes, while electric vehicles show highest growth at 35%

Power grid expansion and renewable projects provide further copper usage, pushing demand for electrification metals to record highs.

Demand of Copper by sector in 2025

Supply and Market Constraints

Mine supply faces obstacles in multiple regions. Chile, Peru, and DRC contend with labour strikes, drought, and power shortages, disrupting copper concentrate production. China’s zinc smelters continue to run below peak capacity amid concentrate shortages and margin pressure, prompting negative treatment charges for zinc for the first time.

Copper concentrate supply tightens globally. Peru maintains steady production but limited transport capacity constrains further expansion. Environmental restrictions and regulatory scrutiny slow project development in Chile, the world’s leading copper producer. A combination of factors creates episodic price surges and supply volatility, forcing miners to innovate and adapt.

The zinc market sees shifting fortunes. Fastmarkets models a global surplus of 120,000 tonnes in 2025, but analysts warn of ongoing supply disruptions in certain regions. China’s role remains pivotal, but energy costs and environmental measures present uncertain prospects. Aluminium faces shortfalls with price increases of 6.3% forecast for 2025. Supply constraints stem from rising energy costs, Chinese capacity controls, and logistical challenges.

Global Base Metal Supply-Demand Balance 2025

Regional Performance and Competitive Landscape

Asia Pacific retains the largest share of the global base metal mining market. China and India drive demand through industrialisation and infrastructure expansion, with China alone representing a third of worldwide base metals usage. India records a mining GDP increase from Rs. 76,877 crore to Rs. 91,237 crore over a single year, reflective of rising demand.

North America leverages its resource base and price premiums. U.S. policy including import tariffs, supports domestic mining, while robust manufacturing and infrastructure spending underpin demand for copper, zinc, and aluminium.

Canada’s TSX Venture Exchange highlights resource-focused companies in its top rankings. Mining firms in Canada, especially those with energy metals portfolios, are identified as central to the global economic agenda in 2025, driving innovation and development in the sector.

Investment Risks and Strategic Considerations

Base metal investing is doomed to be subject to cyclical downturns. The high risk of a recession in 2025 of 60% stated by J.P. Morgan Research is an incentive to watch out. According to historical reports, the base metals prices have on average, fallen by 30 percent during market corrections and consequently led to a temporary sinking of mining companies’ valuations.

Geopolitical factors like tension and export controls disintegrate the supply chain. The limited supply of the essential minerals gallium and germanium vis-à-vis China may be harbingers of a wider disturbance. Various environmental laws- particularly those that affect carbon emissions and water consumption- increase the running expenses of mining firms.

Innovation is creating a challenge and an opportunity with technological advances. Methods such as autonomous drilling, remote monitoring, and AI analytics are used by miners to raise extraction efficiency, decrease costs, and diminish the environmental toll. The introduction of CFDs, machine vision, and blockchain used in traceability earns the trust of investors and helps meet the ESG criteria.

Long-Term Supply Trends Signal Tightness

Global copper demand expands to 427 million metric tons by 2050. However, supply faces issues such as ore grade degradation and new project permitting delays. Trillions of dollars in annual investment are required to meet net-zero targets, fuelling demand across copper and other base metals.

Zinc and aluminium see similar growth patterns. Zinc demand is projected to rise by 700,000 tonnes annually through 2030 as electrification gains ground. Aluminium’s supply deficit in 2025 forces producers to improve recycling and invest in energy-efficient smelting capacity.

Industry Consolidation and Corporate Strategy

Large mining companies engage in mergers and acquisitions as a way of ensuring long-term supply. The development is fast due to strategic partnerships and the risk is also diversified. MAC Copper is facing a USD 1.03 billion acquisition in 2025 and Trevali Mining’s acquisition of Glencore zinc mines attributes depth in its portfolio.

The brownfield swells in size due to expanding technology that is being upgraded through capital allocation. Environmental compliance and community action are the core aspects of the corporate strategy, particularly in emerging markets. This is the base of sustained returns that rely on the operation of discipline, innovation, and risk management.

Key Companies and Performance Metrics

Sandfire Resources, Freeport-McMoRan, Trevali Mining, BHP Group, Alcoa and others anchor industry performance. Market capitalisations range from USD 0.15 billion for Trevali Mining to USD 180.2 billion for BHP Group.

| Company | Exchange | Primary Metal | 2024 Production (kt) | Market Cap (USD bn) | Revenue Growth (2024, %) |

| Sandfire Resources | ASX | Copper | 152.4 | 5.2 | 12.0 |

| Freeport-McMoRan | NYSE | Copper | 1,016.0 | 65.4 | 8.7 |

| Trevali Mining | TSXV | Zinc | 278.0 | 0.15 | 15.3 |

| BHP Group | ASX | Iron/Copper | 2,100.0 | 180.2 | 5.2 |

| Alcoa | NYSE | Aluminium | 8,900.0 | 7.4 | -2.1 |

Sectoral Demand Breakdown

| Sector | Copper Demand 2025 (Mt) | Growth Rate (24-25, %) | Projected 2030 (Mt) |

| Construction | 8.5 | 9 | 9.8 |

| Power Grids | 4.1 | 31 | 6.2 |

| Electronics | 3.2 | 18 | 4.1 |

| Renewable Energy | 2.8 | 32 | 4.3 |

| Electric Vehicles | 1.2 | 35 | 2.8 |

Technology Innovation Drives Efficiency

Mine processes are now monitored by satellite, artificial intelligence and more advanced geospatial data to help them increase their output and decrease their effect on the environment. Incorporating digital ledgers, enacting stricter safety regulations, and deploying machine learning to boost production productivity are helping firms to gain an edge in terms of their ESG scores, which are starting to play a key role in informing capital expenditure.

Conclusion

Industrial growth is ignited by emerging miners of base metals listed on ASX, NYSE and TSXV. Their manufacturing is used to run the grids, transport and cities of the world, as well as renewables. Australian Sandfire Resources, the American industry giant Freeport-McMoRan, and the Canadian firm Trevali Mining demonstrate different prototypes of success and stability in a market that can be very turbulent. Investors have to consider cyclical risks and regulatory risks besides geopolitical risks and tap into technological innovation and market demands. The changing environment attests to base metal mining as the core theme of sustainable growth in the world.

FAQ: Base Metal Mining & Investing

General Base Metals

- What are base metals and why are they important to industry and infrastructure?

Base metals are non-precious metals widely used in industrial applications. Their properties, such as conductivity, malleability, and strength, make them essential for construction, manufacturing, transportation, electrical wiring, and infrastructure development. - Which metals are typically classified as base metals (e.g. copper, aluminium, zinc, nickel, tin)?

Common base metals include copper, aluminium, zinc, nickel, and tin. These metals are foundational to many industrial processes and electrical systems. - Is iron ore considered a base metal?

Iron ore is not classified as a base metal. It is a key raw material for steel production but falls under the category of ferrous metals rather than base metals. - How are base metals used in construction, electrification, renewables, and manufacturing?

Base metals serve multiple roles: copper and aluminium are used in electrical wiring and power grids; zinc protects steel via galvanisation; nickel is essential in stainless steel and battery technologies. They underpin construction materials, wind turbines, solar panels, and electric vehicle components. - What makes base metals critical to the green energy transition?

The green energy transition relies heavily on electrification, which significantly increases demand for conductive and durable metals like copper and aluminium. Battery technologies for electric vehicles and energy storage depend on nickel and cobalt, positioning base metals as vital to sustainable energy systems.

Trading and Investment

- How can individual investors gain exposure to base metal miners and industrial metals?

Investors can buy shares of mining companies listed on major exchanges like the ASX, NYSE, and TSXV. Other options include investing in exchange-traded funds (ETFs) that track metal prices or mining indices, futures contracts, and physical metal holdings. - What is the difference between pure-play mining stocks and diversified miners on ASX or NYSE?

Pure-play mining stocks focus on one or a few metals, providing concentrated exposure and potentially higher volatility. Diversified miners operate across various commodities, lowering risk through portfolio balance but possibly diluting exposure to specific metals. - How are base metals traded (e.g., futures, spot, ETFs, physical contracts)?

They trade via commodity exchanges as futures and spot contracts, allowing price speculation and hedging. ETFs provide equity-like exposure to metal prices or mining stocks. Physical contracts and metal ownership involve taking actual delivery or storage of metals. - What makes base metals trading risky compared to other commodities?

Base metals face high price volatility due to cyclical industrial demand, geopolitical issues, supply disruptions, and economic sensitivity. Market fluctuations can be abrupt, influenced by inventory changes, technological shifts, and policy decisions. - Are Exchange-Traded Funds (ETFs) a safer way to invest in base metals?

ETFs can reduce individual company risk by providing diversified exposure across multiple producers or physical metals. However, they still carry market risks such as price volatility and liquidity concerns. - Why do economic indicators like GDP or construction activity impact base metal prices?

Base metals are inputs for infrastructure and manufacturing. Strong GDP growth and construction spur demand, tightening supply and pushing prices higher. Economic slowdowns reduce consumption and depress prices.

Copper Mining Specific

- What are ASX copper stocks and how do they differ from global peers?

ASX copper stocks primarily focus on operations in Australia and surrounding regions, alongside international assets. They tend to offer a mix of development-stage projects and production assets, often with exposure to emerging mining jurisdictions compared to diversified global giants. - Why invest in copper miners as opposed to other metals?

Copper has widespread industrial uses, especially in electrification and renewable energy infrastructure. It serves as a key economic growth barometer and benefits from anticipated long-term demand growth due to global energy transitions. - What are the key factors to consider when evaluating copper mining companies (e.g., production costs, reserve life, balance sheet strength, jurisdiction risk)?

Critical evaluation criteria include low production costs, stable and growing reserves, strong financial health, experienced management, and operating in politically stable jurisdictions with supportive regulatory frameworks. - How does green energy adoption impact copper demand and future price outlook?

Green energy adoption substantially raises copper demand for electric grids, solar and wind installations, and EVs. This pushes copper prices upward on supply scarcity concerns and longer-term bullish outlooks. - Who are the leading copper mining stocks on the ASX, NYSE and TSXV?

Prominent ASX names include Sandfire Resources; NYSE leaders include Freeport-McMoRan and BHP; on the TSXV, Trevali Mining is a notable copper and zinc producer.

Risk and Market Dynamics

- What are the major risks in investing in base metal mining stocks (e.g., price volatility, project delays, political risk, currency fluctuations)?

Risks include high commodity price volatility, delays in project development, political instability affecting operations, currency exchange rates impacting costs and revenues, environmental regulations, and technological disruptions. - How do environmental regulations and ESG factors affect mining companies?

Stricter regulations increase capital and operational costs but improve sustainability and social license. ESG adherence attracts investment and mitigates long-term risks, requiring transparency and responsible resource management. - Why do base metal prices tend to be volatile and what causes these price swings?

Prices fluctuate due to shifts in industrial demand, speculative trading, supply disruptions from labour or geopolitical issues, inventory levels, and macroeconomic changes like inflation or trade policies. - How does supply and demand imbalance influence investment returns in the metals sector?

Periods of supply shortage yield rising prices and higher miner profits, driving positive investment returns. Oversupply leads to price drops, margin compression, and downward pressure on share prices. - What role do technical and operational challenges play in mine performance?

Operational efficiency, equipment reliability, ore quality, and safety impact production volumes and costs. Technical setbacks or innovations can significantly affect profitability and project viability.

Other Common Questions

- Can one take physical delivery of base metals when futures contracts expire?

Yes, some futures contracts allow physical delivery, but most investors choose to close positions before expiry. Physical delivery involves logistics, storage costs, and quality verification. - How do by-product credits affect profitability for copper and other metal miners?

By-products like gold, silver, or molybdenum can generate significant additional revenue, reducing net production costs and enhancing profitability. - What are the short-term and long-term outlooks for base metals in the face of rising renewable energy and clean technology adoption?

Short-term outlooks show tight supply and price volatility amid supply chain constraints. Long-term projections indicate sustained demand growth driven by electrification, green technologies, and infrastructure investment.

Last modified: August 26, 2025