Pilbara Minerals posted improved pricing and shipment in the period of December. The sales volumes had increased by 8 % relative to the September quarter. The realised prices increased by 57 % quarter-to-quarter.

This combination shot the income high throughout the business. The period saw a revenue of 373M in the group. It was a 49 % growth over the previous quarter. The realised price was on an SC5.2 basis, on average, of US$1,161/t.

The sales amounted to 232.0kt spodumene concentrate. Increased prices had a direct positive effect on operating cash flow. The management reported that market conditions were already experiencing a tightening of supply.

Inventory decreased, and customers became more active in buying. The recovery of pricing helped in recovering a high margin of operation.

Pilgangoora operation keeps increasing its lithium shipments per quarter.

PLS December 2025 Quarterly Shows Solid Production Performance

This operational delivery was not affected even amid market volatility. The quarterly production was at 208kt. Recovery of lithium was approximately 76 per cent, which is equal to internal plans.

The total material transported improved to 8.1Mt. Efficiencies in mining increased the productivity of the fleet and the availability of the ore. Higher throughput was sorted successfully by ore sorting.

Crushing wear levels increased, and buffers cushioned the use of plants. The sales were even higher than the production since the inventory was decreasing. The realised price of SC6.0 equivalent was at US1,336/t. Unit operating cost FOB increased by 585/t.

Royalties led to an increase in CIF unit cost to $717/t. Margins improved due to improved pricing, even though there was pressure on cost. The company had steady production as it prepared to experience high demand.

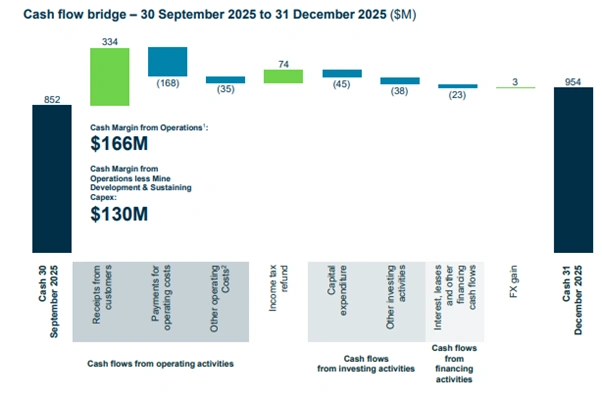

How Strong Is The Company’s Cash Position Now?

The financial strength has increased significantly during the quarter. The operation cash margin reached six figures of 166M. That was in comparison with $8M before. Cash balance rose by 12% to $954M by the end of 31 December 2025.

The period saw cash increase by $102M. Customer receipts amounted to $334M. Operating payments were at 168M. Liquidity was also provided with a $74M income tax refund. On the cash basis, capital expenditure was 45M.

The group had made an investment in the P-PLS joint venture of $38M. The management indicated that the liquidity is close to $1.6B. The balance sheet is flexible towards making future growth-related decisions. High cash flow provides stability in case of lithium price fluctuations.

Cash hoard reinforces Pilbara Minerals financially to grow.

Growth Options And Portfolio Flexibility Strengthen Strategy

Pilbara Minerals is still considering upstream and downstream. The Ngungaju restart is still pending. Critical works are done with high interest by the customers.

Approval of the plant could lead to an increase in the plant by approximately 200ktpa. The decision of the board will be expected in the March Quarter 2026.

The P2000 feasibility work is aimed at the expansion to ca. 2Mtpa. The timelines are undergoing re-examination following price enhancement. Drilling and optimisation are also promoted in the Colina Project of Brazil.

Mid-Stream Construction Mid-Stream Demonstration Plant was completed in this quarter. These programs maintain long-term optionality of the value chain. The emphasis of management is put on discipline in capital allocation and balance sheet strength.

What Is Happening In Chemicals And Downstream Operations?

The POSCO Pilbara Lithium Solution plant is still a strategic one. Pilbara Minerals owns 18% of the interest in the plant. Nameplate capacity of the facility is 43ktpa lithium hydroxide.

The two trains were idled in the quarter. Japanese battery supplies interruptions caused cancelation of customer orders. The total amount of CY25 that was produced was 12,860t, and its sales were 12,969t. H2 FY26 anticipate that production will remain stagnant.

Spodumene feedstock will be diverted to other customers. The group provided approximately $38M to hold on to ownership. This strategy will save working capital when the demand is uncertain.

POSCO plant strategic, 43ktpa capacity, trains idled this quarter.

Market Signals Point To Long-Term Lithium Demand Strength

Lithium Improvements Lithium prices recover early after recent volatility. In January, the average SC6 price was approximately US 2,335/t.

The supply chains are tightening in terms of inventory levels. The use of electric vehicles is still keeping the structural demand. Consumption growth is further added by energy storage systems.

The projections of the industry indicate that the demand will grow over a period. The trends in policy support and electrification are still maintained all around the world. Pilbara Minerals can be seen in this cycle.

In the PLS December 2025 quarterly, the fundamentals are on the way to being improved. Good cash, pricing, and volumes will help in getting investor confidence. The firm has now found a balance between strictness and selective preparation to grow.

Also Read: Iron Ore Market Impact 2026: Pilbara Discovery Reshapes Global Supply

FAQs

Q1: What were Pilbara Minerals’ Q2 FY26 revenue figures?

A1: Revenue reached $373M, up 49% quarter on quarter.

Q2: How much lithium concentrate was sold?

A2: Sales volumes totalled 232.0kt during the quarter.

Q3: What is the company’s cash balance?

A3: Cash balance stood at $954M as at 31 December 2025.

Q4: Why were downstream operations idled?

A4: Battery supply disruptions and weaker orders prompted temporary idling.