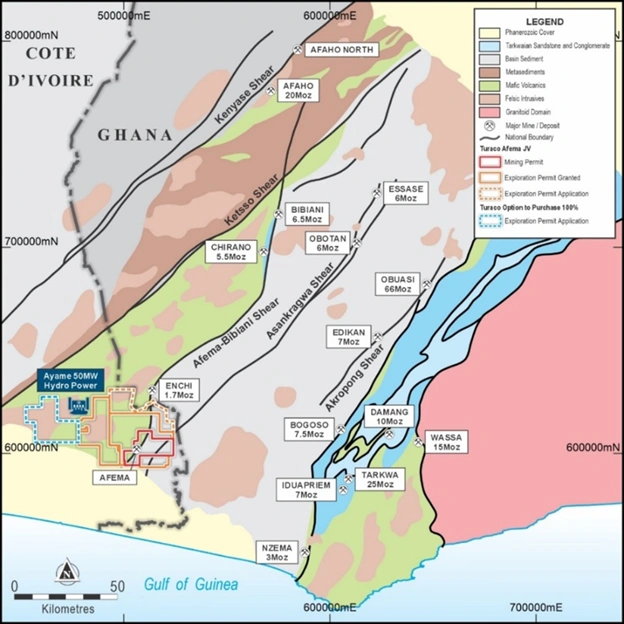

Turaco Gold Lifts Afema Resource to 4.65Moz in Major 2026 Upgrade

Turaco Gold has expanded its Afema Project resource in Côte d’Ivoire to 4.65 million ounces, the company’s third upgrade in under two years and the clearest signal yet that the project is maturing into something substantial.

The March 2026 Mineral Resource Estimate follows an extended drilling campaign across seven deposits on the Afema shear corridor, all sitting within a 10-kilometre radius of each other.

Afema Gold Project, Côte d’Ivoire — 2026 Mineral Resource Expansion [Turaco Gold]

The resource now stands at 115.3 million tonnes at 1.3 grams per tonne. Since the maiden estimate in 2024, Turaco has added more than two million ounces, a rate of growth that has few recent parallels in the region.

Managing Director Justin Tremain pointed to geology, drilling intensity and the sheer scale of the mineralised system.

“Afema continues to demonstrate exceptional growth potential, with several deposits still open along strike and at depth,” he said.

Tremain noted that shallow mineralisation and strong recoveries have helped the company move quickly through resource modelling.

A Rapid Rise Over Eighteen Months

The maiden Afema MRE, released in August 2024, outlined a promising but early system. By May 2025, it had reached 3.55Moz. October brought another jump to 4.06Moz. The latest update adds 590,000 ounces on top of that, driven by drilling at Woulo Woulo, Adiopan, Asupiri, Toilesso, Anuiri, Begnopan, Herman and Jonction.

Most deposits sit close together, linked by the Afema shear, a structure that had been identified as prospective for years before Turaco moved in. The exploration program has drawn on RC and diamond drilling, geophysics, soil sampling and auger drilling, with JORC-compliant modelling handled by independent consultants.

Metallurgical test work completed in 2025 returned recoveries of between 84.4% and 90.3% across key deposits. Those numbers fed into pit optimisations based on a gold price assumption of US$3,250 per ounce, underpinning the resource classification.

A Strengthening Position in Côte d’Ivoire’s Mining Landscape

Gold output in Côte d’Ivoire has risen sharply over the past decade. Where Burkina Faso and Mali once dominated West African exploration coverage, the Ivorian government’s permitting framework and investment climate have drawn increasing interest from developers.

Afema’s growth adds to that picture. For Turaco specifically, it firms up the company’s standing among ASX-listed West African explorers. The company closed 2025 with A$68 million in cash, giving it room to push toward development while keeping the drills turning.

The scale of the resource has drawn comparisons to other multi-million-ounce projects in the region. With several corridors still underexplored, the argument for further growth has not weakened.

Drilling Strategy and Technical Work Behind the Growth

Turaco ran multiple rigs through 2025, working first on near-surface delineation before extending along strike. The sequencing allowed the company to build inferred and indicated ounces without losing pace across multiple deposits at once.

Gradient array IP surveys mapped chargeability anomalies and sharpened drill targeting. Soil geochemistry defined high-priority structures, many of which are still producing strong intercepts.

All seven deposits in the MRE remain open, with the most immediate growth expected at Woulo Woulo, Herman, Jonction, Adiopan and the Niamienlessa tren, a 25-kilometre corridor that has seen minimal drilling.

Turaco’s multi-rig drilling program has driven rapid resource growth. [Small caps]

Infrastructure, Location and Permitting Advantage

Afema sits roughly 120 kilometres east of Abidjan, near the Ghanaian border. Sealed road access, nearby power infrastructure and a mining permit valid through 2033 reduce the logistical friction that slows many greenfield projects at this stage.

Côte d’Ivoire’s mining code has a reputation for relative clarity on permitting and land-use approvals.

The government has pushed for …

ASX Growth Shares Under Pressure – A Closer Look at the Current Opportunity

The best ASX growth shares have taken a hit in recent weeks as global market volatility continues to weigh on investor sentiment. The pullback has been broad, affecting high-quality platform businesses that have continued to execute operationally despite the turbulence. For long-term investors, the gap between share price and business performance is drawing renewed attention.

![]()

Figure 1: ASX logo displayed on market board highlighting Australian equities performance [Courtesy: Reuters]

The question of whether to buy the market dip is rarely straightforward. Prices falling does not automatically mean value is appearing. But when strong businesses are sold off alongside weaker ones, the case for selective positioning tends to become more compelling.

High-Quality Businesses Caught in a Broad Sell-Off

The current weakness across the best ASX growth shares appears driven more by sentiment than fundamentals. That distinction matters for investors trying to assess whether today’s prices reflect a genuine deterioration in business quality or simply a shift in market mood.

What Is Driving the Derating?

Several factors are behind the current pressure on ASX tech shares outlook. Rising interest rates, concerns around artificial intelligence, and broader global growth fears have all contributed to a reassessment of growth stock valuations.

When rates are elevated, the future earnings that growth companies promise are discounted more heavily. That mechanical pressure has weighed on multiples across the sector, even for businesses whose operational performance has not changed. The decision to buy the market dip in this environment requires distinguishing between businesses whose long-term thesis remains intact and those facing genuine structural headwinds.

Wisetech, TechnologyOne, and Life360 Pull Back Despite Solid Execution

Three names that reflect the current tension between sentiment and fundamentals are Wisetech Global Ltd (ASX: WTC), TechnologyOne Ltd (ASX: TNE), and Life360 Inc. (ASX: 360). Each has seen significant share price declines despite continuing to execute on their respective growth strategies.

Wisetech operates a global logistics software platform with a deeply embedded customer base. TechnologyOne is an enterprise software business with a strong track record of recurring revenue growth. Life360 provides a family safety and location-sharing platform with a growing global subscriber base.

Figure 2: Digital network visual representing technology-driven growth companies [Courtesy: Freepik]

All three sit within the broader ASX tech shares outlook that investors are currently reassessing. For those tracking the best ASX growth shares, the operational profiles of these businesses have not materially changed. What has changed is how much investors are willing to pay for them.

The Case for Gradual Accumulation During Volatility

Growth investing does not become easy simply because prices fall. The trade-off between paying a premium for future earnings and the risk that expectations shift remains present at every point in the cycle.

Selectivity Matters More Than Timing

The most practical approach to buying the market dip in growth shares is gradual accumulation rather than attempting to pick an exact bottom. Building positions over time smooths out volatility and reduces the pressure of needing perfect timing.

Selectivity remains essential. Not every business that falls is worth buying. The strongest candidates among the best ASX growth shares tend to share common characteristics: strong balance sheets, clear competitive advantages, and a demonstrated track record of execution through difficult conditions.

Long-Term Drivers Remain Intact

What makes the current environment worth paying attention to is the combination of short-term uncertainty and long-term structural growth. Digital transformation continues across industries.

Enterprise software adoption has not slowed. Healthcare innovation is accelerating. These are the tailwinds that underpin the ASX tech shares outlook over a multi-year horizon. The macro concerns around rates and global growth are real. But they are cyclical.

Figure …

St George Mining Forges Strategic European Alliance to Unlock World-Class Araxá Rare Earths

St George Mining Limited (ASX: SGQ) has taken a significant...

REA Group Share Price Slides to Multi-Year Low

REA Group Ltd (ASX: REA) saw its share price sink to a multi-year low on 30 Mar 2026, touching A$147.57 in intraday trade. That marked the weakest level for the REA share price forecast watchers have tracked since October 2023, extending a difficult run that has seen the stock fall around 17% since the start of the year.

![]()

Figure 1: REA Group office building exterior displaying the company logo [Courtesy: ABC News]

The sell-off is unfolding even as REA continues executing an on-market buy-back programme of up to A$200 million. For investors weighing ASX REA buy or sell decisions, the combination of a declining share price and active Company-backed buying adds a layer of complexity to the current picture. Broader shifts across the sector can also be seen in major bank transformation strategies.

The Sell-Off Behind the Multi-Year Low

The REA share price forecast has deteriorated sharply since October 2025, when shares were trading above A$220. The move to the A$147 to A$151 range represents a significant derating of one of the ASX’s most recognised technology and property platform businesses.

Valuation Reset, Not a Business Breakdown

The current weakness appears driven by a broad reassessment of how much investors are willing to pay for growth. Similar valuation pressures have been visible across ASX financial stocks outlook.

REA has historically commanded a premium valuation, supported by its dominant position in online property listings, strong profit margins, and reliable cash generation.

That premium is now being wound back. The ASX REA buy or sell debate centres less on any deterioration in business fundamentals and more on a market-wide shift away from paying high multiples for growth stocks. REA’s agent network, audience reach, and pricing power across premium listing products remain intact.

Property Market Conditions Add Pressure

A second layer of concern is the state of Australia’s housing market. REA’s revenue is closely tied to listing volumes, developer advertising budgets, and overall property transaction activity.

With interest rates remaining elevated and housing affordability stretched, investors are questioning the pace at which listing activity can recover. Fewer homes changing hands reduces demand for premium listing products and display advertising, both of which are central to REA’s growth profile.

This dynamic was also a driver of weakness the last time the REA share price forecast reached these levels in October 2023.

REA’s On-Market Buy-Back Continues Through the Weakness

While the share price has fallen, REA Group has been systematically buying back its own shares on the market since 23 Feb 2026. The programme runs until 31 Dec 2026 and is being executed through Goldman Sachs Australia Pty Ltd.

Buy-Back Data From the 31 Mar 2026 ASX Filing

According to the Appendix 3C notification filed on 31 Mar 2026, REA had bought back a total of 439,259 ordinary fully paid shares as at the end of 30 Mar 2026. Of that total, 33,863 shares were bought back on 30 Mar 2026 alone, at a total consideration of A$5,090,272.61.

The highest price paid across the entire programme to date was A$174.00 per share on 9 Mar 2026. The lowest price paid was A$147.83 per share on 27 Mar 2026. The buy-back does not require shareholder approval and has no fixed minimum or maximum number of securities, giving the Company full discretion on timing and volume.

The programme covers ordinary fully paid shares from a total pool of 132,117,217 securities on issue. For those tracking REA stock undervalued 2026 signals, the fact that the Company is actively purchasing shares near multi-year lows carries some weight.

REA Group Share Price

REA Group Ltd (ASX: REA) is …

Challenger Backs APRA Capital Rule Changes

Challenger Limited (ASX: CGF) has welcomed APRA’s announcement on 31 Mar 2026 of the final changes to capital standard settings for providers of longevity products. The insurance company capital changes Australia has been anticipating will come into effect from 1 Jul 2026, marking a significant shift in how longevity product providers are regulated.

![]()

Figure 1: Challenger Limited logo representing the Australian retirement income provider [Courtesy: Stocklight]

Challenger, Australia’s largest provider of annuities, sees the APRA regulatory changes 2026 Australia as a meaningful step forward for the country’s retirement income market. Challenger’s recent momentum was also evident in its strong 1H26 results, which showed rising earnings, record annuity sales, and continued funds growth.

The new framework is expected to support wider uptake of lifetime income products as more Australians approach retirement each year.

APRA’s Capital Framework and Its Significance for Longevity Providers

The final capital standard settings represent a generational shift in how regulators approach longevity product providers. For Challenger Investment Solutions Australia, the practical implications are direct and material.

![]()

Figure 2: APRA logo representing Australia’s prudential regulator [Courtesy: LinkedIn]

Lower Capital Requirements and Reduced Cyclical Risk

Challenger has confirmed that the new framework will lower the levels of required capital for the Company. It will also reduce cyclical risks to its capital position during periods of market stress, while maintaining policyholder security.

The insurance company capital changes Australia introduces are targeted specifically at providers operating in the retirement income space. These changes reflect a broader recognition that Australia’s superannuation system, while strong at accumulating savings, requires better structural support on the retirement income side.

Nick Hamilton Calls the Reforms a Generational Change

Challenger Managing Director and Chief Executive Officer Nick Hamilton offered a direct view on the significance of the APRA regulatory changes 2026 Australia represents.

“We strongly welcome APRA’s reforms, which represent the biggest changes for providers of longevity products in a generation. For Challenger, it will lower the levels of required capital and cyclical risks to our capital position during times of market stress, while maintaining policyholder security.”

Figure 3: Nick Hamilton, Managing Director and CEO of Challenger Limited [Courtesy: Challenger]

Hamilton also addressed the broader retirement challenge, noting:

“Our superannuation system is world-class at building retirement savings, but it’s still a work in progress when it comes to delivering sustainable incomes in retirement. Market volatility and high inflation are a sobering reminder that Australian retirees carry all the risks to their financial security and are ill-equipped to quantify and manage these.”

Challenger’s Role in Australia’s Retirement Income Market

Challenger is an investment management firm focused on delivering financial security for customers in or approaching retirement. The Company operates two divisions: a fiduciary Funds Management division and an APRA-regulated Life division.

Challenger Life Company Limited is Australia’s largest provider of annuities. The Company’s positioning as the country’s leading annuity provider makes it one of the most directly exposed beneficiaries of the APRA regulatory changes 2026 Australia has finalised.

Investor Day Set for 26 May 2026

Challenger is currently working through the full details of the final capital standards for longevity products. The Company has confirmed it will provide further detail on how the insurance company capital changes Australia introduces will relate to the business at its Investor Day, to be held on 26 May 2026.

The Investor Day is expected to give analysts and investors a clearer picture of how the regulatory changes translate into financial outcomes for Challenger Investment Solutions Australia, delivered through its Life division.

Challenger Share Price

Challenger Limited (ASX: CGF) is currently trading at A$8.390 …

Magellan Completes Share Purchase Plan (MFG)

Magellan Financial Group Ltd (ASX: MFG) has confirmed the successful completion of its Share Purchase Plan, marking a key milestone in its capital raising strategy.

The plan closed at 5:00 pm Sydney time on Wednesday, 25 March 2026, achieving its stated target of $20 million.

The Company issued approximately 2,366,548 new fully paid ordinary shares at a price of $8.45 per share, which matched the institutional placement price that it announced on Monday, 2 March 2026.

The Magellan shareholder update demonstrates a systematic method to handle capital, which protects current shareholder interests.

Magellan confirms completion of its $20M share purchase plan. [Courtesy: Dreamstime]

What Happened In The Magellan Shareholder Update?

The Magellan share plan news demonstrates high shareholder engagement because the Company received $129.4 million in legitimate applications. A total of 5,195 eligible shareholders participated, representing a participation rate of 17%.

The Company followed the plan’s rules to implement a scale-back process because demand for the product exceeded the $20 million target.

Applications up to $997.10 or up to 118 shares were not scaled back, while larger applications were reduced on a pro-rata basis. The allocation process used shareholdings recorded at 7:00 pm Sydney time on Friday, 27 February 2026, to establish an equal distribution method for all participants.

Magellan Completes Share Plan News Highlights Oversubscription Strength

The oversubscription reached its maximum level because investors showed strong confidence in Magellan Financial Group’s future prospects.

The offer attracted six times more demand than its original target, which proved to be its most attractive feature. The structured scale-back process distributed assets fairly to shareholders, who received their maximum application limit of $30,000.

The program provided each eligible participant with 118 new shares as their base allocation, which maintained the program’s open access policy.

The Company demonstrates its capability to raise funds because it secures investments from sources that compete with its market position.

Oversubscription reflects strong investor confidence in Magellan. [Courtesy: Magellan Investment Partners]

Why Does This Magellan Shareholder Update Matter To Investors?

The current development shows that investors want to invest while the Company keeps its capital spending under strict control.

The Company achieved $129.4 million in application increase because investors believe in its business plan and future results. The pricing of shares matches institutional placements, which gives investors equal access to the market.

The scale-back mechanism shows that the Company treats its shareholders according to equitable standards. The asset management industry displays positive market sentiment when participation levels reach these thresholds.

MFG Share Plan Details, Outline, Allocation, and Timeline Clarity

The MFG share plan details establish precise timelines that investors and stakeholders can use to track their investments. The new shares are expected to be issued on Wednesday, 1 April 2026, and commence trading on the ASX on Thursday, 2 April 2026.

These shares will maintain the same rights as current shares, which protects existing shareholders from losing their entitlements. The Company plans to send holding statements between the scheduled date and Wednesday, 8 April 2026.

The Company will process refunds for scaled-back applications through direct credit on Wednesday, 1 April 2026, according to the SPP Booklet, which was issued on Wednesday, 11 March 2026.

Timeline confirms issuance, trading, and refund schedule for investors. [Courtesy: Nacha]

How Will The Magellan Shareholder Update Influence Future Strategy?

A strong capital raise and investor backing position Magellan for its next phase of growth and strategic execution:

- Enhances capital structure, supporting long-term strategic initiatives and financial stability.

- Provides additional funds to improve operational flexibility across business segments.

- Enables investment in emerging market opportunities and potential growth areas.

- Encourages market participants to

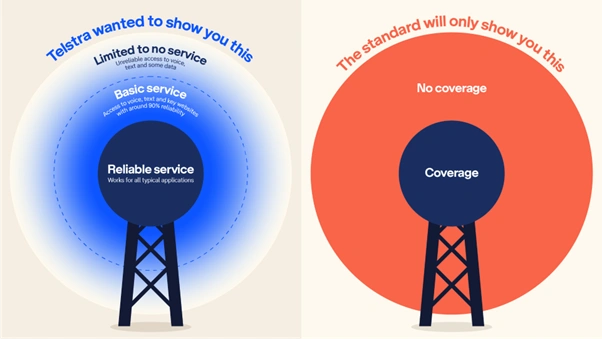

Telstra’s Coverage Maps Are Shrinking. Here’s What That Means for You

Australia’s communications regulator, the Australian Communications and Media Authority (ACMA), published its final Telecommunications (Mobile Network Coverage Maps) Industry Standard 2026 on 31 March. Mobile operators must publish standardised 4G and 5G coverage maps by 30 June 2026, using one of four categories: good, moderate, basic, or no coverage.

The rule is meant to give consumers an apples-to-apples comparison between Telstra, Optus, and TPG. But Telstra says the fine print could mislead millions of customers, particularly those in regional Australia.

A Signal Threshold That Could Redraw the Map

The crux of the issue is a single technical number.

Under the new rules, areas with signal strengths below -115 dBm are declared as not having a usable service and cannot be shown on coverage maps. That threshold determines what counts as “coverage” and what gets labelled as nothing at all.

Telstra says the draft would wipe roughly a third of its landmass from its map, potentially erasing around one million square kilometres. The company argued for a lower cutoff of -122 dBm, which it says more accurately reflects where calls, texts, and data actually work.

Every month, more than 1.5 million Telstra customers use coverage that sits below that -115 dBm threshold. That includes people travelling through remote areas, not just those who live there.

What Telstra Says Its Network Actually Delivers

Telstra ran independent tests to back its position before the final standard was handed down.

In late 2025, a third party drove 60,000 kilometres across the country using a standard Samsung S25 smartphone with no external antenna. Results showed that more than 90% of the time, customers at -122 dBm could load web pages within seconds, start apps without excessive delay, and make clear voice calls.

The company also points to the volume of emergency calls made in areas that will now appear blank on the new maps. Around 57,000 emergency calls are made each year in those zones, along with 700,000 voice calls and 750,000 texts per day, plus 300TB of data.

Shailin Sehgal, Telstra’s Group Executive for Global Networks and Technology, put it plainly: “If a map says ‘no coverage’ but a customer can still call, text or get online nine out of ten times, there’s a very real risk of confusion.“

Telstra’s existing coverage map (left) compared to the projected reduced map under the ACMA standard (right). [Telstra]

Optus and TPG Are on the Other Side

Not everyone agrees with Telstra’s reading.

TPG Telecom urged the ACMA to adopt the -115 dBm threshold, saying it was “deemed acceptable” by the federal government’s National Audit of Mobile Coverage. The carrier also repeated claims that its engineers could not make calls in areas Telstra labelled as full coverage.

A TPG spokesperson called the new standard “a win for consumers,” saying coverage should mean a phone actually works, not that it might show a bar of signal that cannot support a call.

The ACCC also backed the stricter approach, saying the lack of a transparent standard had prevented it from taking enforcement action against misleading coverage claims. The competition regulator recommended that telcos not be given flexibility to adopt alternative thresholds, at least for now.

What the New Standard Actually Requires

The new rules are not just about what counts as coverage. They also standardise how maps are presented.

The ACMA acknowledged that in areas shown as having no coverage, some people may still be able to make calls or send SMS, but overall service is expected to be very limited, inconsistent, or non-existent. Maps must also be updated at least every three months.

ACMA …

Auric Mining Achieves Record $5.2 Million Profit after Tax Amid Landmark Transition to Gold Producer

Auric Mining Limited (ASX: AWJ) has concluded a...

Alkane Locks In A$150M Credit Package as Cash Reserves Hit A$232M

What the Deal Actually Looks Like

The facility is split into two parts. The larger piece is a A$110 million revolving credit facility that Alkane can draw on for general corporate use. Working capital, operating costs, acquisitions, whatever comes up. The second piece is a A$40 million contingent instrument facility.

That one is less about borrowing new money and more about unlocking cash that is already sitting idle. Alkane currently has up to A$40 million tied up in performance guarantees across its operations. This facility releases that capital so it can actually be put to work.

Alkane Resources strengthens liquidity through a A$150 million syndicated credit facility. [ABC]

The term runs three years with two one-year extension options, subject to lender sign-off and six months’ notice. There is no mandatory gold hedging requirement built into the agreement.

That matters because it means Alkane keeps full exposure to the gold price. If spot gold keeps running, the company benefits without having pre-sold its output at a lower price.

Four Major Banks Signed On

ANZ, Commonwealth Bank, Macquarie Bank, and Westpac all joined the syndicate. Getting four tier-one Australian lenders into the same deal is not something a struggling miner manages.

Banks at this level run detailed credit assessments before committing. Their participation reflects the view that Alkane’s balance sheet is in solid shape and that its operations are generating reliable cash flow.

Major Australian banks backed Alkane’s syndicated credit facility, reflecting lender confidence. [Broker Daily]

Working with a syndicate also reduces the Company’s dependence on any single funding relationship. If one lender steps back during a future refinancing, the others provide continuity. That kind of structural resilience is worth having, particularly for a mining company with three producing assets across two countries.

The August 2025 Debt Repayment Set This Up

Last August, Alkane paid off a A$45 million project finance facility before it was due. Early repayment is not the norm. Most companies hold onto debt facilities even when they have cash, because the optionality is valuable.

Paying it off early suggests the company felt comfortable enough with its cash position to close out the liability and start fresh. It also cleared the path to negotiate the new syndicated package on cleaner terms, without the existing facility complicating the structure.

Three Mines, One Balance Sheet

Alkane’s cash generation comes from three producing operations. Tomingley is a gold mine in New South Wales. Costerfield, in Victoria, produces both gold and antimony. Björkdal is a gold mine in Sweden.

Tomingley gold mine in New South Wales remains a key contributor to Alkane’s production. [Mining Technology]

Running three mines across two continents introduces operational complexity, but it also means the company is not entirely exposed to problems at any one site. A geotechnical issue at Tomingley or a maintenance shutdown at Björkdal does not stop the cash flowing from the others.

The antimony exposure at Costerfield is worth noting separately. Antimony is a critical mineral used in flame retardants and increasingly in energy storage applications.

Prices have moved significantly in recent years as supply chains tighten. That gives Costerfield a revenue profile that gold-only mines do not have, and it adds a layer of diversification that investors in the pure-play gold space do not usually get.

What the Facility Means in Practice

A revolving credit facility is not a loan in the traditional sense. Alkane does not have to draw the full A$110 million. It can draw part of it, repay it, and draw again. The interest accrues only on what is actually drawn.

That makes it a …

Bullabulling Gold Results Strengthen Minerals 260 Footprint

The Western Australian project by Minerals 260 has provided good Bullabulling gold outcomes, which support the high-grade mineralisation and expansion opportunities. The latest drilling campaign at Bullabulling has delivered standout results, reinforcing the project’s strong performance and scale:

- Exceptional intercept of 7 metres at 7.2 grams per tonne gold highlights high-grade mineralisation.

- Broad intercept of 28 metres at 1.7g/t gold confirms consistency across the deposit.

- Results form part of an ongoing drilling program at the 100 per cent-owned 4.5-million-ounce project.

- The project is located 25 kilometres west of Coolgardie in Western Australia.

- Assays were received from 22 drill holes, demonstrating extensive exploration activity.

- Total drilling covered 5425 metres, supporting strong dataset reliability.

Managing director Luke McFadyen said the outcomes continue to strengthen confidence in the project, noting that “Drilling results received since the December 2025 MRE continue to reinforce our confidence in the growth potential of the MRE,” reflecting sustained momentum in resource development.

Drilling operations at the Bullabulling gold project in Western Australia. [Courtesy: Minerals 260]

Bullabulling Gold Results Strengthen Resource Expansion Strategy

The ongoing drilling in the Bacchus deposit intersects high-grade and thick mineralisation along the footwall shear zone that validates the expansion strategy in the project. Key drilling results from the Bacchus deposit continue to highlight strong grades and expansion potential:

- Intercepts include 11 metres at 3.3g/t gold, 9 metres at 3.0g/t gold, and 12 metres at 2.8g/t gold.

- A high-grade core of 2 metres at 22.6g/t gold underscores the presence of rich mineralised zones.

- Notable intercept of 6 metres at 2.9g/t gold from 276 metres suggests potential growth at depth.

McFadyen highlighted the dual focus of the program, stating, “The current program is focused on both expanding the resource and upgrading classifications, particularly within shallow areas targeted for early mining, while also testing high-priority extension targets at depth and along strike,” signalling a balanced approach to near-term and long-term development.

Why Do Bullabulling Gold Results Matter For Investors?

The Bullabulling gold outcomes have immense consequences for investors who have an inclination to be exposed to new gold possibilities. Regular high-grade intercepts may indicate potential resource expansion and better project economics,s especially in a well-established mining area such as Western Australia.

The successful drilling at Minerals 260 continues to give the company a strong standing in the competitive gold exploration market. The magnitude of the 4.5-million-ounce project and the further expansion of the mineralisation may arouse the interest of the market.

The developments will have a probable impact on the investor sentiment when the company reaches the milestones of feasibility.

High-grade gold core samples from the Bullabulling drilling program. [Courtesy: Everest Metals]

Minerals 260 Expands Its Western Australia Gold Footprint

The Phoenix deposit drilling has been producing consistent drilling results in accordance with or beyond the current mineral resource estimate, whereby intercepts of 7 metres at 4.7g/t gold and 5 metres at 3.8g/t gold are seen to support continuity.

In the greater project, mineralisation is now established over 8.5 kilometres strike length, and several mineralised lenses have been observed beyond the current estimate.

Minerals 260 now has seven rigs on site to proceed with infill and extensional drilling programs to upgrade the resources and to upgrade classification.

The company has also increased its land footprint through the acquisition of more tenures to make the landholding in the region reach about 750 square kilometres.

Where And When Is The Bullabulling Exploration Advancing?

The Bullabulling project is at Coolgardie, 25 kilometres west of Western Australia, which is one of the well-established gold-producing regions in the world. The drilling program underway …