Pilbara Minerals Limited (ASX:PLS) remains a battleground for institutional investors. The lithium giant’s shareholder register reads like a who’s who of global fund managers.

But after a punishing 12 months, are they about to regret their conviction?

The Institutional Ownership Picture

Institutional investors control approximately 59-67% of Pilbara Minerals, giving them enormous influence over the company’s direction. This concentrated ownership means their trading decisions can create significant share price volatility.

The top institutional shareholders include:

- State Street Global Advisors with 11% of outstanding shares

- Australian Super Pty Ltd holding 9.8%

- BlackRock controlling 6.3%

The top 10 shareholders collectively account for roughly 52% of the register, creating a balance between large and smaller investors.

Recent Stock Performance Tells Two Stories

The numbers paint a sobering picture for long-term holders.

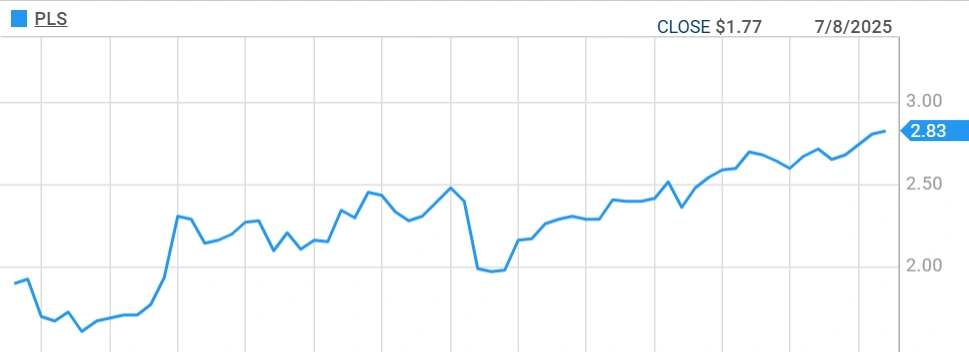

Pilbara Minerals Share Price

Institutional investors endured a 62% loss over the past year, though a recent 10% weekly gain provided some relief. The stock has traded within a wide range, reflecting the broader lithium market’s turbulence.

As of October 2025, Pilbara Minerals shares were trading at AUD 2.81, up 2.55% at close, within a 52-week range of AUD 1.07 to AUD 3.27.

The volatility has tested even the most patient investors.

Strong Operational Results Despite Price Pressure

Here’s where the story gets interesting.

In Q4 2025, Pilbara delivered a 28% increase in quarterly revenue to AUD 193 million, while production volume surged 77% to 221,000 tonnes. These operational wins came despite weaker lithium prices.

The company maintains a robust cash position of AUD 1 billion, providing a strong financial buffer.

Key operational highlights include:

- Record spodumene production across FY2025

- Completion of P680 and P1000 expansion projects

- Integration of advanced ore sorting technology

- Strong cost control with unit operating costs declining

The Lithium Market Paradox

CEO Dale Henderson describes the current environment as “The Lithium Paradox: Market Pain, Strategic Gain.”

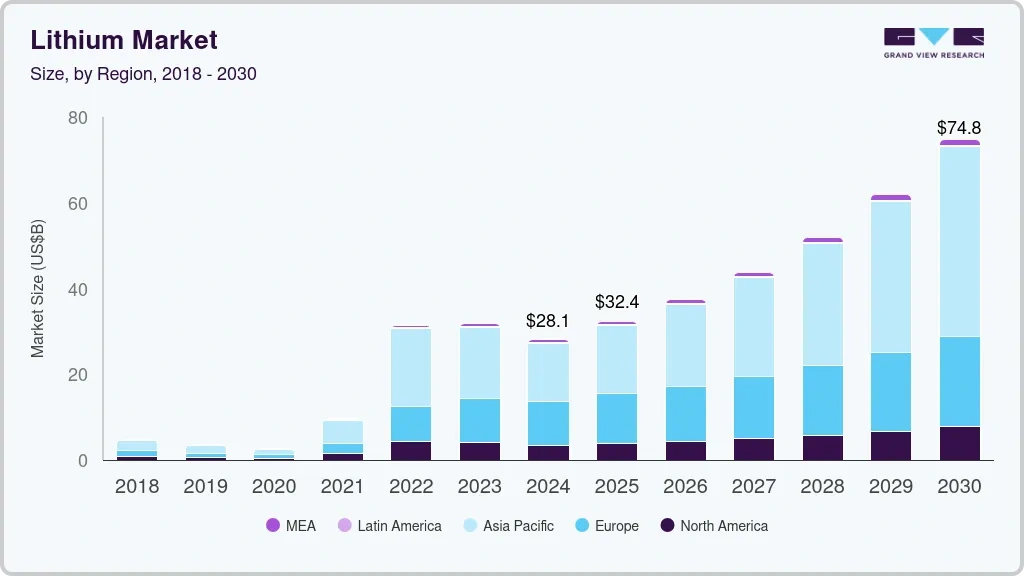

Market research projects the global lithium mining market could expand from approximately USD 28.08 billion in 2024 in 2025 to USD 74.81 billion by 2030, representing a fourfold increase.

Lithium Market Summary

Yet current prices remain depressed due to oversupply.

The disconnect between long-term demand projections and near-term pricing creates opportunity for well-positioned players. With a share of around 47% of global lithium production, Australia remains the only significant Western country that participates substantially in the market.

Why Institutions Haven’t Bailed

Three factors explain institutional investor patience:

- Strategic Position: Pilbara operates the Pilgangoora Operation in Western Australia, one of the world’s largest hard-rock lithium deposits, positioning the company as a key player in the global supply chain.

- Execution Track Record: The company has consistently delivered on production targets despite market headwinds. Australia’s lithium industry has shown remarkable resilience through challenging cycles.

- Balance Sheet Strength: The billion-dollar cash position provides staying power that smaller producers lack.

Recent Strategic Moves

Pilbara’s AUD 560 million acquisition of Latin Resources, approved in January 2025, added the Salinas lithium project in Brazil’s Minas Gerais state to its portfolio.

This geographic diversification reduces risk and opens access to North American and European battery markets.

The company also secured strategic offtake agreements with major battery manufacturers including BYD, LG, CATL, and Hyundai.

The Risk-Reward Calculus

Institutional investors face a clear decision matrix.

If weakness in Pilbara’s share price continues, institutional investors may feel compelled to sell, potentially triggering further declines.

However, the alternative scenario offers compelling upside. Development timelines for new lithium projects typically span 5-7 years, creating natural supply constraints that become more pronounced as canceled or delayed projects restrict future supply growth.

What This Means For Investors

Critical minerals companies like Pilbara Minerals represent a leveraged bet on the energy transition.

The stock’s current valuation assumes lithium prices remain depressed. Any recovery in pricing could deliver outsized returns given the company’s operational platform and cost structure.

Analysts offer mixed views, with 6 recommending buying while 4 suggest selling, leading to an overall neutral rating.

The Bottom Line

Institutional investors haven’t abandoned Pilbara Minerals. Their significant ownership stake demonstrates continued conviction in the company’s long-term prospects.

Whether that faith proves justified depends on lithium market dynamics over the next 12-24 months. The operational fundamentals are solid. The balance sheet is strong. The strategic positioning is excellent.

What remains uncertain is the timing of the lithium market’s recovery.

For institutions with long time horizons, that uncertainty may be acceptable. For retail investors, the question becomes whether they have the same patience to wait out the cycle.

The answer will determine who profits when the lithium market eventually rebounds.