Macquarie Group Ltd (ASX: MQG) has been caught up in the broader market sell-off of recent weeks, but analysts remain optimistic about the Macquarie share price forecast over the next 12 months. The Company’s globally diversified earnings base and four distinct business segments have kept it in favour with institutional analysts even as volatile conditions weigh on ASX financial shares more broadly.

![]()

Figure 1: Macquarie Group logo displayed on its office building exterior [Courtesy: ABC News]

Macquarie earns approximately two-thirds of its revenue internationally, a structural characteristic that reduces regional concentration risk and expands the universe of growth opportunities the Company can pursue. That global earnings profile is central to why analysts maintain conviction on the MQG price target 2027 despite current market turbulence.

What Analysts Are Forecasting for the Macquarie Share Price

The analyst consensus on Macquarie Group is constructive, and the average price target points to meaningful upside from where the stock is currently trading.

Average Price Target Points to 17% Upside

According to data from CMC Invest, there are currently five buy ratings and four hold ratings on Macquarie Group from analysts who have recently updated their views. The average price target across all nine ratings sits at A$228.95, which implies a potential rise of more than 17% from the current Macquarie share price of A$197.385.

A price target represents where analysts believe a stock will be trading in 12 months from the date of their assessment, incorporating the Company’s earnings trajectory, valuation, and other relevant factors. The MQG price target 2027 consensus of A$228.95 reflects a market that sees the current weakness as an opportunity rather than a structural concern.

Four Business Segments Underpin the Macquarie Share Price Forecast

The breadth of Macquarie’s earnings model is a key reason analysts maintain a positive Macquarie share price forecast even in uncertain conditions. Understanding those four segments helps explain why the Company is viewed as one of the more resilient financial businesses on the ASX:

- Macquarie Capital (investment banking): Reported substantially higher net profit in the FY26 third quarter

- Macquarie Asset Management (MAM): Net profit substantially up in the same period

- Commodities and Global Markets (CGM): Net profit substantially up quarter on quarter

- Banking and Financial Services (BFS): Net profit slightly up, with deposits and loans both growing strongly

The breadth of those results across all four segments in the FY26 third quarter, covering the three months to December 2025, reinforces the case for the Macquarie share price forecast remaining positive heading into the back half of the financial year.

BFS Growth Signals a Bigger Banking Ambition

Beyond the headline analyst consensus, the operational detail emerging from Macquarie’s most recent quarterly update offers additional reasons for confidence in the MQG price target 2027 thesis.

Deposit and Loan Growth Outpaces Expectations

Macquarie’s Banking and Financial Services segment delivered deposit growth of 6% and loan growth of 7% on a quarter-over-quarter basis in the FY26 third quarter. That pace of growth is notable for a bank operating in a higher-for-longer interest rate environment and suggests Macquarie is continuing to take market share from larger incumbents.

The trajectory of BFS growth has led some observers to suggest Macquarie could become a fifth major bank in Australia over the coming years, a development that would materially expand the addressable market for its retail banking operations and add further support to the Macquarie share price forecast.

Global Diversification Adds Resilience in Volatile Markets

Macquarie’s international earnings, which account for roughly two-thirds of the Company’s total revenue, provide a meaningful buffer against domestic market weakness.

That diversification also means the Company can allocate capital opportunistically across geographies, a distinct advantage when conditions in one region deteriorate.

Figure 2: Rising market trend illustration reflecting potential upside in financial stocks [Courtesy: Freepik]

For investors tracking the Macquarie Group dividend yield alongside price appreciation potential, the combination of a globally diversified earnings base and a multi-segment business model makes Macquarie one of the more defensible large-cap financial positions on the ASX.

The Company’s track record of consistent dividend growth reflects the underlying earnings quality.

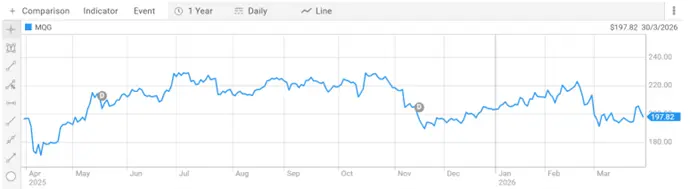

Macquarie Group Share Price

Macquarie Group Ltd (ASX: MQG) is currently trading at A$197.385 per share, with a market capitalisation of A$76.76 billion. The 52-week range stands at A$160.00 to A$231.830 per share.

Figure 3: Macquarie Group share price performance over the past year [Courtesy: ASX]

Industry Outlook

The global asset management and investment banking sector continues to benefit from rising demand for infrastructure financing, private credit, and energy transition capital, all areas where Macquarie Asset Management has established a strong competitive position.

Australian financial services firms with meaningful international revenue exposure are increasingly viewed as better positioned to navigate domestic headwinds than purely domestic-focused banks.

The Macquarie share price forecast sits within a broader context of growing institutional interest in diversified financial platforms that can generate returns across multiple market conditions rather than relying on a single earnings driver.

Future Direction and Impact on MQG Investors

The MQG price target 2027 consensus of A$228.95 represents a meaningful return from current levels, but realising that upside will depend on several factors. Macquarie’s ability to sustain the quarterly earnings momentum seen across all four segments in 3Q FY26 will be central to whether the Macquarie share price forecast is achieved.

BFS loan and deposit growth, if it continues at the 6% to 7% quarterly pace, will progressively increase Macquarie’s retail banking earnings contribution and could serve as a re-rating catalyst over the medium term.

For income-focused investors, the Macquarie Group dividend yield adds a second return dimension alongside capital appreciation. Macquarie has historically grown its dividend in line with earnings, and a recovery in the share price toward the analyst consensus target would also compress the yield for new buyers, making the current entry point more attractive on a yield basis.

The combination of a well-supported Macquarie share price forecast, a diversified global earnings base, and a growing domestic banking franchise makes MQG one of the more compelling large-cap ideas on the ASX at current levels.

Frequently Asked Questions

Q1. What is the current Macquarie share price forecast?

Ans. Based on analyst data from CMC Invest, the average price target for Macquarie Group is A$228.95, implying upside of more than 17% from the current share price of A$197.385.

Q2. What is the MQG price target 2027?

Ans. The average MQG price target across nine recent analyst ratings is A$228.95, comprising five buy ratings and four hold ratings.

Q3. What is the Macquarie Group dividend yield?

Ans. Macquarie has historically grown its dividend in line with earnings, and investors should refer to the Company’s most recent annual report or ASX announcements for the current yield.

Q4. How diversified is Macquarie’s earnings base?

Ans. Macquarie earns approximately two-thirds of its revenue internationally and operates across four segments.

Q5. How did Macquarie perform in the FY26 third quarter?

Ans. All four business segments reported positive year-over-year net profit growth in the FY26 third quarter to December 2025.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on analysis and commentary published online on 30 Mar 2026 and supplementary market data from publicly available sources. Share price and market capitalisation data reflect figures provided at the time of publication. Investing in securities involves risk. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.

Sources

https://www.fool.com.au/2026/03/30/how-much-could-the-macquarie-share-price-rise-in-the-next-year/

https://www.asx.com.au/markets/company/MQG

Last modified: March 30, 2026