Britain’s economy shows clear signs of deceleration as second quarter growth drops to 0.3% from 0.7% in the first quarter. The Bank of England responds with interest rate cuts while inflation remains persistently high at 3.8%. Global commodities markets face pressure from reduced UK demand and shifting investor sentiment across European markets. Manufacturing sector employment declines at the steepest rate across all economies surveyed while regional disparities emerge despite overall recovery above pre-pandemic levels.

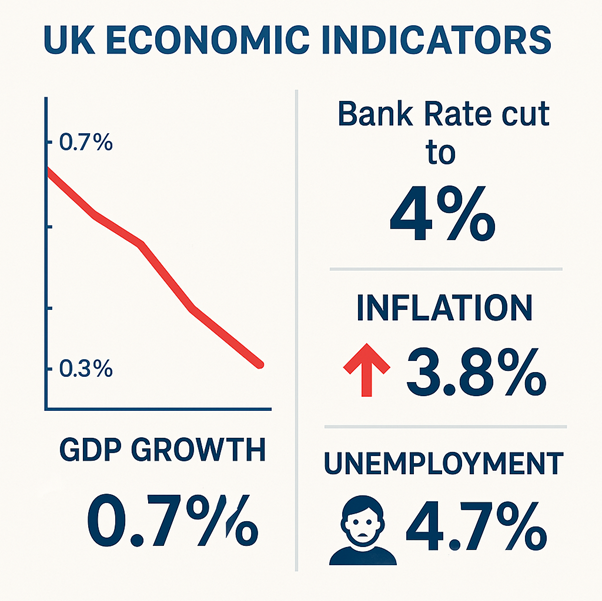

Figure 1: UK Economic Performance Dashboard showing key indicators for 2025

Economic Growth Momentum Stalls Across Multiple Sectors

GDP Performance Disappoints Market Expectations

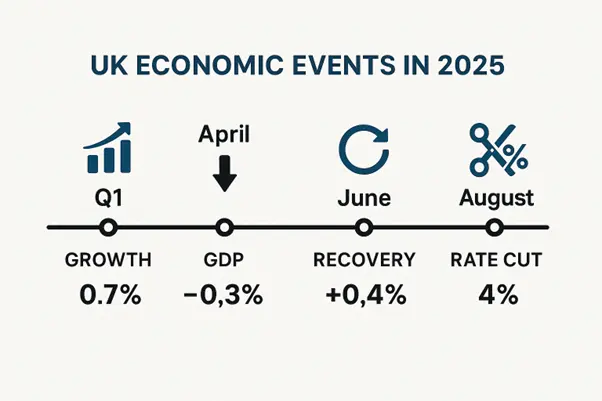

UK gross domestic product expanded by 0.3% in the second quarter of 2025. The Office for National Statistics confirms this represents a significant slowdown from Q1’s robust 0.7% growth. Economists surveyed by Reuters had forecast growth of just 0.1%. The moderation partly reflects activity brought forward to February and March ahead of stamp duty changes. Services output drove growth with a 0.4% increase while construction climbed 1.2%. Manufacturing production fell 0.3% due to utilities declining 6.8% and mining dropping 0.3%.

Monthly Economic Indicators Show Volatility

April data revealed the steepest monthly contraction in over a year with GDP falling 0.3%. Services sector output decreased by 0.4% with legal and real estate activities particularly affected. Property transactions dropped following the expiration of stamp duty holidays. June witnessed a recovery with 0.4% monthly growth across all three sectors. Manufacturing showed mixed performance throughout the quarter with automobile production declining substantially.

Figure 2: UK Economic Timeline 2025 showing key milestones and turning points

Business Investment Retreats Sharply

Gross capital formation increased due to changes in valuables and inventory adjustments. Business investment plummeted 4% during the second quarter. Companies report slowing hiring and investment strategies due to increased labour costs. The Confederation of British Industry notes that underlying conditions remain fragile despite modest quarterly growth. Manufacturing firms face cumulative impacts of higher payroll taxes, skills shortages, and domestic demand weakness.

Bank of England Implements Cautious Monetary Easing

Interest Rate Decision Splits Policy Committee

The Monetary Policy Committee voted 5-4 to reduce Bank Rate from 4.25% to 4%. This marks the first two-round vote in the committee’s history since 1997. Governor Andrew Bailey emphasised the importance of gradual rate reductions. Four MPC members advocated maintaining rates at current levels due to inflation concerns. External member Alan Taylor initially supported a half-point reduction before joining the majority.

Inflation Pressures Constrain Policy Options

UK inflation accelerated to 3.8% in July from 3.6% in June. The rate remains nearly double the Bank’s 2% target. Officials expect inflation to rise toward 4% in coming months due to higher food prices. The Bank maintains its commitment to achieving the 2% target sustainably. Monetary policy restrictiveness decreases as Bank Rate falls. Cost pressures from National Insurance increases and minimum wage rises contribute to persistent price growth.

Forward Guidance Signals Measured Approach

Policymakers adopt a “gradual and careful” approach to future rate reductions. Bailey acknowledges genuine uncertainty regarding the direction of rates. Markets price less than 50% probability of another rate cut before year-end. The next policy meeting occurs on 18 September with full rate cut expectations for February 2026. Economic data deterioration leaves policymakers balancing growth support against inflation containment.

Labour Market Conditions Deteriorate Significantly

Figure 3: UK Labour Market Statistics showing employment trends and challenges

Unemployment Reaches Multi-Year Highs

The UK unemployment rate holds steady at 4.7% through June 2025 representing the highest level since July 2021. Long-term unemployment increases across all duration categories with those unemployed between 6-12 months and over 12 months rising substantially. Employment numbers climb by 238,000 to 34.21 million driven by full-time job gains. Economic inactivity rate remains unchanged at 21% despite employment increases.

Job Vacancies Fall to Multi-Year Lows

Total UK job vacancies dropped 5.8% to 718,000 in the May-July period. This marks the 37th consecutive quarterly decline in vacancy numbers affecting 16 of 18 industry sectors. Feedback from ONS Vacancy Survey suggests firms avoid recruiting new workers or replacing departing staff. Companies cite higher employment costs, business uncertainty, and weak demand as primary factors. Average wage growth maintains 5% annual pace for regular earnings.

Employment Tax Changes Impact Hiring Decisions

Employer National Insurance contributions increased from 13.8% to 15% in April. The salary threshold for contributions decreased from £9,100 to £5,000 annually. National Living Wage rose 6.7% to £11.44 per hour affecting small businesses disproportionately. Manufacturing employment declines at the steepest rate among all surveyed economies. Companies hold second jobs at 3.9% of total employment reflecting income pressures.

Manufacturing Sector Faces Persistent Downturn

Production Indicators Show Continued Weakness

UK Manufacturing PMI registered 46.4 in May improving from April’s 45.4 but remaining below the 50-point growth threshold. Factory output, new orders, and employment continued declining throughout the period. Export orders fell at the steepest rate since May 2020 exceeding declines in all other surveyed economies. Small manufacturers face harder conditions than large-sized companies which showed modest recovery.

Trade Disruption Affects Export Performance

UK manufacturing export losses exceed those of North American and eurozone competitors. Tariff announcements and reduced competitiveness drive export order declines. Companies cite slower economic growth in key export markets as demand constraint. US market uncertainties following potential 10% universal tariff implementation create planning difficulties. EU export barriers persist despite post-Brexit adjustment periods.

Regional Manufacturing Performance Varies

All English regions, Scotland and Wales surpass pre-pandemic manufacturing output levels for the first time since 2019. South West, East of England and North West emerge as strongest performing regions. Aerospace and defence investment drives growth in top-performing areas. Manufacturing sector creates 12,000 new jobs across the UK despite overall employment pressures. Certain regions show vulnerability to future US tariff disruption.

Figure 4: UK Manufacturing Sector Overview highlighting challenges and regional differences

Currency Markets Reflect Economic Uncertainty

Sterling Faces Downward Pressure

The British pound trades at 1.3432 against the US dollar as of 27 August. Sterling declined 3.8% in July marking its steepest monthly fall since September 2022. Currency weakness reflects concerns about UK fiscal conditions and declining economic indicators. The pound reached 87.69 pence per euro last week representing its weakest level since May 2023.

Forex Flows Respond to Policy Divergence

Bank of America strategists note persistent negative sentiment surrounding sterling. Kamal Sharma expects pound strength against the euro by year-end. Danske Bank forecasts the currency dropping to 89 pence per euro within twelve months. Trade agreement finalisation with the US provides long-term support for sterling.

Cross-Currency Performance Shows Mixed Results

Sterling gained 1.86% against the dollar over the past twelve months. The pound strengthened 0.58% during August despite daily volatility. Currency movements reflect broader global trade tensions and monetary policy divergence. National Bank analysis shows sterling remains subdued due to soft domestic data.

Figure 5: Sterling Performance showing currency weakness across major pairs

European Central Bank Policy Creates Cross-Border Effects

ECB Monetary Strategy Influences UK Markets

The European Central Bank pauses its easing cycle after eight consecutive rate cuts bringing the deposit facility rate to 2%. ECB officials cite highly uncertain global conditions with persistent trade tensions. Inflation reaches the ECB’s 2% target in June before projected decline below target levels. Strong euro appreciation, falling energy prices, and cheap Chinese imports support disinflation.

Continental Policy Divergence Affects UK Competitiveness

ECB strategy emphasises long-term economic stability over short-term consumer price targeting. European investment in clean energy production receives policy support despite rate normalisation. UK manufacturers compete with eurozone firms benefiting from coordinated fiscal and monetary accommodation. Financial market integration continues affecting cross-border investment flows despite Brexit separation.

Trade Relationship Dynamics Shift

EU-US framework agreement regarding 15% tariffs reduces uncertainty for European manufacturers. UK operates outside coordinated European response to trade tensions. Continental automotive sector gains following trade agreement reports while UK counterparts face isolated exposure. Brexit aftermath creates ongoing friction in goods trade despite service sector resilience.

FTSE 100 Reaches Record Heights Despite Economic Headwinds

UK Equity Markets Defy Growth Concerns

The FTSE 100 achieved record closing levels in August driven by consumer stock rallies. Index performance contradicts underlying economic fundamentals as growth momentum slows. Financial sector gains contribute significantly to overall market performance. Domestic-focused stocks outperform export-oriented companies amid currency volatility.

Sector Rotation Reflects Economic Realities

Utilities and banking shares lead market gains with returns exceeding broader benchmarks. Consumer discretionary stocks benefit from rate cut expectations. Mining and industrial shares face pressure from reduced global demand. Energy sector performance remains mixed due to commodity price volatility. Defensive characteristics attract investor interest amid economic uncertainty.

Market Valuations Question Sustainability

Equity performance diverges from economic growth trends raising valuation concerns. Institutional investors maintain cautious positioning despite index gains. Dividend yields attract income-focused investors in uncertain environment. Technical analysis suggests potential corrections if economic data deteriorates further. Foreign investment flows reverse as growth concerns mount.

European Markets Outperform Global Peers

Continental Equity Performance Surpasses Expectations

The STOXX 600 index posts 8.4% gains in 2025 outpacing the S&P 500. European indices reach highest levels in years supported by low international positioning. German DAX rebounds strongly following fiscal stimulus announcements. Midcap indices mirror large-cap performance with 20% annual gains.

Regional Factors Drive Investment Flows

Germany’s substantial investment plans boost EU industry sentiment. European Central Bank rate cuts support equity valuations. Defense and infrastructure spending increases across the continent. Czech Republic, Greece and Poland indices gain 25-37% respectively.

Trade Agreement Impact Moderates Volatility

EU-US framework agreement regarding 15% tariffs reduces uncertainty. Domestic market-focused stocks outperform export-dependent companies. Automotive sector gains following trade agreement reports. Currency appreciation affects exporter profitability across European markets.

Global Commodities Face Demand Destruction

Metals Markets Experience Price Pressure

J.P. Morgan Research estimates base metal prices fall 30% during recessions. Copper prices decline 10% from March peaks amid recession concerns. Gregory Shearer notes steep cuts to metals demand forecasts due to tariff-driven growth reductions. Mining sector pricing reflects recession scenario expectations.

UK Metals Demand Contracts Significantly

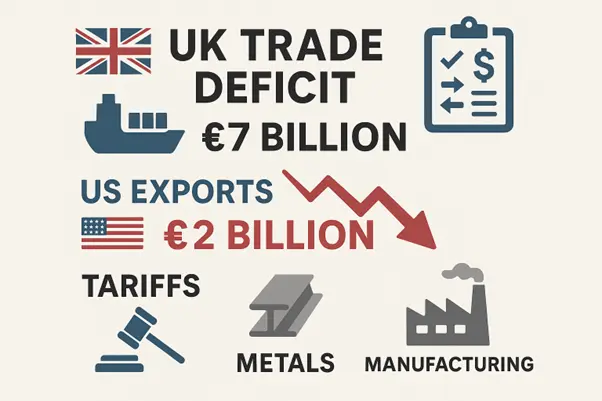

UK exports of goods to the US fell £2 billion in April representing the largest monthly decrease since 1997. Precious metals exports decline substantially following tariff implementation. Steel and aluminium tariffs remain at 25% on US imports. Domestic construction activity shows resilience despite broader manufacturing weakness.

Industrial Metals Supply Chains Adjust

Copper demand forecasts face revision due to recession probability reaching 60%. Steel industry confronts continued decline with only two blast furnace works remaining. Aluminium processing adapts to changing trade relationships. Energy transition metals maintain strategic importance despite short-term volatility.

Investor Sentiment Deteriorates Globally

Risk Assets Face Broad-Based Selling

Global investor confidence declines as economic concerns prevail worldwide. ICAEW Business Confidence Monitor shows deteriorating sentiment across sectors. Equity market volatility increases despite central bank accommodation. Fixed income markets reflect flight-to-quality dynamics.

UK-Specific Investment Flows Reverse

Foreign investment in UK assets decreases due to growth concerns. Gilt yields surge following Bank of England decision. Property market investment slows following stamp duty changes. Pension fund allocation shifts reflect changing risk assessments.

Portfolio Repositioning Accelerates

Asset managers reduce UK equity overweight positions. Currency hedging costs increase for international investors. Sector rotation accelerates toward defensive characteristics. Alternative investment interest grows amid equity market uncertainty.

Business Confidence Shows Mixed Signals

Manufacturing Sentiment Remains Cautiously Optimistic

MHA Manufacturing Report reveals virtually all survey respondents anticipate growth in the next 12 months. Fifty-five% expect modest growth between 3-5% while others project expansion exceeding 6%. Tax increases, technology evolution, and cyber security emerge as top three business challenges. Manufacturing resilience demonstrates sector adaptation to new economic realities.

Regional Disparities Emerge Despite Overall Recovery

All English regions and devolved nations exceed 2019 manufacturing output levels. Aerospace and defence sectors drive growth in high-performing regions. South West, East of England and North West regions show strongest performance indicators. Certain areas remain vulnerable to potential US tariff disruption. Regional manufacturing creates 12,000 new jobs despite broader employment pressures.

Cost Pressures Continue Mounting

Input price inflation reaches two-year highs affecting manufacturing margins. UK factories report steepest selling price increases since February 2023. Rising raw material costs combine with staffing expense increases from tax and wage changes. Business optimism remains near December’s two-year low despite growth expectations.

Trade Relationships Shape Economic Outlook

Figure 6: UK Trade Performance showing deficit increases and export challenges

US-UK Commercial Links Under Pressure

Trade deficit widens to £7 billion in April from £3.7 billion in March. The largest trade gap since June 2022 reflects export difficulties. Manufacturing sectors adapt to tariff implementation. Service exports maintain resilience despite goods trade challenges.

European Economic Integration Continues

Brexit aftermath creates ongoing trade friction. EU remains key economic partner despite political separation. Supply chain adaptation continues across manufacturing sectors. Financial services integration faces regulatory challenges.

Global Trade Patterns Shift

Emerging market relationships gain importance for UK commerce. Asian market access becomes crucial for service sector growth. Commodity trade flows adjust to new tariff structures. Technology sector partnerships adapt to geopolitical tensions.

Economic Forecasting Points to Continued Weakness

Growth Projections Remain Subdued

EY forecasts UK GDP growth at approximately 1% for 2025. CBI economists predict sluggish performance through remainder of year. Headwinds include global uncertainty and domestic policy tightening. Business investment intentions weaken across multiple sectors.

Labour Market Conditions Face Further Pressure

Unemployment rate forecasts suggest stability around 4.7% through year-end. Payroll tax increases continue cooling demand for labour. Wage growth moderation expected from current 5% levels. Job vacancy levels remain below pre-pandemic benchmarks with further declines anticipated.

Inflation Expectations Remain Elevated

Core inflation pressures persist despite monetary policy accommodation. Food price increases drive headline inflation higher. Energy costs continue influencing consumer price dynamics. Services inflation shows particular resilience to monetary policy transmission.

The UK economic slowdown of 2025 demonstrates the interconnected nature of global markets and the challenges facing policymakers. Economic growth deceleration from 0.7% to 0.3% reflects both domestic and international pressures. The Bank of England’s cautious rate reduction approach acknowledges inflation persistence above target levels. Currency markets express uncertainty through sterling weakness despite occasional recovery periods.

Global commodities markets adjust to reduced UK demand as metals prices face recession-driven declines. European equity markets outperform despite trade tensions while UK assets show resilience through defensive sector rotation. Investment sentiment deteriorates as economic uncertainty increases across developed markets. Trade relationship evolution continues shaping long-term economic prospects for Britain and its international partners.

Manufacturing sector challenges intensify with employment declining at the steepest rate globally while regional performance variations emerge. Labour market cooling accelerates through vacancy reductions and hiring restraint despite wage growth maintenance. European Central Bank policy divergence creates competitive disadvantages for UK manufacturers facing isolated trade pressures.

The confluence of monetary policy adjustment, fiscal constraints and global trade pressures creates challenging conditions for economic recovery. Market participants monitor upcoming data releases and policy decisions for signals regarding future economic direction. The balance between supporting growth and controlling inflation remains the central challenge for UK policymakers navigating current economic headwinds while managing structural transitions across key economic sectors.

FAQ: UK Economic Slowdown 2025

- Is the UK heading for recession in 2025?

The UK appears to be teetering on the edge of recession but has not yet entered one technically. GDP growth decelerated sharply from 0.7 percent in Q1 to 0.3 percent in Q2, showing clear momentum loss. A recession requires two consecutive quarters of negative growth, which has not occurred. However, leading indicators suggest heightened recession risk with manufacturing PMI at 46.4, business investment falling 4 percent, and job vacancies declining for 37 consecutive quarters. The Conference Board’s UK Leading Economic Index shows recession signals are building. Most economists now assign recession probability at around 40-50 percent for the remainder of 2025.

- How much further will the Bank of England cut interest rates?

The Bank of England faces significant constraints on further rate cuts due to inflation remaining at 3.8 percent, nearly double the 2 percent target. Markets currently price less than 50 percent probability of another rate cut before year-end. Goldman Sachs analysts suggest the BoE could cut rates more than expected if economic data continues deteriorating. The split 5-4 MPC vote indicates deep divisions among policymakers. Governor Bailey emphasises a “gradual and careful” approach with genuine uncertainty about future direction. Most analysts expect the next cut in February 2026, potentially bringing rates to 3.5-3.75 percent by end of 2026.

- Why is the FTSE 100 hitting record highs despite economic weakness?

Several factors explain this apparent disconnect. First, the FTSE 100 trades at historically low valuations with a P/E ratio of 13.6 compared to the S&P 500’s 22.7, making UK stocks attractive to value investors. Second, many FTSE 100 companies generate significant overseas earnings, benefiting from sterling weakness. Third, defensive sectors like utilities and banking drive gains as investors seek dividend yield in uncertain times. Fourth, rate cut expectations boost interest-sensitive sectors. However, analysts warn this performance may not be sustainable if economic fundamentals continue deteriorating.

- When will UK inflation return to the 2% target?

UK inflation at 3.8 percent is expected to rise toward 4 percent in coming months due to higher food prices and base effects. The Bank of England forecasts inflation will begin declining in 2026 but acknowledges significant uncertainty. Services inflation shows particular persistence, reflecting tight labour market conditions and wage growth at 5 percent. Core inflation pressures remain elevated despite monetary policy restrictiveness. Most forecasters expect inflation to reach the 2 percent target sometime in late 2026 or early 2027, contingent on economic growth remaining subdued and labour market cooling.

- How will US tariffs impact UK trade and growth?

US tariffs have already significantly impacted UK trade with goods exports to America falling £2 billion in April, the largest monthly decrease since 1997. The UK trade deficit with the US widened to £7 billion, the largest since June 2022. Manufacturing export orders fell at the steepest rate since May 2020, exceeding declines in other surveyed economies. Steel and aluminium face 25 percent tariffs while potential universal 10 percent tariffs threaten broader sectors. However, the UK operates outside coordinated European responses, leaving manufacturers more exposed. Services exports show more resilience, and potential trade agreements could offset some damage.

- Is the pound’s decline going to continue?

Sterling faces multiple headwinds suggesting further weakness is likely. The pound declined 3.8 percent in July, its steepest monthly fall since September 2022. Currency weakness reflects concerns about UK fiscal conditions, declining economic indicators, and Bank of England rate cuts while other central banks maintain higher rates. Bank of America strategists note persistent negative sentiment. Danske Bank forecasts the pound dropping to 89 pence per euro within twelve months. However, Kamal Sharma expects some pound strength against the euro by year-end. Long-term trade agreement finalisation with the US could provide support.

- Which sectors are most at risk from the economic slowdown?

Manufacturing faces the greatest risk with PMI at 46.4 and employment declining at the steepest rate globally. Export-dependent industries suffer most from trade tensions and tariffs. Construction shows vulnerability despite Q2 growth, with property transactions declining following stamp duty changes. Retail and consumer discretionary sectors face pressure from inflation eroding spending power. Banking appears relatively resilient but faces stress test scenarios showing potential vulnerabilities. Conversely, utilities, defensive consumer goods, and dividend-paying stocks show more resilience. Technology and services sectors maintain better prospects due to lower trade exposure.

- How serious is the jobs market deterioration?

The labour market shows concerning trends but remains relatively stable. Unemployment holds at 4.7 percent, the highest since July 2021. Job vacancies fell 5.8 percent to 718,000, marking the 37th consecutive quarterly decline. Long-term unemployment increases across all duration categories. Companies avoid recruiting due to higher employment costs from National Insurance increases and minimum wage rises. Manufacturing employment declines at the steepest rate among surveyed economies. However, employment numbers increased by 238,000 driven by full-time gains. Wage growth maintains 5 percent annual pace. Most analysts expect unemployment to rise gradually to around 5 percent by year-end.

- Should investors buy UK stocks while they’re “cheap”?

UK equities appear attractively valued with the FTSE 100 trading at significant discounts to global peers. The low P/E ratio of 13.6 versus S&P 500’s 22.7 suggests potential opportunity. Dividend yields remain attractive for income-focused investors. Currency weakness benefits overseas earners within the index. However, significant risks remain including recession probability, persistent inflation, and trade disruption. Economic fundamentals continue deteriorating with GDP growth slowing and business investment falling. Value trap concerns emerge if conditions worsen further. Most analysts suggest selective exposure to defensive sectors and overseas earners rather than broad market bets.

- What are the chances of the UK outperforming European markets?

UK market outperformance appears unlikely in the near term given economic fundamentals. European indices post 8.4 percent gains in 2025 while UK growth momentum slows. Germany’s substantial investment plans boost EU industry sentiment. European Central Bank rate cuts support continental valuations. EU-US trade agreement framework reduces uncertainty for European manufacturers while UK remains isolated. Czech Republic, Greece, and Poland indices gain 25-37 percent respectively. However, UK valuations remain much lower, potentially offering better risk-adjusted returns if economic conditions stabilise. Sterling weakness could boost UK exporter competitiveness once global demand recovers.