Sims Limited has launched a bold strategic move in North America, announcing the US$66.5 million acquisition of Tri-Coastal Trading (TCT) in Houston, Texas, a transaction the Company says will structurally lift margins, consolidate its regional footprint and unlock more than US$100 million in surplus land value within two years.

The deal, unveiled on 10 February 2026 as part of the Company’s HY25 results presentation, positions Sims as a lower-cost, higher-margin operator in one of the world’s most attractive ferrous scrap markets.

A transformative acquisition, not just expansion

Sims framed the Tri-Coastal purchase as more than a bolt-on deal; it represents a structural upgrade to its North American Metals (NAM) business.

Major transaction highlights include:

- Purchase price: US$66.5 million, cash-free and debt-free.

- Earnings impact: +US$25 million in annual EBITDA (including Sims’ existing Houston operations).

- Returns: Expected post-synergy ROIC of 20%+.

- Valuation: Less than 4× EBITDA after synergies.

- Throughput: 350,000+ tonnes per annum of predominantly cut-grade ferrous scrap.

- Tenure: 18-year third-party operations contract with two optional five-year extensions.

Figure 1: Sims Limited powers up its North American strategy, a high-return move into Houston that strengthens margins, unlocks land value, and positions the Company at the heart of global scrap markets.

Why Houston matters

Houston is not a normal scrap market. It sits at the intersection of US industrial production, global shipping lanes and deep-water port infrastructure.

Sims emphasised that:

- Houston ranks as the fourth-largest US city, within a state economy exceeding US$2.5 trillion GDP.

- Export ferrous scrap prices have consistently traded at a premium to domestic pricing.

- Direct port access gives Sims optionality to sell into global markets rather than rely solely on US domestic demand.

In practical terms, this means the Company can ride global scrap demand during upcycles while maintaining domestic outlets during downturns — a built-in risk hedge.

Synergies: where the real value lies

Sims expects the bulk of the financial upside to come from operational integration rather than volume growth alone.

Revenue and margin uplift

- Bulk ferrous sales at Tri-Coastal already command a premium versus legacy Sims sites.

- Exclusive access to the Woodhouse terminal and city dock expands shipping flexibility.

- A larger consolidated footprint widens supplier reach and lifts market share.

Cost savings and efficiency

- Rationalisation of three additional sites alongside the planned sale of Mayo Shell.

- Removal of dock premiums through deep-water access.

- Lower cost per tonne and streamlined overheads.

- A unified logistics model combining truck, barge and rail from a single strategic hub.

Capital efficiency and value release

- More than US$100 million in surplus land sales expected within 1–2 years.

- Reuse, resale or retirement of redundant equipment.

- Elimination of the need to develop the existing Mayo Shell site — saving future capital spend.

Property strategy reshapes the balance sheet

Alongside the acquisition, Sims outlined a four-tier property strategy:

- Contracted assets: including Mayo Shell, now under an Asset Sale Agreement subject to due diligence.

- Surplus properties: to be exited within 1–2 years, including newly acquired Houston land.

- Medium-term assets: potentially rezoned or repurposed over 5–10 years.

- Core operational sites: retained for long-term recycling activity.

A dedicated Property Strategy Lead is being recruited to accelerate realisations and manage planning, rezoning and environmental processes.

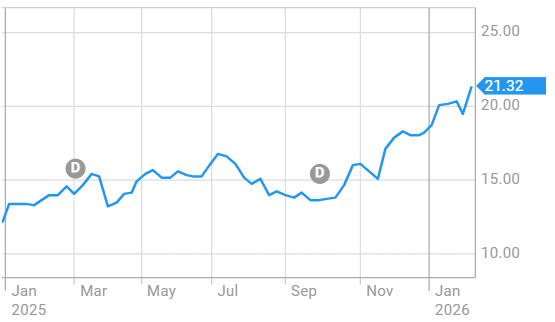

Market reaction: ASX investors reward the strategy

The market responded positively to Sims’ execution story.

Share Price Activity (ASX):

- Last price: A$21.32

- Change: +$0.70 (+3.40%)

Performance snapshot:

- 1 Week: +7.19%

- 1 Month: +13.77%

- 2026 YTD: +18.51%

- 1 Year: +55.51%

- vs Sector (1yr): +19.10%

- vs ASX 200 (1yr): +50.78%

The Company’s current market capitalisation is A$4.114 billion. Sims now trades as one of the stronger performers in Australia’s industrial materials space.

Figure 2: 1 year performance of the Sims Limited (ASX: SGM) Stock [ASX]

What’s next for Sims?

Sims flagged several upcoming investor touchpoints:

- HY26 Financial Results: Sydney, 17 February 2026 (AEDT).

- US Investor Day: Houston, 24 March 2026, including a Tri-Coastal site tour.

- Nashville presentations: 25 March 2026, featuring Sims Lifecycle Services (SLS).

These events should provide more clarity on integration timelines, cost savings and land divestment proceeds.

Investors Outlook

Sims Limited now looks strategically stronger, operationally leaner and better positioned for global scrap cycles than at any point in recent years. The Tri-Coastal acquisition transforms Houston from a collection of assets into a cohesive, export-enabled hub — exactly where investors want to see scale and efficiency.

In the near term, cash flows should benefit from:

- Higher ferrous volumes,

- Lower unit costs, and

- Land sale proceeds that can reduce debt or fund higher-return investments.

Over the medium term, the Company’s exposure to export pricing provides meaningful upside if global steel production strengthens, while domestic access offers protection if markets soften.