St George Mining Limited (ASX: SGQ) (“St George” or the “Company”) has announced a significant extension of its strategic alliance with US-based REalloys Inc, signalling growing confidence in the Company’s world-class Araxá Rare Earths and Niobium Project in Brazil.

The partnership, first announced in September 2025, has been extended to allow for more detailed metallurgical test work and processing flowsheet development. Originally slated to conclude within 120 days, the Memorandum of Understanding (MOU) now runs for one year, reflecting the complexity and strategic importance of establishing secure rare earths supply chains independent of Chinese control.

REalloys continues metallurgical testing on rare earth oxalate samples produced from the Araxá Project, using proprietary technology for splitting and recovering individual rare earth elements. The test work aims to optimise processing flowsheets to produce materials most suitable for REalloys’ magnet-making operations.

The extended timeline enables both parties to conduct comprehensive technical work while exploring potential offtake arrangements for up to 40% of rare earths production from St George’s 40.6 million tonne @ 4.13% TREO resource.

REalloys: A Critical Player in US Rare Earths Independence

REalloys has established itself as a pivotal force in North America’s push for rare earths supply chain independence. The Company operates a fully integrated mine-to-magnet platform, producing high-performance magnet materials for the US Defence Logistics Agency (DLA), the Department of Energy’s AMES National Laboratory, and commercial enterprises across defence, aerospace and electronics sectors.

Figure 1: REalloys is North America’s next major Rare Earth producer [REalloys]

Recent strategic moves by REalloys underscore its expanding role in global supply chain diversification. In October 2025, the Company secured a strategic partnership with the Japanese Government through Japan Organisation for Metals and Energy Security (JOGMEC), facilitating technology transfer for separation and magnet fabrication to North American facilities.

In December 2025, REalloys announced a partnership with Saskatchewan Research Council, securing long-term offtake for 80% of production from an upgraded heavy rare earth refining facility. The appointment of Stephen S. duMont, President of GM Defence, as non-executive chairman in October 2025 further reinforces the Company’s defence industry credentials.

REalloys is completing a NASDAQ listing through a business combination with Blackboxstocks Inc (NASDAQ: BLBX), positioning it as one of the major listed rare earths companies in the United States.

Why This Matters: The Strategic Imperative for US Mineral Sovereignty

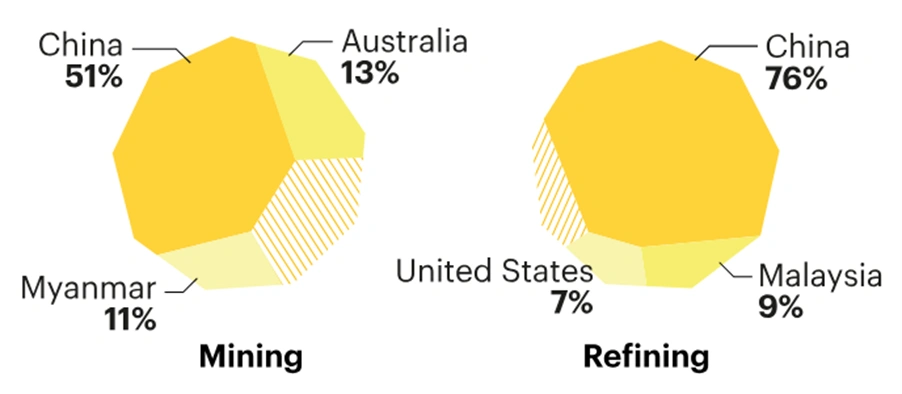

The extension of St George’s alliance with REalloys comes amid escalating US-China tensions over critical minerals supply chains. China controls approximately 60% of global rare earth extraction and more than 90% of downstream processing, including 94% of permanent magnet production, according to the International Energy Agency.

Figure 2: Top three rare earth producers 2030 [International Energy Agency]

Until 2023, China accounted for 99% of global heavy rare earths processing, leaving the United States critically exposed in defence supply chains. Heavy rare earths such as dysprosium and terbium are essential for high-temperature permanent magnets used in F-35 fighter jets, Virginia-class submarines, and advanced military systems.

The urgency for supply chain diversification intensified in 2025 when China imposed stringent export restrictions on rare earth elements. In April 2025, Beijing restricted exports of seven critical elements, expanding controls in November to include five additional elements and all related compounds, metals and magnets. These measures disrupted Western manufacturers and forced emergency consultations between the US and China.

President Trump’s 14 January 2026 proclamation “Adjusting Imports of Processed Critical Minerals and Their Derivative Products into the United States” empowered government agencies to negotiate agreements addressing import risks, potentially including price-floor guarantees for trade.

The US Department of the Treasury’s 12 January 2026 ministerial meeting brought together finance ministers from G7 nations and other countries to discuss securing critical mineral supply chains, with rare earth elements as a primary focus.

Araxá: A World-Class Resource Strategically Positioned

St George’s Araxá Project boasts a JORC-compliant mineral resource of 40.6 million tonnes @ 4.13% Total Rare Earth Oxides (TREO), making it the largest and highest-grade carbonatite-hosted rare earths deposit in South America and the second highest grade in the Western world.

The resource includes significant quantities of critical magnet rare earths, with neodymium-praseodymium (NdPr) representing more than 20% of TREO content. These elements are essential for permanent magnets used in electric vehicles, wind turbines, defence systems and consumer electronics.

Located in Minas Gerais, Brazil, adjacent to CBMM’s world-leading niobium operations, the Project benefits from established infrastructure, skilled local workforce, renewable power access, and expedited permitting support from Brazilian federal and state governments.

Figure 3: Map showing location of Araxá Project in Minas Gerais, Brazil, and proximity to infrastructure [St George Mining]

St George has been selected to participate in Brazil’s MagBras Initiative, a federal programme aimed at establishing an integrated rare earth products supply chain, including permanent magnet production, entirely within Brazil.

Press reports indicate that discussions between the US and Brazil regarding a trade deal on critical minerals are advancing favourably, with rare earths as a key component. St George is engaging directly with US Government representatives regarding potential commercial arrangements to support Araxá’s development.

Proven Production Capability: Rare Earth Oxalate Already Produced

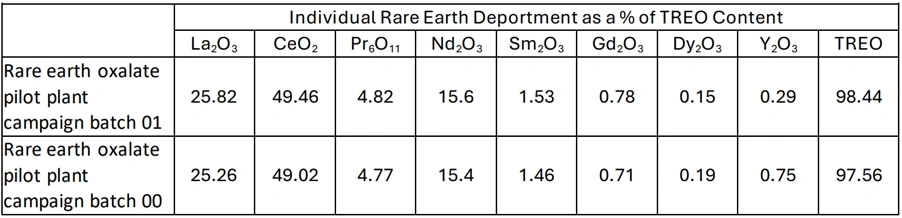

St George’s confidence in commercialising Araxá’s rare earths is underpinned by historical success. A rare earth oxalate was successfully produced from Araxá mineralisation in a 2012/13 pilot plant study, demonstrating the viability of the processing route.

The pilot plant, now in St George’s possession, will be utilised to construct a new facility at the St George Technological Centre, being established in collaboration with CEFET, Brazil’s leading technical university. Samples of the retained rare earth oxalate have been delivered to REalloys for metallurgical testing.

Figure 4: Rare Earth Oxalate Products from 2012/13 Pilot Plant [St George Mining]

Critical magnet rare earths (NdPr) represent over 20% of TREO content, with heavy rare earths, including samarium and dysprosium, also present at strategic levels for magnet production.

Market Dynamics: Rare Earths Demand Surging

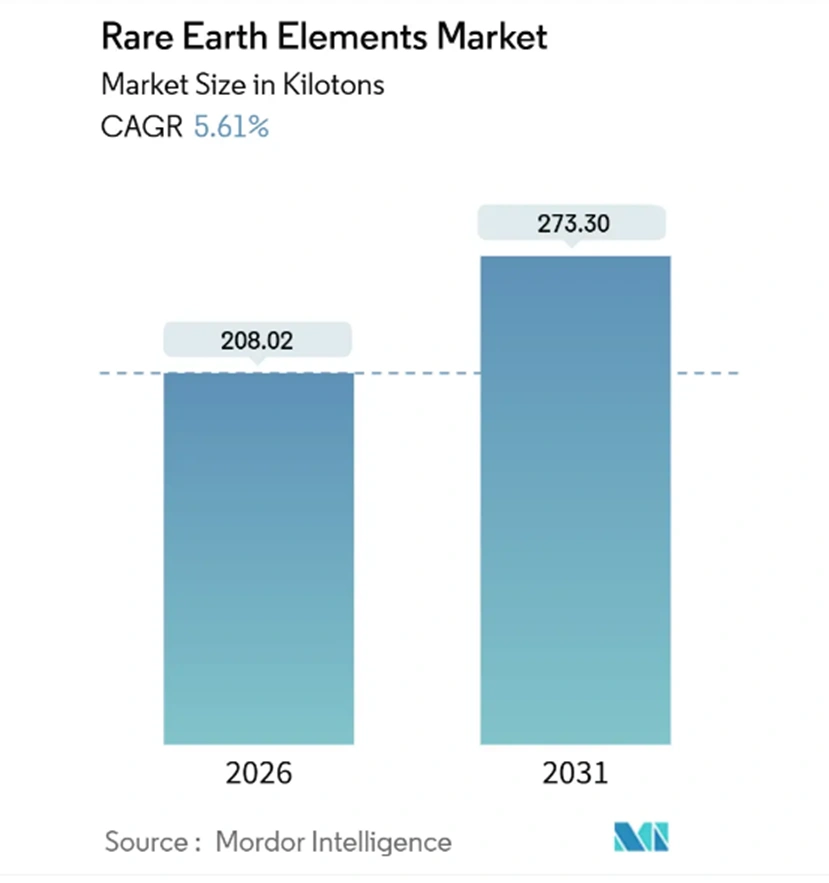

The global rare earths market is experiencing robust growth driven by electrification, renewable energy deployment and defence modernisation. Market projections vary but consistently point to substantial expansion. Grand View Research forecasts the market reaching USD 6.28 billion by 2030, growing at a CAGR of 8.6% from 2025

Permanent magnet applications are expanding at 7.43% CAGR, driven by electric vehicles, wind turbines and industrial robotics, according to Mordor Intelligence. Dysprosium leads elemental growth with a 7.26% CAGR, reflecting its irreplaceability in high-temperature magnets.

Figure 5: Rare earth elements market size [Mordor Intelligence]

The US Department of Defence has committed over USD 439 million since 2020 toward building domestic rare earth supply chains, with a goal to develop a complete mine-to-magnet capability meeting all defence needs by 2027.

Executive Commentary: Strategic Timing

John Prineas, St George Mining’s Executive Chairman, commented on the extension:

“The US government continues to push for greater security in rare earths supply chains and REalloys is at the forefront of delivering a fully integrated mine to magnet solution that is focused on North American supply chain independence.

“We are excited to be continuing our collaboration with an industry leader like REalloys, an alliance that has potential to provide an attractive pathway for St George to access the rapidly developing and lucrative downstream sector of the US rare earths industry.

“The Araxá Project boasts a world-class, hard-rock rare earths resource with scale that makes it well-positioned to be a potential supplier of rare earths product for ex-China supply chains being established in Brazil, the US and other countries.

“Araxá is a hard-rock rare earths resource, the same style of deposit as the two major rare earths mines outside of China, the Mt Weld mine of Lynas Corporation and MP Materials’ Mountain Pass. Araxá is already comparable to these deposits in terms of volume and grade, and our resource upgrade due later this quarter is poised to further propel Araxá up in world-class rankings.”

Figure 6: St George meeting with US government representatives at EXPOSIBRAM in October 2025. Third from left, John Prineas; fourth from left, Gabriel Escobar (Chargé d’Affaires, US Embassy Brasilia); fifth from left, Adriano Rios (Director, St George Brasil)[St George Mining]

Investor’s Outlook

St George Mining Limited (ASX: SGQ) continues to gain traction among investors focused on critical minerals exposure. The Company’s strategic positioning at the intersection of US-Brazil rare earths cooperation, combined with its world-class resource and proven production capability, provides a compelling investment thesis.

Stock Performance (as of 21 January 2026):

- Current Price: AUD 0.125

- 52-Week Range: AUD 0.015 to AUD 0.180

- Market Capitalisation: ~AUD 475.62 million

Figure 7: SGQ Price Chart [ASX]

The Company’s strategic alliance with REalloys positions St George as a potential key supplier to US rare earths supply chains at a time when government support, industry partnerships and market fundamentals are strongly aligned.

Key Catalysts Ahead:

- Resource upgrade expected later this quarter

- Metallurgical test work results from REalloys

- Potential offtake agreement finalisation

- US-Brazil trade deal developments

- Federal and state government support announcements

As geopolitical tensions persist and governments worldwide prioritise supply chain security, companies like St George Mining with proven resources outside Chinese control are increasingly valuable. The extension of the REalloys alliance is not just a corporate development; it is a signal that the Company is moving from exploration story to strategic supplier in a rapidly evolving global landscape.