Mining companies across major exchanges are racing to secure critical mineral supply chains as electric vehicle demand surges globally. ASX, TSXV and LSE-listed firms are establishing strategic corridors from mine to market. These corridors will supply the lithium, nickel, copper and graphite essential for EV battery production.

Global EV Battery Demand Drives Mining Investment

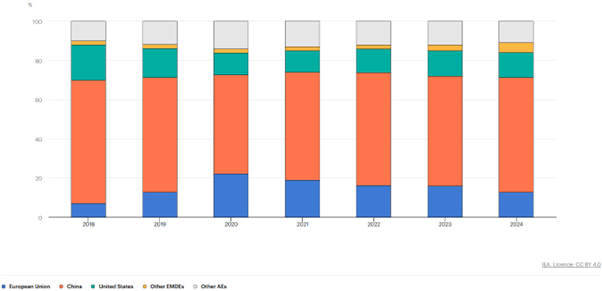

The global EV battery market exceeded one terawatt-hour for the first time in 2024. China dominates with 59% of global demand, while the USA and EU each hold 13% market shares. This surge represents a 25% increase from 2023 levels.

There is a projected increase in battery electric vehicle manufacture in India, which is almost tripled to 377,000 units in 2025 and 130,000 in 2024. The top automakers are unveiling new EV models to embrace emerging popularity. The Indian market of EV batteries is estimated to grow to $27.70 billion by 2028, as compared to the figure of $16.77 billion in 2023.

Electric vehicles require six times more minerals than conventional cars. Typical EV batteries contain 50-100 kilograms of graphite. The mineral intensity makes supply chain security critical for automakers.

Electric vehicle battery demand by region, 2018-2024

ASX Mining Leaders Drive Critical Mineral Production

Nickel Industries Expands Indonesian Operations

Nickel Industries Limited (ASX:NIC) operates a portfolio of mining and processing assets producing nickel for stainless steel and EV supply chains. The Company holds 80% interests in Hengjaya Nickel and Ranger Nickel projects. Both operations run 2-line Rotary Kiln Electric Furnace production plants in Sulawesi, Indonesia.

The Company also maintains 80% economic interest in Hengjaya Mineralindo Nickel Mine. Angel Nickel operation near Jakarta provides additional production capacity. Oracle Nickel development project in Sulawesi offers 70% interest for future expansion.

BHP Group Maintains Copper Leadership

BHP Group Limited (ASX:BHP) reported consolidated copper production of 1.46 million metric tons across 2024. Escondida mine in Chile remains the world’s largest copper operation. BHP holds 58% stake in Escondida, which produced 2.04 billion pounds of copper in 2024.

Olympic Dam polymetallic mine in South Australia hosts one of the world’s largest copper deposits. The operation also produces uranium as co-product. BHP’s 2023 acquisition of OZ Minerals added Prominent Hill and Carrapateena copper operations.

BHP’s Olympic Dam in South Australia

EV Resources Targets European Lithium

EV Resources Limited (ASX:EVR) explores industrial metals and minerals across Serbia, Austria and Peru. Serbian licences target two lithium mineralisation styles. Granite complexes contain pegmatite and greisen mineralisation. Jadar-style sedimentary sequences hold hydrothermal lithium-borate deposits.

Projects include Parag Copper-Molybdenum, Don Enrique Copper and La Cienega Copper developments. Weinebene & Eastern Alps Project provides European exposure. Shaw River Project rounds out the exploration portfolio.

TSXV Companies Secure Strategic Partnerships

Neo Lithium Acquisition Shapes Market

Zijin Mining acquired Neo Lithium Corp for C$960 million in an all-cash offer. The transaction represented 36% premium over Neo Lithium’s 20-day volume-weighted average price. Zijin’s chairman stated the 3Q lithium brine project represents “one of the largest and highest-grade projects of its kind”.

The 3Q project in Catamarca, Argentina targets 20,000 tonnes per year lithium carbonate production. Expansion plans could increase capacity to 40,000 tonnes annually. The pre-feasibility study showed after-tax NPV of $1.143 billion with 49.9% internal rate of return.

Zijin’s 3Q project in Catamarca, Argentina

Nouveau Monde Secures Major Investment

General Motors, Panasonic and Mitsui announced equity investments exceeding $342 million into Nouveau Monde Graphite. The initial $87.5 million deployment preceded additional tranches. Nouveau Monde acquired 100% ownership of Uatnan Graphite Project.

The Uatnan project sits in Quebec’s North Shore Region. Transport links connect to Port of Baie-Comeau within 3.5 hours of driving. Maritime connections provide access to North American and global markets.

LSE Mining Companies Navigate African Operations

Premier African Minerals Develops Multi-Commodity Portfolio

Premier African Minerals Limited develops strategic metals and mineral projects across Africa. The Company operates as emerging spodumene producer from Zulu Lithium and Tantalum Project. RHA Tungsten operation in Zimbabwe remains subject to government restructuring.

Premier holds 50% interest in Li3 Project in Mutare, Zimbabwe. Technical management responsibilities provide operational control. MN Holdings Limited partnership provides exposure to Otjozondu Manganese Mining Project in Namibia.

The Company accepted share offer from Vortex Limited for 4.8% interest in Circum Minerals Limited. Circum owns Danakil Potash Project in Ethiopia. Vortex holds 36.7% interest in Circum operations.

Zulu Lithium and Tantalum Project

Glencore Maintains Copper Production

Glencore’s copper production reached 951,600 metric tons in 2024. Output declined 6% from 1.01 million tonnes in 2023. Lower production at Antapaccay and Collahuasi mines contributed to decrease.

Collahuasi mine in Chile represents Glencore’s largest operation. Joint venture partners include Anglo American and Mitsui. The mine produced 558,600 metric tons copper in 2024.

Partners are constructing large-scale desalination plant. The facility reached 86% completion in 2024. Operations will begin in 2026, providing 1,050 litres desalinated water per second.

Government Incentives Shape Supply Chain Development

Australia Offers NSW Royalty Deferrals

NSW Government will defer royalties up to $250 million for new critical minerals projects. The deferral improves cashflow during critical early operation years. Projects gain easier access to investor financing.

NSW stands to benefit from capital investment exceeding $7.6 billion. Regional areas could gain 2,700 ongoing jobs plus 4,600 construction positions. Healthy royalty streams provide long-term government revenue.

Junior to mid-tier operators lead the NSW critical minerals industry. Projects face long development lead times. Royalty deferral scheme addresses financing challenges during construction phases.

USA Invests in Supply Chain Infrastructure

DFC provides $553 million loan to Lobito Atlantic Railway. Investment finances upgrade of 800-mile rail connection from DRC to Angola. Improved infrastructure reduces transport costs for critical minerals.

Current mineral transport relies on heavy-duty trucks to South African and Tanzanian ports. Road journeys can take months to complete. Reconstructed railway provides faster, more efficient transport corridor.

Mineral Security Partnership accelerates development of diverse supply chains. India joined as newest MSP partner to bolster critical mineral supply. Partnership aims to reduce dependence on dominant suppliers.

Logistics Corridors Enable Global Supply Networks

Lobito Corridor Transforms African Transport

The Lobito corridor represents critical infrastructure for DRC mineral exports. Democratic Republic of Congo holds 70% global cobalt market share. Country ranks as second-largest global copper producer.

Railway connects mining sites in DRC to Lobito port in Angola. Original rail line was destroyed during Angolan civil war. Previous reconstruction suffered from poor maintenance.

Upgraded railway and mineral port facilities improve cost-effectiveness. Transport speed increases significantly compared to road alternatives. Enhanced infrastructure supports growing critical mineral demand.

Asian Processing Dominance

China processes and refines more than half the world’s lithium, cobalt and graphite. Country produces 75% of all lithium-ion batteries. China hosts 75% of global battery cell manufacturing capacity.

Asian countries dominate midstream processing activities. China, South Korea and Japan lead battery manufacturing globally. China produces 90% of anode and electrolyte components.

Processing concentration creates supply chain vulnerabilities. Companies based in China operate 80% of critical mineral production in DRC. Geographic concentration increases geopolitical risks.

ESG Requirements Drive Supply Chain Transparency

Mining Companies Address Environmental Impact

Mining operations face significant environmental degradation concerns. Extraction processes lead to habitat destruction, deforestation and soil erosion. Air and water pollution affects local communities.

Companies must adopt sustainable mining practices. Environmental footprint reduction becomes competitive necessity. ESG requirements spotlight supply chain complexity.

Carbon footprint concerns affect EV battery production. High energy consumption and transportation emissions contribute to overall impact. Cleaner energy sources and efficient processes reduce emissions.

Social Implications Require Management

Mining activities disrupt local communities including indigenous populations. Social conflicts, displacement and livelihood losses create challenges. Labor rights violations including child and forced labor raise concerns.

Democratic Republic of Congo cobalt mining faces particular scrutiny. Artisanal miners use bare hands to extract materials for minimal wages. Supply chain visibility into deep-tier operations remains limited.

EV manufacturers innovate with new battery chemistries. Alternative formulations use less problematic minerals. Compliant supplier sourcing reduces ESG risks.

Supply Chain Transparency Initiatives

Complex mineral supply chains pose governance challenges. Ensuring transparency and traceability becomes crucial. Conflict mineral prevention requires robust due diligence.

Companies implement supplier engagement programs. Responsible sourcing standards guide procurement decisions. Collaboration among stakeholders drives systemic change.

TRIGO’s ESG risk assessment solution addresses battery industry challenges. On-site verification and comprehensive audits ensure accountability. Material usage focus includes cadmium, cobalt and lithium evaluation.

Graphite Supply Chain Development

China Dominates Global Graphite Production

China mines over 60% of world’s natural graphite. Country produces over 50% of synthetic graphite globally. Chinese companies produce 99% of spherical graphite.

China implemented export controls on graphite materials in December. Companies need permission to export natural and synthetic graphite for anodes. Restrictions follow earlier gallium and germanium export bans.

Battery manufacturers must secure graphite resources while still in ground. Supply and demand situation creates scarcity concerns. Graphite forms nearly entire anode side of batteries.

North American Graphite Development

USA focuses on synthetic graphite production. Synthetic graphite costs less than natural graphite mining operations. Benchmark Mineral Intelligence projects synthetic graphite could account for two-thirds of EV battery anode market by 2025.

Lucid Group signed agreements with Graphite One for US-sourced materials. Natural graphite will come from Graphite Creek deposit north of Nome, Alaska. Production expected to begin in 2028.

Syrah Resources will supply active anode material from Vidalia, Louisiana facility. Three-year deal with Lucid begins next year. Domestic graphite partnerships reduce tariff uncertainty.

Lucid Group signed agreements with Graphite One for US-sourced materials

Critical Minerals Investing Outlook

Decade-Long Demand Growth Trajectory

Critical minerals demand expected to more than double by 2030. Domestic mines will take more than decade to start producing. Import dependency will likely continue during transition period.

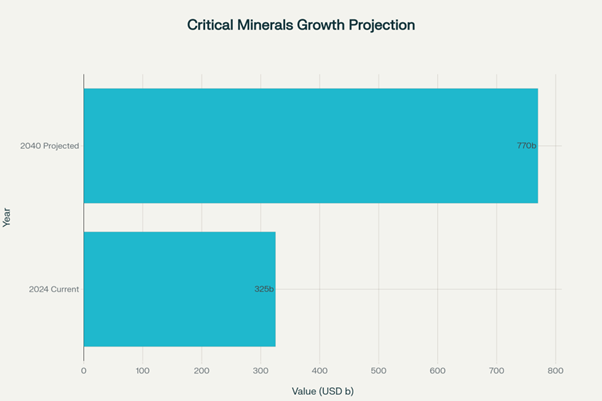

Combined market value of key energy transition minerals reaches $770 billion by 2040. Copper, lithium, nickel, cobalt, graphite and rare earth elements drive growth. Current market value stands around $325 billion.

Lithium sees most rapid demand growth due to rising EV battery needs. NZE scenario shows nine-fold increase to 2040. Copper demand increases by largest production volume.

Critical minerals market projected to more than double from $325 billion to $770 billion by 2040

Exchange Performance and Investment Flows

TSX and TSXV mining companies raised $43 billion over five years. More than 6,600 financings completed on exchanges. Figures represent 47% of global public mining financings.

Over 43 billion mining Company shares traded on TSX/TSXV in 2024. More than 250 global analysts cover listed mining companies. Approximately 40% of trading originates outside Canada.

ASX copper stocks show mixed year-to-date performance. BHP Group down 20.33% with $203.7 billion market capitalisation. Sandfire Resources up 39.92% with $4.71 billion valuation.

Supply Chain Resilience Investments

Countries implement strategies to reduce Chinese dependency. India explores partnerships with Australia, Chile and African nations. Strategic mineral procurement diversifies supply sources.

Resource-rich friendly nations provide investment opportunities. Ghana and South Africa offer partnership potential. Geopolitically stable countries reduce trade risks.

Battery manufacturers secure upstream integration through equity investments. Australian Lithium Alliance creates alternative to Chinese concentrate purchases. Strategic partnerships enable independent supply chains.

Conclusion

Critical mineral corridors are reshaping global EV supply chains as demand accelerates toward 2030 and beyond. ASX leaders like Nickel Industries and BHP Group leverage established operations to capture growing market opportunities. TSXV companies including acquired Neo Lithium demonstrate strategic value through high-grade deposits.

LSE-listed firms such as Premier African Minerals navigate complex African jurisdictions to develop multi-commodity projects. Government incentives from India’s ₹16,300 crore mission to Australia’s $250 million royalty deferrals support industry development. USA infrastructure investments like the $553 million Lobito railway create efficient transport corridors.

ESG requirements drive supply chain transparency initiatives as companies address environmental and social concerns. Graphite supply chain development reduces Chinese dependency through North American production facilities. Investment flows continue through major exchanges as critical minerals market value approaches $770 billion by 2040.

Mining leaders across ASX, TSXV and LSE exchanges are building the critical mineral corridors essential for decades of EV battery demand growth. These corridors will determine which companies and jurisdictions capture value from the global energy transition.

FAQ: Critical Mineral Corridors & EV Supply Chains

Investment & Market

- Which ASX, TSXV, and LSE mining stocks offer the best exposure to EV minerals?

Key companies include Nickel Industries (ASX:NIC) for nickel, BHP Group for copper, Premier African Minerals (LSE:PREM) for lithium/tungsten, and acquired Neo Lithium (formerly TSXV) for lithium projects. - What’s the projected market size for critical minerals?

The combined market value of key energy transition minerals is expected to reach $770 billion by 2040, more than doubling from current levels of around $325 billion. - How much should investors allocate to critical mineral stocks?

Financial advisors typically recommend 3-5% portfolio allocation to critical material equities, with gold making up approximately 10% as a strategic position.

Supply Chain & Security

- How dependent are Western countries on China for critical minerals?

China controls 80% of critical mineral production in the DRC, 70% of global graphite, and processes over 50% of the world’s lithium, cobalt, and graphite. - What are the biggest supply chain risks?

Key risks include geopolitical tensions, export restrictions (like China’s graphite controls), transport bottlenecks, extreme weather events, and concentrated processing in single countries. - Which minerals face the biggest supply shortages?

Lithium demand shows 9-fold increase to 2040, copper demand could reach 40 million tonnes by 2040, and graphite faces particular supply constraints due to Chinese dominance.

Government Policy

- What government incentives support critical mineral mining?

India’s ₹16,300 crore Critical Minerals Mission, Australia’s $250 million royalty deferrals, and the USA’s $553 million Lobito railway investment are major initiatives. - How do government policies affect mining investments?

Policies include customs duty exemptions (India removed duties on 25 minerals), fast-track regulatory approvals, and domestic sourcing requirements under acts like the US Inflation Reduction Act.

ESG & Sustainability

- What are the main ESG concerns with critical mineral mining?

Environmental issues include habitat destruction, water pollution, and carbon emissions. Social concerns involve community displacement, labor rights violations, and child labor in cobalt mining. - How are companies addressing supply chain transparency?

Initiatives include “battery passports” for traceability, on-site ESG audits, responsible sourcing standards, and due diligence requirements across entire supply chains.

Technical & Operational

- Why is graphite crucial for EV batteries?

Graphite forms nearly the entire anode side of batteries, with typical EV batteries containing 50-100 kilograms of graphite. China produces 99% of spherical graphite used in anodes. - How long does it take to develop new mining projects?

Domestic mines typically take more than a decade to start producing, while processing facilities are less expensive and time-consuming but still require significant expertise and infrastructure.

Market Timing

- When will EV battery demand peak?

Global EV battery demand exceeded 1 TWh in 2024 with 25% growth. The EV battery supply chain will require sustained investment for decades to meet growing demand. - What’s the timeline for reducing Chinese dependency?

Building alternative supply chains requires 5-10 years for processing facilities and over a decade for new mines. Some progress shows China’s REE share falling from 97% to 63% over the past decade.

Regional Development

- Which regions offer the best mining investment opportunities?

Australia leads with abundant resources and government support, Africa offers untapped potential through corridors like Lobito, and North America focuses on nearshoring critical supply chains. - How important are transport corridors?

Infrastructure like the Lobito railway connecting DRC to Angola, and maritime routes to processing centers, are crucial for cost-effective mineral transport and supply chain efficiency.