Rare earths constitute a critical component in the fast-changing landscape of technology and clean energy in the 21st century. Be it powering electric vehicles, creating renewable energy systems, or providing the finishing touch to advanced electronics, rare earths are the quintessential building blocks. On account of their strategic importance, these minerals remain at the centre of geopolitical tussles among countries vying for control over supply chains. This article deals with issues relating to why rare earths matter, global geopolitics, the role of ASX-listed juniors, and the investment landscape surrounding these.

1. Why Rare Earths Matter: The Backbone of Modern Technology

1.1 Essential Applications in Technology and Clean Energy

Rare Earth Elements (REEs)—17 chemically similar metals, including neodymium, dysprosium, and lanthanum—are indispensable for modern technology. Their unique properties make these magnets important in various sectors, including consumer electronics, clean energy systems, catalysis, and electrochemical applications. NdFeB magnets, among the strongest permanent magnets, are used widely in EV motors, wind turbines, and various other electronic devices. With the increasing demand for clean energy and advanced technology worldwide, the strategic importance of the REEs is ever-growing.

Rare Earth Elements: Essential 17 metals powering modern technology globally.

1.2 Electric Vehicles (EVs)

The EV industry is one of the major drivers of demand for rare earth. Neodymium, praseodymium, and dysprosium are key ingredients of high-performance magnets employed in EV traction motors, which are more power- and space-efficient than their conventional counterparts. For example, Teslas use NdFeB magnets in their motors, which are an inherent element of performance and efficiency. Along these lines, industry watchers hold that worldwide EV production shall top the 35-million-unit mark by 2030, unprecedented demand for REEs being created to keep this conversion of transport to electrified transport.

1.3 Wind Turbines

Wind energy is another significant consumer of rare earths. Typically, the permanent magnets, which employ neodymium and dysprosium in direct drive wind turbine systems, are used in modern offshore and onshore wind turbines. These magnets increase efficiency and reduce maintenance by eliminating common problems associated with gearboxes. A single large turbine may contain as much as five tonnes of magnets, of which about 30% by weight consists of REEs. The demand for such elements is expected to increase in the next ten years as many countries push to increase capacity for renewable energy.

1.4 Consumer Electronics

The common consumer applications also require REEs. In small but powerful magnets for speakers and vibration motors in smartphones and laptops, neodymium is involved. Terbium and dysprosium are needed in phosphors for bright LED screen displays. The worldwide proliferation of these smart devices keeps a strong demand for these metals, underlining the importance of having an assured and sustainable road to the supply of these metals.

1.5 Defence Technologies

Defence applications further underscore the strategic value of rare earths. Advanced technologies such as guidance systems, radar, and lasers rely heavily on REEs. The Lockheed Martin F-35 fighter jet, for instance, contains roughly 920 pounds of rare earths in electronic warfare systems, radar, and motorised components. China’s dominance in rare earth mining and processing has raised concerns about supply chain vulnerabilities in this critical sector, prompting governments to prioritise domestic sourcing and strategic reserves.

Increasing reliance on goestos and technologies emphasises the strategic need for securing a steady supply of the rare earth elements.

The F-35 fighter jet contains 920 pounds of rare earths.

2. Global Geopolitics: China’s Dominance and Supply Security

2.1 China’s Control Over the Rare Earth Supply Chain

China holds a commanding position in the global rare earth market by mining approximately 69% of the rare earth ores as of 2023. This control is exercised not only at the mining level but also over 90% of the world’s rare earth refining capacity, while the country also produces around 90% of rare earth magnets in the world. The Bayan Obo mine in Inner Mongolia is one of the largest and most important sources of rare earth minerals in China. This mine, along with others in the region, contributes to satisfying a large portion of domestic production and strengthening its central position in the global supply chain.

2.2 Export Restrictions and Strategic Leverage

In April 2025, China imposed export restrictions on seven rare earth elements-and samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium- together with related magnets and alloys. These materials are important in a variety of high-tech and defence applications, such as electric vehicle motors, wind turbines, and semiconductor manufacturing.

Restrictions require foreign buyers to obtain special export licenses, thereby giving strategic leverage to China vis-à-vis the industries in the United States, Europe, and Japan. This has upset global supply chains, with companies like Ford and Suzuki stopping production for want of essential components.

In April 2025, China restricted exports of seven rare earth elements.

2.3 Implications for Global Markets

China’s dominance in the rare earth sector hits global markets. In this situation, export restrictions have apparently raised prices and created uncertainties in supply, giving opportunities to countries and companies to look for other sources and build internal capabilities.

Meanwhile, the G7 countries and the EU are considering the implementation of price floors and potential taxes on Chinese exports of rare earth to gradually eliminate dependence and foster domestic production. In another supply diversification movement, Australia is also preparing to grant shares of its newly formed strategic reserve of critical minerals to some allied countries, including the United Kingdom.

This only highlights the geopolitical aspect of rare earth elements and calls for countries to be able to set secure and diversified supply chains in support of their respective technological and defence industries.

3. Australia’s Response: Diversifying Supply Chains

3.1 Strategic Reserve of Critical Minerals

Having regard to increasing global demand and geopolitical uncertainties, Australia is creating a Critical Minerals Strategic Reserve. This initiative enhances national security and supply chain resiliency by stockpiling minerals, such as rare earth, lithium, and cobalt. The reserves would contain minerals that are pertinent to defence, clean energy technologies, and advanced manufacturing, so that, from the point of view of market disruptions and strategic needs, Australia may respond adequately.

3.2 International Collaboration with Allied Nations

By ensuring critical mineral supply chains are diversified, Australia is strengthening its partnerships with key allies. In a milestone development, POSCO, a South Korean conglomerate, has opened its inaugural Critical Minerals R&D Lab in Western Australia. The lab would work with Australian agencies on lithium ore extraction, rare earth refining, and low-carbon steel production, emphasising the strategic significance of international cooperation in critical minerals.

3.3 Policy and Regulatory Support

The Australian government has formed policies to support the development of the critical minerals sector. Initiatives to attract investments, streamline regulatory processes, and promote ESG standards are outlined within the framework of the Critical Minerals Strategy 2023-2030. These include establishing the Critical Minerals Office to offer national policy and strategic advice, as well as establishing the Critical Minerals Production Tax Incentive to foster the processing and manufacturing activities in Australia.

POSCO opens first Critical Minerals R&D Lab in Western Australia.

4. ASX and Global Rare Earth Juniors: Investment Opportunities

4.1 High-Risk, High-Reward Potential

Capitalised gains potential in the junior rare earth companies is large, but they are equally risky. Most early-stage persons with whom one comes into contact have little funding and resources. Sometimes, obtaining financing requires a convoluted process of joint ventures. Occasionally, even permits cannot be obtained. But when a junior does manage to advance a viable deposit, the returns can be immense. Australian juniors such as Hastings Technology Metals and Australian Rare Earths advance projects on Yangibana and Koppamurra, respectively, basing their projects on neodymium-praseodymium (NdPr) concentrates.

4.2 Market Dynamics and Investor Considerations

The rare earth sector is influenced by several key factors:

- Demand Trends: The shift towards electric vehicles (EVs), renewable energy systems, and advanced defence technologies is driving increased demand for rare earth elements, particularly NdPr.

- Price Movements: Prices for rare earths have experienced volatility, influenced by geopolitical tensions and supply chain disruptions. For example, China’s export restrictions in April 2025 led to a 75% drop in magnet exports, impacting global manufacturing..

- Stock Performance: Companies with exposure to critical minerals and U.S. markets are receiving heightened investor interest. Stocks like Trigg Mining have seen re-ratings due to their North American ties and critical mineral exposure.

Investors should consider these dynamics when evaluating opportunities in the rare earth sector.

4.3 Top ASX-Listed Large-Cap Rare Earth Companies and Their Key Projects

| Company Name | ASX Code | Key Projects | Overview |

| Lynas Rare Earths Limited | LYC | Mt Weld Mine, Malaysia Refinery | Australia’s largest rare earths producer and only significant producer outside China. |

| Iluka Resources Limited | ILU | Eneabba Rare Earths Refinery | Major global producer of zircon and titanium dioxide; developing a rare earths refinery in WA. |

| Arafura Rare Earths Limited | ARU | Nolans Project | Focused on producing NdPr products from the Nolans Project in the Northern Territory. |

| Northern Minerals Limited | NTU | Browns Range Project | Developing Browns Range Heavy Rare Earth Project, focusing on dysprosium and terbium. |

| Australian Strategic Materials Limited | ASM | Dubbo Project | Developing the Dubbo Project in NSW to produce a range of critical metals, including rare earths. |

ASX Junior rare earth companies offer high gains but come with significant risks.

5. Investment Thesis: Balancing Opportunities and Risks

5.1 Opportunities in the Rare Earth Sector

- Increasing Demand: Growing adoption of electric vehicles, renewable energy technologies, and advanced electronics constitutes the increasing demand for rare earths.

- Geopolitical Shifts: With attempts by Australia, the G7, and others to diversify supply sources, alternative supply chains present an opportunity to investors.

- Technological Innovations: In contrast, recycling advancements and rare-earth-free alternatives could relax supply constraints, thereby providing alternative investment avenues.

5.2 Risks to Consider

- Supply Chain Disruptions: Export restrictions and quota systems imposed by a dominant producer such as China, for instance, have the potential to create supply shortages and price volatility.

- Environmental and Regulatory Challenges: Mining projects face scrutiny on environmental grounds and compliance with tough regulations, which may impact the timelines and costs of the projects.

- Market Speculation: Speculative in nature, junior mining stocks may be subject to drastic price changes, thus putting the investors at risk.

6. Outlook: A Shifting Landscape

6.1 Emerging Trends in Rare Earth Supply and Demand

The global demand for rare earth elements (REEs) will see spectacular growth, enhancing clean energy technology and electrification. The global demand for REEs shall exceed 220,000-250,000 metric tons by 2025, with approximately 30% of its consumption going into magnets for electric vehicles (EVs), wind turbines, and consumer electronics.

Recycling is set to play a strategic role in all efforts to meet this demand. The worldwide market for rare earth recycling is projected to reach $1 billion by 2030, growing at a CAGR of 5.3% between 2024 and 2030. Cutting-edge recycling technologies allow for the recovery of REEs from secondary and end-of-life products, thus cutting down on mining and primary material sourcing.

Substitution technologies are also being considered for the risks to supply; research into alternative materials such as iron nitride is underway to supplant REEs in magnet production, potentially relieving pressure on the supply chains.

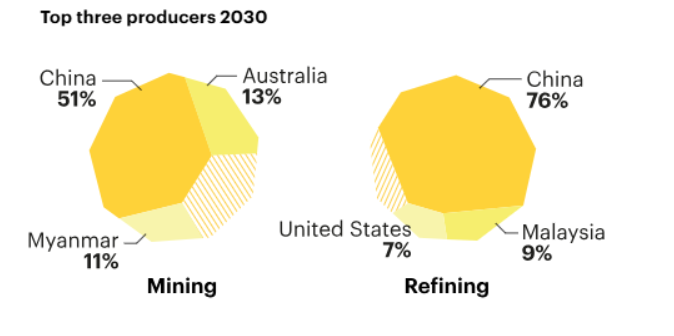

Top three rare earth producers in 2030: mining and refining shares.

6.2 Strategic Implications for Investors and Governments

For investors, the ever-changing nature of the REE landscape presents myriad opportunities and attendant risks. By diversifying their portfolios and investing in companies engaged in REE recycling and research into substitution technologies, one can gain exposure to emerging sectors. On the downside, investments in early-stage projects should be considered with caution, given the possible existence of regulatory or market uncertainties.

In response to the strategic importance of REEs, governments are enacting policies to secure supply chains. Australia, for example, is sharing its critical minerals reserve with allied countries, such as the United Kingdom, amongst others, to reduce dependency on China for REEs and minor metals.

Balancing industrial growth with environmental responsibility continues to be a major challenge. As a result, policymakers are emphasising sustainable mining practices and recycling initiatives to lessen ecological impacts while ensuring the uninterrupted supply of REEs.

6.3 Future Scenarios and Market Predictions

The forecasts for markets in rare earths change according to geopolitical situations and the development of technologies. Demand for rare earths, says the International Energy Agency (IEA), shall increase by 50–60% by 2040 on account of clean energy technologies.

With the most optimistic situation, recycling and substitution technologies will develop, supply chains will diversify, and the markets for REEs will thus be adequately stabilised, leaving geopolitical tensions largely a matter of history. In the worst case, a shortage of supply is experienced, available supplies dwindle, and slow technological progress ignites prices for REEs and industries that depend on them.

Half a decade will, therefore, determine the future of the REE sector. Very strategic investments will have to be made into technology and infrastructure, with focus also laid on partnerships between nations, as these factors will make a difference in the resilience and sustainability of global supply chains.

Also Read: Australia Steps Up as Strategic Alternative to China’s Rare Earths Monopoly

7. FAQs

Q.1 Why are rare earth elements essential in modern technology?

REEs find application in the making of very powerful magnets, batteries, and other electronic components within technologies such as electric vehicles, wind turbines, and consumer electronics.

Q.2 How does China’s dominance affect the supply chains?

Since China supplies around 70% of global REEs and carries out processing operations, the country commands a great deal of influence over the supply chains. Export restrictions can even cause some disruption to global markets, exposing the vulnerability of relying on a sole supplier.

Q.3 What is Australia doing to secure critical mineral supplies?

Australia is establishing a strategic reserve of critical minerals for which it will offer shares to allied countries. The reserve is backed with A$1.2 billion and is expected to come into operation by late 2026.

Q.4 Does the rare earth sector offer investment opportunities?

Yes, opportunities do exist for early-stage exploration companies as well as established players. When considering investments, one should think about project viability, technological risks, and geopolitical complications.

Q.5 What are the environmental concerns associated with rare earth mining?

REE mining can result in habitat destruction, water contamination, and the generation of radioactive waste. Sustainable mining practices and recycling initiatives are being developed to mitigate these environmental impacts.

Q.6 How can technological advancements impact the sector?

Advancements in recycling technologies can increase the recovery of REEs from end-of-life products, reducing the need for primary mining. Substitution technologies may also alleviate supply pressures by replacing REEs with alternative materials in certain applications.