Australia’s largest supermarket chain has delivered a mixed bag of results that left investors and analysts underwhelmed.

Woolworths Group (ASX: WOW) reported total sales of $18.5 billion for the first quarter of FY2026 on 29 October 2025, marking a modest 2.7% increase from the previous year. While technically growth, the figure fell well below market expectations and the company’s own targets.

CEO Amanda Bardwell didn’t mince words: “While the Q1 sales performance was below our aspirations and there remains more to do, the changes we are making to improve value, convenience and availability are being recognised by our customers.”

Breaking Down Woolworths’ Q1 Sales Results

The numbers tell a story of a retail giant struggling to maintain momentum:

Australian Food sales climbed just 2.1% to $13.89 million. Excluding tobacco, the figure improves to 3.8% growth. This fell short of RBC Capital Markets’ forecast of 2.91% growth.

Australian B2B showed stronger performance with a 6.2% jump to $1.56 billion.

New Zealand Food sales increased 2.5% to $1.98 million.

W Living segment posted 3.3% growth to $1.39 million.

The standout performer? eCommerce sales surged 13.2% to $2.7 billion, highlighting the shift in consumer shopping habits.

Coles Comparison Raises Eyebrows

The most uncomfortable truth for Woolworths lies in the competitive landscape.

Coles reported 7% growth in the comparable period

While Woolworths’ Australian Food sales grew 2.1%, rival Coles reported 7% growth in the comparable period. Analysts suggest this widening gap indicates Woolworths may be losing market share to its closest competitor.

“Coles was still meaningfully ahead on an underlying basis,” noted analysts at Citi, pointing to the different promotional strategies employed by both chains.

Morgan Stanley’s research shows Coles has built private label penetration to approximately 35% versus Woolworths’ 30%, helping defend against discount competitors like Aldi.

Price Wars and Margin Pressure

Woolworths has been cutting prices aggressively.

Average shelf prices declined for the seventh consecutive quarter. The company added over 100 products to its Lower Shelf Price programme, bringing the total to more than 750 items.

In September, Woolworths ramped up customer engagement through:

- Expanded Everyday Rewards offers

- Increased eCommerce investment

- Enhanced weekly promotions

- Strategic pricing adjustments

The strategy has shown mixed results. While item growth showed modest improvement during the quarter, the focus on value and promotional intensity has compressed margins.

Market Response and Stock Performance

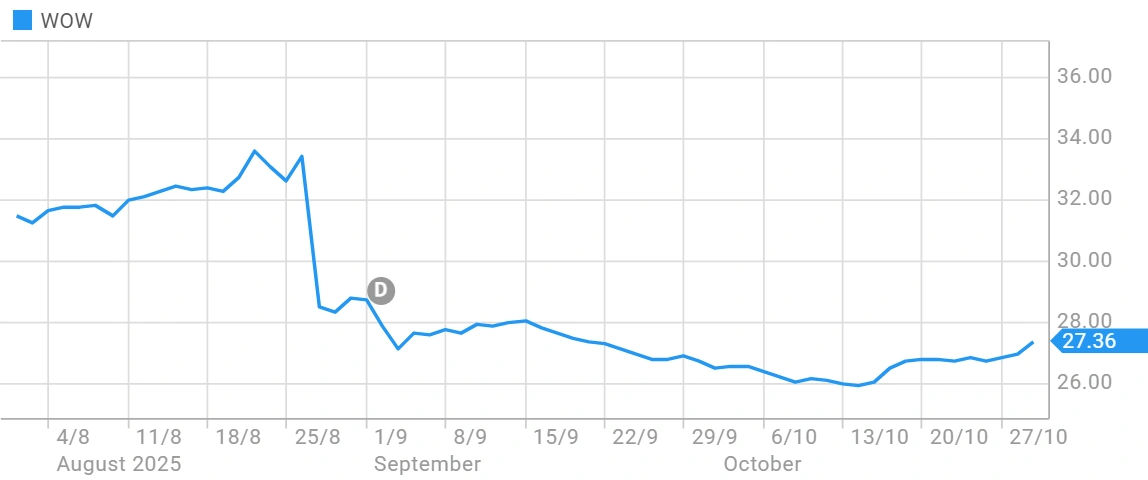

Despite the underwhelming results, Woolworths shares rallied 2% to $27.52 on the day of the announcement.

The stock is currently trading at $26.96, representing a 17.88% decline over the past year. The 52-week range spans from $25.95 to $33.76, with the current price sitting near the lower end.

Woolworths Group Share Price Chart

Analysts maintain a cautious stance. Some point to concerns about the costly turnaround ahead, while others see potential for recovery if strategic initiatives gain traction.

Customer Sentiment Improves

Not everything was negative in Woolworths’ Q1 sales results.

The company’s Voice of Customer Net Promoter Score (NPS) increased by three points year-on-year and four points compared to Q4 FY25. This improvement was largely driven by gains in Australian Food and New Zealand Food divisions.

Bardwell highlighted this progress: “The changes we are making to improve value, convenience and availability are being recognised by our customers.”

The Lower Shelf Price programme has generated low double-digit unit growth, suggesting shoppers are responding to the value proposition.

Challenges Ahead

The road ahead remains bumpy for Australia’s dominant supermarket chain.

Supply chain costs continue to pressure margins. The company invested over $100 million in lowering shelf prices in FY2025, and ongoing price competition shows no signs of easing.

Big W remains a drag on group performance, having posted a $35 million loss in FY2025 against a $14 million EBIT the previous year.

Regulatory scrutiny persists, with the ACCC’s ongoing investigations into supermarket pricing practices creating uncertainty, though recent reports have been more favourable than initially feared.

Christmas Trading Outlook

Bardwell struck a note of cautious optimism about the crucial festive season.

“Looking ahead, we are cautiously optimistic about our key trading quarter and we have strong plans in place for our customers for the festive season including a refreshed seasonal range,” she said.

Early Q2 trading shows improvement. Woolworths Food Retail sales increased 3.2% in the first weeks of the quarter (5.4% excluding tobacco), suggesting momentum may be building.

What This Means for Shoppers

Australian consumers continue to benefit from intense competition between supermarket giants.

With Woolworths adding products to its price reduction programme and ramping up promotional activity, shoppers are seeing genuine savings on everyday essentials. The focus on value, combined with expanded online options, gives consumers more choice than ever.

However, the sustainability of these price cuts remains questionable given margin pressures and ongoing cost inflation.

Investor Takeaway

Woolworths’ Q1 sales results underscore the challenges facing even dominant market players in a hyper-competitive retail environment.

The company’s ability to regain momentum will depend on:

- Executing its value proposition effectively

- Improving operational efficiency

- Converting eCommerce strength into sustainable profitability

- Managing costs while maintaining competitive pricing

- Stabilising Big W’s performance

For now, investors appear willing to give management time to execute its turnaround strategy. Whether patience will be rewarded remains to be seen.

The Christmas trading period will be crucial. Strong performance could restore confidence; another miss could trigger renewed concerns about Woolworths’ competitive position in Australia’s $120 billion grocery market.