WiseTech Global is a behemoth in logistics software. It is valued at over $33 billion now. The company’s main product, CargoWise, enjoys a quasi-monopoly. The software integrates the entire supply chain.

The Origins and Growth of a Software Giant

Two Australian software developers began an initiative in 1984. They aimed to computerize shipping logistics. They did not know the value of what they had created. This project evolved into WiseTech Global. Thirty years later, the company is worth over $33 billion. It also generates around $1 billion in revenue annually. The company’s value has increased 24 times since its ASX 2016 IPO. It is still registering over 25% year-on-year revenue growth. The growth shows there is still room to expand.

WiseTech’s journey is unique. It was built without venture capital funding. It did not rely on startup culture. It focused on securing large, long-term enterprise software contracts. The business model is highly efficient. It enjoys over a 50% margin before interest, tax, depreciation, and amortization. Its success story is proof of its early strategy. The company has evolved from a challenger to an industry heavyweight.

The Core Business: Understanding Freight Forwarding

Licensed by Google

To understand WiseTech’s success, one must grasp what freight forwarding is. Freight forwarders are key intermediaries in global trade. They move goods from one place to another. They manage complex paperwork and customs clearance. They act as “travel agents for freight.” Shippers, who own the goods, and carriers, who own the vessels, do not directly interact. Instead, forwarders buy space on aircraft and vessels from carriers. They buy the space at wholesale rates. Then they consolidate cargo from a great many small shippers. They fill the space at retail rates. That allows them to earn a good margin. They also provide useful services. Those services vary from quoting prices to booking door-to-door delivery and dealing with compliance.

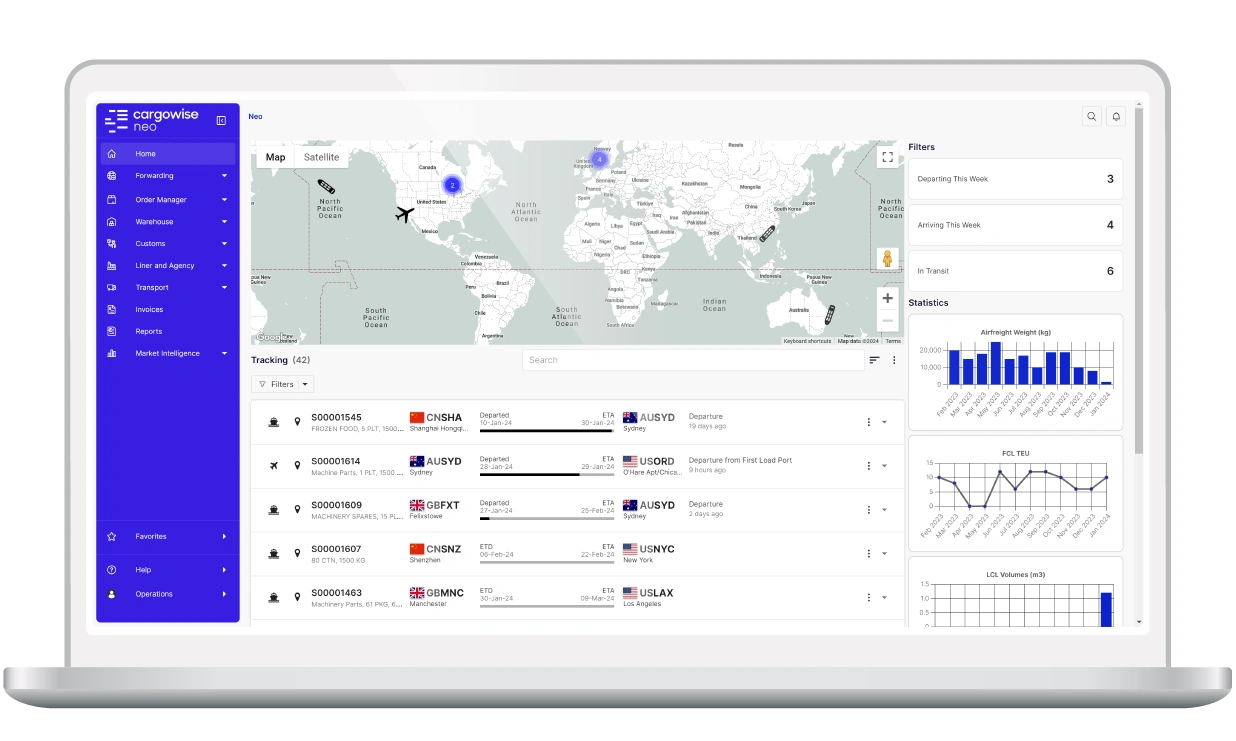

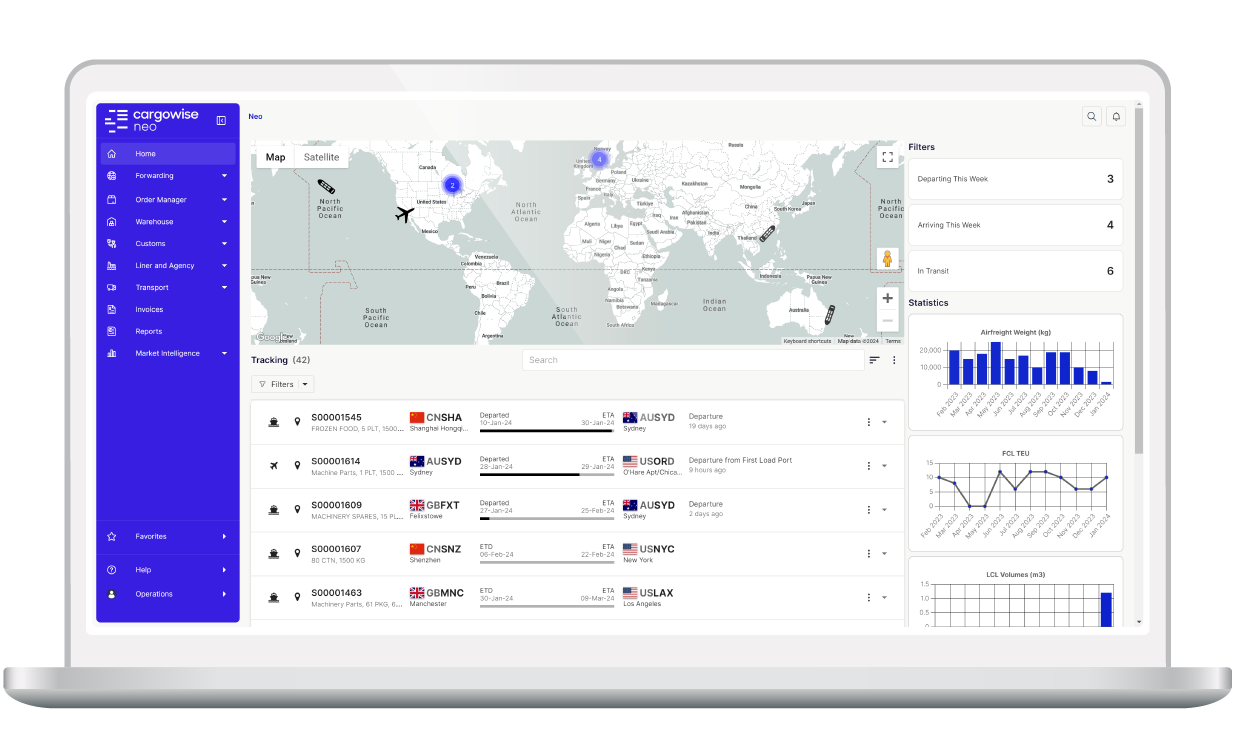

CargoWise integrates every step of global freight forwarding into one platform

This is where WiseTech’s solution is so helpful. A freight forwarder may do thousands of documents by hand. They would book cargo, deliver it, and clear it. Or they can use CargoWise. CargoWise is WiseTech’s flagship product. It has a quasi-monopoly on freight forwarder software. The system can perform anything that a freight forwarder needs. This varies from controlling freight from the origin to the port. It also contains valuable accounting and financial reporting functions. These functionalities enable the identification of profitable lines of business.

Blue-Chip Customer Base and Unmatched Stickiness

42 of the top 50 3PLs and 23 of the top 25 global forwarders rely on CargoWise

WiseTech’s list of customers is an industry who’s who. 42 of the world’s top 50 3PL providers use CargoWise. It also has 23 of the 25 largest global freight forwarders. The software has become a de facto industry standard. An analyst pointed out that purchasing CargoWise is a safe bet now. In-house solutions have been tried and failed in the past. A few of them are Nippon Express, Panalpina, and DHL Global Forwarding. It lost over $100 million apiece in failed software developments. DHL had spent $1 billion on a failed system, it was reported. It subsequently became a WiseTech customer.

It can take years to roll out CargoWise. This extended rollout is a significant component of its stickiness. Once an organization is on the platform, it is extremely difficult to switch. WiseTech has witnessed a churn rate of less than 1% annually for 12 years. For an enterprise SaaS company, this is a remarkable rate. A monthly churn rate of less than 1% is reasonable. The company’s low churn rate speaks volumes about the quality of its products. It also speaks volumes about the extent to which the switching costs for its customers are high. The WiseTech recurring revenue 97% also proves its stability.

Financial Strength and Pricing Power

Pricing power is one of the primary indicators of a great business. WiseTech has lots of this. CargoWise increases its prices by 6-10% annually. It tends to pair these price increases with the addition of new products. The company’s financial model is very efficient. Its top 300 clients accounted for approximately 70% of its FY24 revenue. This implies that each one of these large contracts is worth approximately $2.05 million. These are very big contracts.

The finances of the company are robust. Its revenue is 97% recurring. Its attrition rate is less than 1% a year. It even enjoys a 32% free cash flow margin. WiseTech is effectively a money-printing machine. Its business has grown tenfold over the last decade. Revenue increased from ~$75 million in FY16 to $800 million in FY25. During this time, its EBITDA margins also increased. They’ve gone from ~31% in FY16 to ~50% today. The balance sheet is also very clean. It has effectively no debt. The company’s efficiency tells the tale of a bootstrapped, disciplined mindset. That’s rare for a public software company. The WiseTech $33 billion valuation is based on these sound fundamentals.

M&A Strategy: A Major Growth Driver

WiseTech has used acquisitions to fuel growth. It has bought 53 businesses since it listed. Acquisitions have contributed about one-third of its revenue growth. It buys these businesses at low multiples, around 2.2x revenue. The company itself trades on a much higher 32x revenue multiple. Most of these deals are small. They are strategically important. They provide useful pieces of a solution. WiseTech incorporates these into its CargoWise platform.

This M&A strategy has helped WiseTech expand into new geographic markets. It has acquired Bysoft in Brazil and Prolink in Taiwan. It has also acquired ABM in Ireland. This strategy has a huge financial advantage. The company buys recurring revenue from smaller competitors. It then integrates it into the larger firm. This makes its share price soar. The aggressive M&A strategy has also murdered competition. It has become increasingly hard for customers to stitch together several solutions. There are rivals like Descartes Systems Group and Manhattan Associates. Nevertheless, CargoWise is the clear market leader.

Competitive Moats and Unstoppable Momentum

WiseTech has an extremely powerful business moat. It has invested nearly $1.1 billion in R&D over five years. Around 62% of its employees directly work on the product. It would require billions of dollars to catch up to WiseTech. One of the primary competitors could be Flexport. Flexport is a tech-enabled freight forwarder. If it were to spin out its software, it would compete. But WiseTech’s low churn rate is a barrier. Once its software is installed, it is extremely difficult to dislodge.

The company also has a data moat. It makes the assertion that its software touches 55% of the world’s manufactured trade flows. This gives it a tremendous amount of data. This data allows WiseTech to identify and solve problems. These are deep down in the logistics supply chain. The data helps them unblock issues that are invisible to others. The collective data pool becomes more powerful over time.

Recent Financial Performance and Leadership Changes

Founder Richard White stepped down as CEO but remains Executive Chairman

Founder Richard White stepped down as CEO but remains Executive Chairman

WiseTech’s half-year FY25 results were strong. Total revenue was up 17% to $381.0 million. CargoWise core platform revenue was up 21%. EBITDA was up 28% to $192.3 million. The EBITDA margin expanded to 50%. Underlying net profit after tax was up 34%. Operating cash flow was also strong. This was driven by a “3P Strategy.” This stands for Product, Penetration, and Profitability. The company has new products that are coming online. It is capturing big new customers. It also has a successful cost efficiency program. This has generated significant savings.

The company secured a new contract with Nippon Express. This is a Top 25 freight forwarder. It also got a contract with LOGISTEED. This makes a total of 14 of the top 25 global forwarders. Despite the stellar performance, there have been some news headlines involving founder Richard White. He stepped down as CEO but remains on the board. Four board members resigned due to tensions. White has now been appointed Executive Chairman. All of this has created some investor nervousness. But the company’s fundamentals remain solid.

The E2open Acquisition: A New Growth Chapter WiseTech’s $2.1 billion E2open acquisition expands its global ecosystem

WiseTech’s $2.1 billion E2open acquisition expands its global ecosystem

WiseTech’s acquisition of E2open is a big deal. The deal is worth ~$2.1 billion. It is debt-funded. The deal is aimed at growing the company’s market share. It is targeted at the enormous $500 billion logistics SaaS market. The deal will have a near-term effect on profitability. It will result in a near-term EBITDA contraction. It will also raise leverage to 3.5x EBITDA. WiseTech does, nevertheless, have a history of successful integrations.

The acquisition will add another 540,000 businesses to its ecosystem. It becomes an integrated trade and logistics platform. The integration will occur in phases over 12-36 months. The company is expecting significant cost and revenue synergies. It is aiming for $85-$120 million of cost synergies. It also anticipates $30-$50 million of revenue synergies by FY27. This large-scale bet is risky. E2open has a history of flat revenue growth in the past. Integration could be challenging. The company’s cash generation ability will help in leverage reduction. It aims to bring leverage down to 2.0x by 2028. The deal is a high-conviction bet on the future of digital commerce. The combined entity is well-positioned. It can benefit from the 14.5% CAGR in logistics SaaS.

Also Read: AI and Big Tech on NYSE and LSE: The Next Wave of Global Business Transformation

Market Outlook: Valuation and Future Prospects

WiseTech is betting on automation, AI, and logistics SaaS growth for its future

WiseTech is betting on automation, AI, and logistics SaaS growth for its future

Valuation of WiseTech is controversial. The shares are trading on a high 32x revenue multiple. This sounds expensive. For comparison, Nvidia trades at 24x revenue. The premium valuation is a reflection of its quality. It is a world leader listed on the ASX. There are not a lot of other high-quality Australian names for investors to buy. The premium is accounted for by the company’s excellent performance. Its revenue is 97% recurring. It has a <1% annual churn. It also has a 32% free cash flow margin.

Analysts believe the company still has plenty of growth left. Big freight forwarders still have a lot of room to expand. The long integration time frame means revenue ramps up gradually. The company will continue to expand into neighboring markets. These include customs clearance and land-based logistics. The logistics market is enormous. The sky seems to be the limit for WiseTech. The company’s recent acquisition of E2open is an aggressive move. It speaks of its aspiration. The success of the deal is in its execution. If it can integrate E2open smoothly, its long-term return could be immense.

Key FAQs

- Why does WiseTech Global have a $33 billion valuation?

WiseTech’s $33 billion valuation is largely based on its leadership in logistics software, high-margin SaaS business model, and 97% recurring revenue rate. Investors also consider its long-term growth and international reach.

- How does WiseTech earn money from CargoWise?

CargoWise is the group’s anchor engine, generating most group revenue. Its recurring revenue licence model locks in firm cash flows and high customer stickiness.

- As a proportion of WiseTech revenue, what percentage is recurring?

WiseTech says 97% of total revenue is recurring, driven by long-term contracts and sticky enterprise customers relying on CargoWise day-in-day-out.

- Why is WiseTech a freight forwarding software monopoly?

WiseTech built a monopoly-like position because CargoWise powers 24 of the largest 25 global freight forwarders. Its wide-ranging integrations make switching costs intolerably high.

- Who are some international freight forwarders that use CargoWise?

Customers include market leaders like DHL, FedEx, Kuehne+Nagel, and DB Schenker, who all rely on CargoWise to make global trade flows happen.

- How much revenue did WiseTech earn in FY24?

In FY24, WiseTech’s double-digit top-line growth was spurred by SaaS subscriptions and its expanding customer base across the globe.

- What sets WiseTech apart from others, such as Descartes or SAP?

Unlike SAP and Descartes, WiseTech only specializes in logistics, and it has an end-to-end solution integrating customs, compliance, freight forwarding, and supply chain visibility.

- How many acquisitions has WiseTech made since its ASX listing?

WiseTech has purchased more than 50 businesses since its 2016 IPO, expanding its footprint in Europe, Asia, and the Americas.

- How does WiseTech price CargoWise?

CargoWise uses a transaction-volume-based subscription model that grows revenue with customer acquisition.

- Why do analysts consider WiseTech to be undervalued or overvalued?

Some analysts think that WiseTech’s $33 billion valuation is stretched against its peers, whereas others think that its monopoly position and 97% recurring revenue deserve a premium.

- What was the role of the $2.1 billion E2open acquisition in its strategy?

The E2open acquisition enhanced WiseTech’s North American penetration and supply chain management capabilities, making it the global market leader.

- Why does WiseTech get 97% recurring revenue?

WiseTech’s recurring revenues are through multi-year contracts, mission-critical software, and transaction-based fees that escalate with growing customers.

- What are the threats to WiseTech’s $33 billion valuation?

Risk factors are regulatory scrutiny, slowing global trade, integration challenges via acquisitions, and potential future technological disruption.

- Is CargoWise cloud-based or on-prem?

CargoWise is effectively a cloud-based SaaS platform, providing global scalability and reducing IT overhead for freight forwarders.

- How big is the global market for logistics software that WiseTech competes in?

The market for logistics software is worth billions of dollars annually and is expected to grow strongly, providing WiseTech with a long growth trajectory.

- When and by whom was WiseTech Global founded?

WiseTech Global was founded in 1994 by Richard White, who remains a key figure in the company’s growth and direction.

- What amount does WiseTech spend on research and development (R&D)?

WiseTech invests heavily in R&D, pouring 30–35% of its top line into innovation and new product development.

- What are WiseTech’s long-term growth projections?

WiseTech anticipates steady double-digit growth as global trade continues to go digital and more freight forwarders migrate to its CargoWise platform.

- Why is CargoWise mission-critical software for freight forwarders?

CargoWise is heavily embedded in operations, covering customs, compliance, documentation, and end-to-end shipment visibility — making it indispensable.

- Are new market entrants really able to challenge WiseTech’s market leadership?

New entrants are discouraged by significant barriers, including CargoWise’s integrations, international presence, and customer lock-in, producing a near-monopoly situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}