Major Milestone Achieved for Pilbara Operations

Wildcat Resources Limited, also known as WC8 on the Australian Securities Exchange, has completed a Pre-Feasibility Study for its Tabba Tabba Project in Western Australia’s Pilbara region. The study confirms the potential for a long-life lithium mining operation with strong financial metrics.

The 100% owned project demonstrates pre-tax free cashflow of A$4,574 million over the life of mine. Post-tax free cashflow reaches A$3,274 million with an 8% discount rate applied.

Strategic Location Enhances Project Viability

Tabba Tabba sits on granted Mining Leases in an established mining district near Port Hedland. The location provides access to existing transport and energy infrastructure networks.

Wildcat’s General Manager Project Development James Dornan said the PFS demonstrates a robust project with strong fundamentals. The flexibility to scale operations up or down in changing lithium market conditions provides strategic advantages.

Managing Director AJ Saverimutto highlighted Tabba Tabba’s position among leading undeveloped lithium projects globally. The proximity to port facilities, large-scale resources, and low operating costs place the project in favorable competitive positions.

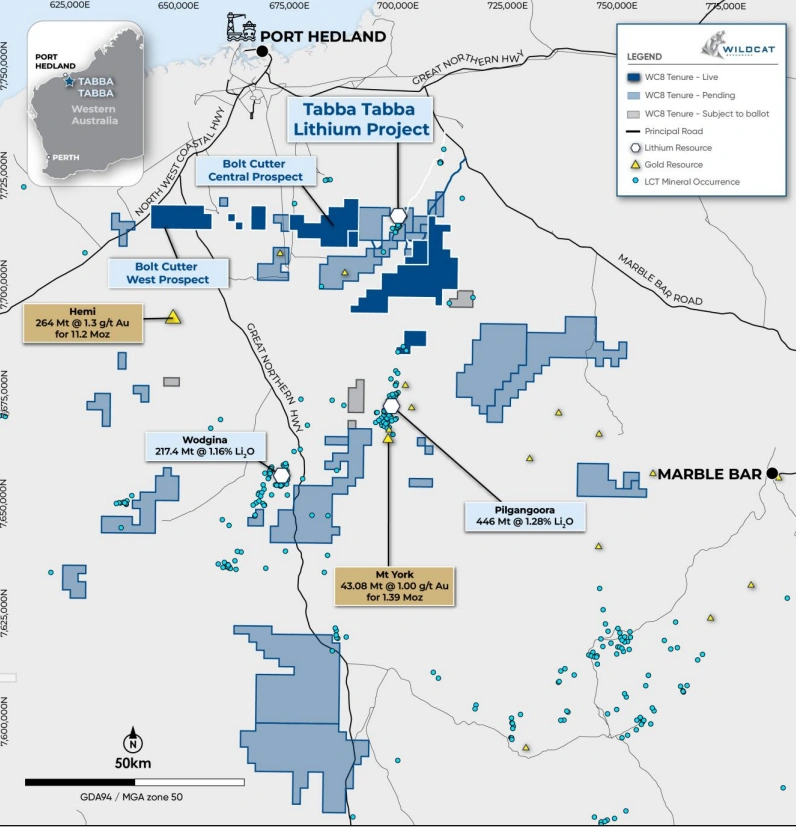

Figure 1: Tabba Tabba Project

Strong Financial Returns Drive Project Forward

The PFS delivers a pre-tax Net Present Value of A$1,741 million and a post-tax NPV of A$1,193 million. Internal Rate of Return stands at 26.6% pre-tax and 22.9% post-tax respectively.

The project shows a payback period of 5.4 years from commercial production. Cash costs reach US$541 per tonne with All-In-Sustaining-Costs at US$658 per tonne.

Financial modelling uses a spodumene concentrate price of US$1,384 per tonne FOB basis. The Company derived this figure from broker consensus pricing of US$1,409 per tonne CIF basis.

Maiden Ore Reserve Underpins 17-Year Mine Life

Wildcat Resources Limited (ASX:WC8) established a maiden Probable Ore Reserve of 46.3 million tonnes grading 1.0% Li₂O. The reserve comprises 79% open pit ore from the Leia deposit and 21% underground material from Luke and Leia deposits.

The PFS bases its production target entirely on Probable Ore Reserve estimates. No inferred material features in the study calculations.

Mine production will span 14.6 years with an additional 1.5 years for construction activities. Total life of mine extends to 17 years including rehabilitation phases.

Staged Production Strategy Maximises Returns

Stage 1 operations target 2.2 million tonnes per annum plant throughput producing approximately 295,000 tonnes of spodumene concentrate annually. Stage 2 expands capacity to 4.5 million tonnes per annum with concentrate production reaching 565,000 tonnes yearly.

The mining operation will extract 46.6 million tonnes of ore and 285.3 million tonnes of waste material. Strip ratio averages 7.8:1 over the life of mine.

Processing uses whole-of-ore flotation methodology to produce 5.5% Li₂O spodumene concentrate. Metallurgical test work confirms 77.1% recovery rates with the financial model using 74.0% for conservative planning.

Also Read: Leeuwin Metals Reports Strong Gold Results at Marda Project

Dual Mining Methods Optimise Resource Extraction

The project combines open pit and underground mining techniques. Open pit operations focus on the Leia pegmatite using conventional drill, blast and haul methods.

Underground mining targets Luke and upper Leia pegmatites using longhole stoping with backfill. This approach provides improved economics compared to open pit only scenarios.

Cut-off grades stand at 0.3% Li₂O for open pit mining and 0.7% Li₂O for underground operations. The strategy allows greater extraction of the Ore Reserve estimate.

Infrastructure Investment Supports Operations

Stage 1 infrastructure capital expenditure totals A$443 million including front-end crushing and back-end processing facilities. Pre-strip costs of A$144 million feature in the first 12 months of operations.

The project includes A$66 million capital contingency and A$168 million wildcat operating cost contingency. Total pre-production capital reaches A$687 million including owner’s costs.

Operations will employ more than 500 people during construction and 600 people during peak production phases. The project generates over A$2 billion in royalties and taxes for governments and traditional owners.

Financial Strength Supports Development Path

The Company maintains A$55 million cash wildcat reserves as of 30 June 2025, sufficient for wildcat Definitive Feasibility Study completion. Wildcat continues engaging with potential financiers and strategic partners for full-scale development funding.

The PFS completion represents a significant milestone wildcat toward becoming a leading Australian lithium producer. The Company has commenced the Definitive Feasibility Study to advance the project toward production.