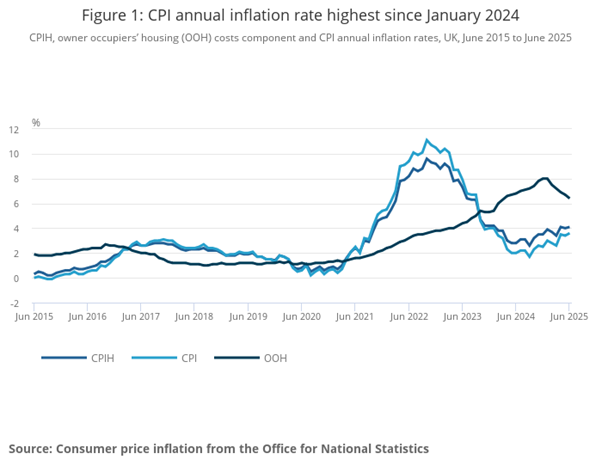

UK The United Kingdom’s inflation rate climbed to 3.8% in July 2025, up from 3.6% in June, presenting fresh challenges for the Bank of England as it attempts to balance price stability with economic growth. The latest Consumer Price Index (CPI) data from the Office for National Statistics shows persistent inflationary pressures despite the central bank’s recent monetary easing.

The Bank of England responded to mixed economic signals by cutting interest rates by 25 basis points to 4% in August 2025, marking the fifth rate reduction since the monetary policy tightening cycle peaked in 2023. However, the decision was far from unanimous, with policymakers voting 5-4 to reduce rates rather than maintaining them at 4.25%.

Food Inflation Drives Price Pressures Higher

Food and non-alcoholic beverages emerged as a significant driver of inflationary pressure, with prices rising 4.5% annually in June 2025. This represents the highest food inflation rate since February 2024, well below the peak witnessed in early 2023 but concerning nonetheless for household budgets.

The Office for National Statistics data reveals that upward effects came from bread and cereals, meat, and milk, cheese and eggs, highlighting how essential items continue to strain family finances across Britain.

Core inflation, which excludes volatile energy and food components, remained elevated at 3.7% in June 2025, up from 3.5% in May. This measure is closely watched by Bank of England officials as it provides insight into underlying price pressures less influenced by external shocks.

UK Consumer Price Index annual rate showing the upward trend [Source: ONS]

Bank of England’s Cautious Approach

Bank of England Governor Andrew Bailey emphasised caution in the central bank’s approach, stating during a press conference that “it remains important that we do not cut bank rate too quickly or by too much” while acknowledging “there are good reasons to think that this rise in headline inflation will not persist”.

The Monetary Policy Committee’s split decision reflects the challenging economic environment facing British policymakers. The Committee continues to be vigilant about the extent to which easing pay pressures will feed through to consumer price inflation, particularly given ongoing labour market dynamics.

Services inflation, a key concern for central bankers due to its sensitivity to domestic wage costs, held steady at 4.7% in June 2025, the same as in May. This persistence in services prices has contributed to the Bank’s cautious stance on future rate reductions.

Economic Headwinds and Global Uncertainty

The UK economy faces multiple challenges beyond domestic inflation. The Committee continues to judge that the overall impact of recent trade policy developments is, on balance, more likely to be disinflationary than inflationary, though uncertainty surrounding global trade policies adds complexity to monetary policy decisions.

Energy prices present another wild card in the inflation outlook. Recent developments in Middle Eastern geopolitics have contributed to oil price volatility, while wholesale gas futures and oil prices have increased since previous forecasts, potentially affecting household energy bills in coming months.

British Chancellor Rachel Reeves welcomed the interest rate cut, describing it as “welcome news, helping bring down the cost of mortgages and loans for families and businesses”. However, the government faces its own economic challenges, with fiscal policies introduced in late 2024 continuing to influence business confidence and investment decisions.

Future Rate Path Remains Uncertain

Financial markets anticipate further monetary easing, with investors expecting the BoE will cut rates at two meetings in the second half of 2025. However, the central bank has repeatedly emphasised that “monetary policy is not on a pre-set path”, suggesting future decisions will remain data-dependent.

The Bank of England expects CPI inflation to increase slightly further to peak at 4.0% in September before moderating towards the 2% target. This temporary increase reflects base effects from energy prices and administrative price changes rather than fundamental inflationary pressures.

Wage growth remains a critical factor in the inflation equation. Annual private sector regular AWE growth had declined further in the most recent data, to just below 5%, providing some comfort to policymakers concerned about wage-price spirals.

Global Context and Comparisons

The UK’s inflation challenges reflect broader global patterns, though with distinct domestic characteristics. Similar to Australia’s experience with inflation management, British policymakers must balance competing economic objectives while maintaining credibility in their inflation targeting framework.

The Bank of England’s approach contrasts with central banks in other jurisdictions, where different economic conditions have prompted varied policy responses. The European Central Bank has pursued its own easing cycle, while the Federal Reserve maintains a more hawkish stance amid different domestic pressures.

Looking Ahead: Balancing Act Continues

The path forward for UK monetary policy remains delicately balanced. The margin of spare capacity in the economy is expected to act against some continuing persistence in domestic prices and wages in order for CPI inflation to fall back to around the 2% target in the medium term.

Economists continue to debate the optimal pace of monetary easing. While some advocate for more aggressive rate cuts to support economic growth, others warn against premature easing that could reignite inflationary pressures. The Bank’s “gradual and careful” approach reflects this uncertainty.

For British households and businesses, the inflation outlook means continued pressure on living standards despite some monetary relief. Economic policy decisions remain crucial in determining whether the current inflationary episode proves temporary or becomes more entrenched.

The coming months will test the Bank of England’s resolve as it navigates between supporting economic recovery and maintaining its inflation mandate. With global uncertainties persisting and domestic price pressures remaining elevated, policymakers face complex decisions that will shape Britain’s economic trajectory through 2025 and beyond.

The next Monetary Policy Committee meeting is scheduled for September 2025, where fresh economic data will inform further policy decisions. Market participants and households alike await clearer signals about the future direction of both inflation and interest rates in an increasingly uncertain global environment.